1 はじめに 32

1.1 調査目的 32

1.2 市場の定義 32

1.3 調査範囲 33

1.3.1 考慮したセグメントと地域 33

1.3.2 含むものと含まないもの 34

1.3.3 考慮した年数 34

1.3.4 通貨 34

1.4 利害関係者 35

1.5 変更点のまとめ 35

2 調査方法 36

2.1 調査データ 36

2.1.1 二次データ 37

2.1.1.1 主な二次情報源 37

2.1.1.2 二次調査の目的 38

2.1.1.3 二次資料からの主要データ 39

2.1.2 一次データ 39

2.1.2.1 主要な一次情報源 40

2.1.2.2 一次調査の目的 40

2.1.2.3 主要な業界インサイト 41

2.2 市場規模の推定 42

2.2.1 ボトムアップアプローチ 43

2.2.1.1 企業の収益推定アプローチ 44

2.2.1.2 顧客ベースの市場推定 44

2.2.2 トップダウンアプローチ 45

2.2.2.1 一次インタビュー 46

2.3 データの三角測量 48

2.4 市場シェア評価 49

2.5 調査の前提 49

2.6 成長率の仮定/市場予測方法 50

2.7 調査の限界 50

2.8 リスク評価 50

3 エグゼクティブ・サマリー 51

4 プレミアムインサイト

4.1 キャプノグラフィ装置市場の概要 55

4.2 キャプノグラフィ装置市場:地域別、2024年対2029年(百万米ドル) 56

4.3 キャプノグラフィ装置市場:エンドユーザー別、国別

2024 (百万米ドル) 56

4.4 キャプノグラフィ装置市場の地理的スナップショット 57

5 市場の概要

5.1 導入 58

5.1.1 推進要因 59

5.1.1.1 呼吸器疾患の有病率の増加 59

5.1.1.2 パルスオキシメトリに対するカプノグラフィの臨床的利点 60

5.1.1.3 CO2 モニタリングを必要とする手術件数および対象疾患の増加 61

5.1.2 抑制要因

5.1.2.1 カプノグラフィ装置の承認に関する複雑な規制枠組み 61

5.1.3 機会 62

5.1.3.1 臨床研究エビデンスの増加 62

5.1.3.2 新興国におけるヘルスケア産業の成長機会 63

5.1.4 課題 63

5.1.4.1 カプノメーターを操作する熟練技術者と専門トレーニングの不足 63

5.2 業界動向 64

5.2.1 ウェアラブル機器とワイヤレス機器の進歩 64

5.2.2 マルチパラメーターモニターとの統合 65

5.3 バリューチェーン分析 65

5.4 ポーターのファイブフォース分析 67

5.4.1 新規参入企業の脅威 68

5.4.2 サプライヤーの交渉力 68

5.4.3 買い手の交渉力 68

5.4.4 代替品の脅威 68

5.4.5 競合の激しさ 68

5.5 主要ステークホルダーと購買基準 69

5.5.1 購入プロセスにおける主要ステークホルダー 69

5.5.2 主要な購買基準 70

5.6 特許分析 71

5.7 貿易データ分析 73

5.7.1 HSコード9018の輸入データ 73

5.7.2 HSコード9018の輸出データ 74

5.8 主要会議・イベント(2024-2025年) 75

5.9 アンメットニーズと主要ペインポイント 76

5.10 エコシステム分析 77

5.11 サプライチェーン分析 78

5.11.1 著名企業 78

5.11.2 中小企業 78

5.11.3 エンドユーザー 79

5.12 AI/ジェネAIがカプノグラフィ装置市場に与える影響 79

5.13 顧客のビジネスに影響を与えるトレンド/混乱 80

5.14 技術分析 81

5.14.1 主要技術 81

5.14.1.1 主流のカプノグラフィ 81

5.14.1.2 サイドストリーム・キャプノグラフィ 82

5.14.1.3 波形キャプノグラフィ 82

5.14.2 補完的技術

5.14.2.1 パルスオキシメトリー 82

5.14.2.2 人工呼吸器 82

5.14.3 隣接技術

5.14.3.1 マイクロモーター技術 82

5.15 規制情勢分析 83

5.15.1 規制機関、政府機関、その他の組織 83

5.15.2 規制の枠組み 86

5.15.2.1 北米 86

5.15.2.1.1 米国 86

5.15.2.2 欧州 88

5.15.2.3 アジア太平洋地域 89

5.15.2.3.1 日本 89

5.15.2.3.2 インド 89

5.15.2.3.3 中国 90

5.16 保険償還シナリオ分析 91

5.16.1 カプノグラフィ手技の償還コード 91

5.16.2 キャプノグラフィ装置の地域別償還状況 92

5.17 投資と資金調達シナリオ 93

5.18 価格分析 94

5.18.1 カプノグラフィ装置の地域別平均販売価格 95

5.18.2 上位3つのアプリケーションの平均販売価格、

主要プレーヤー別、2023年 99

6 キャプノグラフィ装置市場、製品別 100

6.1 導入 101

6.2 装置 101

6.2.1 マルチパラメータキャプノメータ 104

6.2.1.1 ハンドヘルド型マルチパラメータキャプノメータ 106

6.2.1.1.1 患者の安全性の向上、携帯性、採用を助ける可聴・視覚アラーム内蔵 106

6.2.1.2 従来の多波長型カプノメーター 109

6.2.1.2.1 麻酔を伴う複雑な手術の増加がセグメントの成長を支える 109

6.2.2 単独型カプノメーター 111

6.2.2.1 ハンドヘルド型独立型カプノメーター 114

6.2.2.1.1 救急搬送件数と複雑な手術件数の増加がセグメント成長を促進 114

6.2.2.2 従来型スタンドアロン型カプノメーター 116

6.2.2.2.1 簡単な携帯性とクリティカルケア環境での使用がセグメント成長を促進 116

6.3 ソフトウェア 118

6.3.1 より良い臨床的意思決定と患者管理が市場成長を促進 118

6.4 キャプノグラフィ付属品&消耗品 121

6.4.1 好ましい償還シナリオが市場成長を後押し 121

7 キャプノグラフィ装置市場:技術別 124

7.1 導入 125

7.2 主流のカプノグラフィ 125

7.2.1 高精度、高速応答時間、新生児への適合性向上が市場成長を促進 125

7.3 サイドストリームカプノグラフィ 128

7.3.1 信頼性の高い呼気終末CO2濃度測定が臨床現場での採用を促進 128

7.4 マイクロストリームカプノグラフィ 130

7.4.1 手術室での使用を制限する黒体赤外線技術の限界 130

8 カプノグラフィ装置市場、用途別 133

8.1 導入 134

8.2 心臓ケア 134

8.2.1 心肺手術件数の増加とEco2レベルのモニタリング選好の高まりが市場を牽引 134

8.3 外傷・救急医療 137

8.3.1 交通事故の増加が市場成長を促進 137

8.4 呼吸器モニタリング 139

8.4.1 対象となる呼吸器疾患の有病率の上昇が市場成長を後押し 139

8.5 その他の用途 142

9 キャプノグラフィ装置市場:エンドユーザー別 145

9.1 導入 146

9.2 病院 148

9.2.1 ICU患者の気道関連死亡の減少が市場成長を加速 148

9.3 外来手術センターと在宅ケア環境 151

9.3.1 ascペイメントシステムによる償還承認医療処置の増加が市場を牽引 151

9.4 その他のエンドユーザー 153

10 キャプノグラフィ装置市場:地域別 156

10.1 はじめに 157

10.2 北米 157

10.2.1 北米のマクロ経済見通し 161

10.2.2 米国 161

10.2.2.1 予測期間中、北米のカプノグラフィ装置市場は米国が支配的 161

10.2.3 カナダ 164

10.2.3.1 対象となる呼吸器疾患の有病率の上昇が市場成長を支える 164

10.3 欧州 167

10.3.1 欧州のマクロ経済見通し 171

10.3.2 ドイツ 172

10.3.2.1 整備された医療インフラと高い政府投資が市場成長を促進 172

10.3.3 英国 175

10.3.3.1 対象患者数の増加と医療費の増加が市場成長を促進 175

10.3.4 フランス 177

10.3.4.1 カプノグラフィ監視手順に対する認知度の高まりと外傷症例の増加が市場成長を促進 177

10.3.5 イタリア 180

10.3.5.1 糖尿病患者の増加と高齢者人口の増加が市場成長を促進 180

10.3.6 スペイン 183

10.3.6.1 生活習慣病の蔓延がカプノグラフィ機器の需要を促進 183

10.3.7 その他のヨーロッパ 185

10.4 アジア太平洋地域 188

10.4.1 アジア太平洋地域のマクロ経済見通し 193

10.4.2 日本 193

10.4.2.1 高齢者人口の増加と肥満の蔓延が市場成長を促進 193

10.4.3 中国 196

10.4.3.1 高い対象患者数と入院サービスの改善により市場成長をサポート 196

10.4.4 インド 199

10.4.4.1 有利な規制政策と高い公的医療費が市場成長を促進 199

10.4.5 オーストラリア 202

10.4.5.1 患者数の増加と助成金の増加が市場成長を促進 202

10.4.6 韓国 205

10.4.6.1 研究開発活動への重点化と健康保険の高い普及率が市場成長を促進 205

10.4.7 その他のアジア太平洋地域 208

10.5 ラテンアメリカ 211

10.5.1 ラテンアメリカのマクロ経済見通し 214

10.5.2 ブラジル 214

10.5.2.1 医療セクターの改善と官民投資の増加が市場を牽引 214

10.5.3 メキシコ 217

10.5.3.1 恵まれた貿易環境と外国企業の参入が市場成長を促進 217

10.5.4 その他のラテンアメリカ地域 220

10.6 中東・アフリカ 223

10.6.1 中東・アフリカのマクロ経済展望 226

10.6.2 北アフリカ諸国 227

10.6.2.1 医療インフラの整備と患者の安全性重視の高まりが市場を牽引 227

10.6.3 その他の中東・アフリカ地域 230

11 競争環境 233

11.1 はじめに 233

11.2 主要プレーヤーの戦略/勝利への権利 233

11.2.1 キャプノグラフィ装置市場で各社が採用した戦略の概要 234

11.3 収益分析、2019年~2023年 235

11.4 市場シェア分析、2023年 237

11.4.1 主要市場プレイヤーのランキング 238

11.5 企業評価マトリックス:主要企業、2023年 239

11.5.1 スター企業 239

11.5.2 新興リーダー 239

11.5.3 浸透型プレーヤー 239

11.5.4 参加企業 239

11.5.5 企業フットプリント:主要プレーヤー、2023年 241

11.5.5.1 企業フットプリント 241

11.5.5.2 製品フットプリント 242

11.5.5.3 技術のフットプリント 242

11.5.5.4 アプリケーションフットプリント 243

11.5.5.5 エンドユーザー・フットプリント 244

11.5.5.6 地域別フットプリント 245

11.6 企業評価マトリクス:新興企業/SM(2023年) 246

11.6.1 進歩的企業 246

11.6.2 対応力のある企業 246

11.6.3 ダイナミックな企業 246

11.6.4 スタートアップ・ブロック 246

11.6.5 競争ベンチマーク:新興企業/SM(2023年) 248

11.7 企業評価と財務指標 249

11.7.1 財務指標 249

11.7.2 企業評価 249

11.8 ブランド/製品の比較 250

11.9 競争シナリオ 251

11.9.1 製品の上市と承認 251

11.9.2 取引 252

12 企業プロファイル 253

12.1 主要企業 253

Becton

Dickinson and company (US)

Medtronic (US)

Koninklijke Philips N.V.(Netherlands)

GE Healthcare (US)

Drägerwerk AG (Germany)

Nihon Kohden (Japan)

Zoll Medical (US)

Edan Instruments Inc (China)

Hamilton Medical (Switzerland )

Masimo Corporation (US)

Mindray (China)

13 付録 311

13.1 ディスカッション・ガイド 311

13.2 Knowledgestore: Marketsandmarketsの購読ポータル 316

13.3 カスタマイズオプション 318

13.4 関連レポート 318

13.5 著者の詳細 319

Growth factors include the high incidence of chronic respiratory diseases such as asthma, COPD, and sleep apnea are significantly driving the market for capnography equipment. An upsurge in home healthcare would require non-invasive monitoring solutions, thus boost the growth of this market. Improvements in technology especially about miniaturization, reduced profile, and wireless connectivity would ensure that capnography equipment is portable and user-friendly.

“Capnography accessories & disposables to register largest market share in 2022-2029.”

The largest share in capnography equipment consists of capnography accessories & disposables. Capnography accessories and disposables are also some of the necessary parts of the proper working of capnography equipment. These include disposable sampling lines, filters, and connectors, which are very necessary to maintain hygiene levels and prevent cross-contamination. Calibration gases are also needed to ensure the accuracy of measurements of capnography. Other devices would include power cords, wall mounts, and carrying cases that increase the convenience and portability of capnography devices.

“Hospitals segment held the largest share of capnography equipment market in 2023, by End-user.”

Based on the end-user, the capnography equipment market is segmented into hospitals. ambulatory surgery centers & home care and other end users. In the year 2023, the global capnography equipment market was dominated by hospitals. The use of capnography equipment is extremely prevalent in critical care areas, such as ICUs, operating rooms, emergency departments, and respiratory care units of hospitals. Such hospitals form the biggest market in the capnography equipment market because of this widespread usage. The growth of surgeries, critical care procedures, and respiratory illnesses has further led to a growing demand for capnography devices. In addition, the increased practice of monitoring patients for early respiratory complications detection along with the development of acute care has worked in favor of the integration of capnography in the clinical settings of hospitals.

"Asia Pacific to register highest growth rate in the market during the forecast period."

The Asia-Pacific region is projected to exhibit the highest CAGR in the capnography equipment market. This growth is primarily driven by factors such as increasing healthcare expenditure, rising prevalence of respiratory diseases, growing geriatric population, and increasing awareness about the benefits of early detection and treatment of respiratory disorders. Additionally, the expanding healthcare infrastructure and increasing adoption of advanced medical technologies in countries like India and China are further contributing to the growth of the capnography equipment market in this region.

A number of drivers were responsible for the upswing, including:

A breakdown of the primary participants referred to for this report is provided below:

• By Company Type: Tier1- 40%, Tier2- 30%, and Tier 3- 30%

• By Designation: C-level-- 55%, Director-level–27%, and Others–18%

• By Region: North America–35%, Europe-32%, Asia Pacific–25%, Latin America-6% , Middle East & Africa-2%

Prominent players in this market are Becton, Dickinson and company (US), Medtronic (US), Koninklijke Philips N.V.(Netherlands), GE Healthcare (US), Drägerwerk AG (Germany), Nihon Kohden (Japan), Zoll Medical (US), Edan Instruments Inc (China), Hamilton Medical (Switzerland ), Masimo Corporation (US), Mindray (China), among others.

Research Coverage

Capnography equipment market is segmented by product, technology, application, end-user, and region. Factors determining market growth are driving forces, restrains, opportunities, and challenges, as well as those offering opportunities and challenges for stakeholders. Further examining the competitive landscape among the top players, the report does this. In doing so, it further segments the market into micro-markets for analyzing growth trends, prospects, and contribution to the overall market. It outlines the future revenue growth across the different market segments in five of the major regions.

Key Benefits of Buying the Report:

The report would be useful for new market entrants in the capnography equipment market as it gives detailed information about the market. This helps to get a good understanding of any investment opportunities. The report provides in-depth insight into key and smaller players which helps in doing strong risk assessment for investment decisions. The report segments the market precisely by both end-users and by regions to gain focused insights in specific market segments. Furthermore, it outlines the critical trends, challenges, growth drivers, and opportunities to facilitate strategic decision-making through well-rounded analysis.

The report provides the insights on the following pointers:

Analysis of the key drivers, restraints, opportunities, and challenges influencing the rise of the capnography equipment market The majority of the capnography equipment market is driven by the increase in chronic respiratory diseases such as asthma, COPD, and sleep apnea. There is an increasing demand for non-invasive monitoring solutions, especially in home care environments. Advancements in technology also involve miniaturization and wireless connectivity that enable smaller and user-friendly size capnography devices to be utilized.

Product Development/Innovation: The report showcases emerging technologies in the domain, ongoing R&D activities, and recent product and service launches in the market for capnography equipment.

Market Development: It has elaborated about the new product development and unexplored markets, latest developments, and investment in the capnography equipment market.

Market Diversification: Detailed insight into new product launches, unexplored markets, recent developments, and investments made in the capnography equipment market.

Competitive Assessment: Detailed assessment of market share, service offerings leading strategies of key players such as Becton, Dickinson and company (US), Medtronic (US), Koninklijke Philips N.V.(Netherlands), GE Healthcare (US), Drägerwerk AG (Germany), among others.

1 INTRODUCTION 32

1.1 STUDY OBJECTIVES 32

1.2 MARKET DEFINITION 32

1.3 STUDY SCOPE 33

1.3.1 SEGMENTS AND REGIONS CONSIDERED 33

1.3.2 INCLUSIONS & EXCLUSIONS 34

1.3.3 YEARS CONSIDERED 34

1.3.4 CURRENCY CONSIDERED 34

1.4 STAKEHOLDERS 35

1.5 SUMMARY OF CHANGES 35

2 RESEARCH METHODOLOGY 36

2.1 RESEARCH DATA 36

2.1.1 SECONDARY DATA 37

2.1.1.1 Key secondary sources 37

2.1.1.2 Objectives of secondary research 38

2.1.1.3 Key data from secondary sources 39

2.1.2 PRIMARY DATA 39

2.1.2.1 Key primary sources 40

2.1.2.2 Objectives of primary research 40

2.1.2.3 Key industry insights 41

2.2 MARKET SIZE ESTIMATION 42

2.2.1 BOTTOM-UP APPROACH 43

2.2.1.1 Company revenue estimation approach 44

2.2.1.2 Customer-based market estimation 44

2.2.2 TOP-DOWN APPROACH 45

2.2.2.1 Primary interviews 46

2.3 DATA TRIANGULATION 48

2.4 MARKET SHARE ASSESSMENT 49

2.5 STUDY ASSUMPTIONS 49

2.6 GROWTH RATE ASSUMPTIONS/MARKET FORECASTING METHODOLOGY 50

2.7 RESEARCH LIMITATIONS 50

2.8 RISK ASSESSMENT 50

3 EXECUTIVE SUMMARY 51

4 PREMIUM INSIGHTS 55

4.1 CAPNOGRAPHY EQUIPMENT MARKET OVERVIEW 55

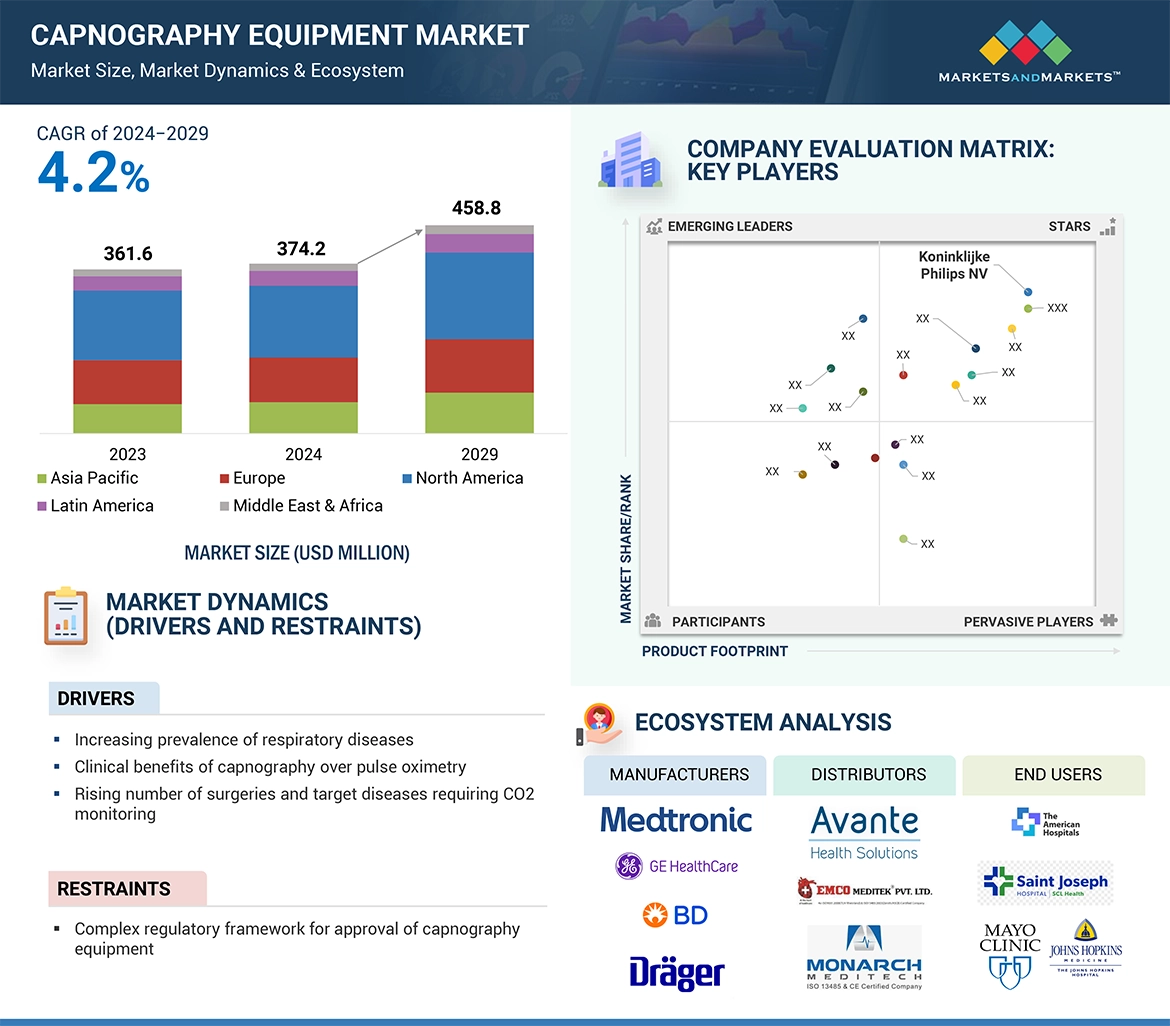

4.2 CAPNOGRAPHY EQUIPMENT MARKET, BY REGION, 2024 VS. 2029 (USD MILLION) 56

4.3 CAPNOGRAPHY EQUIPMENT MARKET, BY END USER AND COUNTRY,

2024 (USD MILLION) 56

4.4 GEOGRAPHIC SNAPSHOT OF CAPNOGRAPHY EQUIPMENT MARKET 57

5 MARKET OVERVIEW 58

5.1 INTRODUCTION 58

5.1.1 DRIVERS 59

5.1.1.1 Increasing prevalence of respiratory diseases 59

5.1.1.2 Clinical benefits of capnography over pulse oximetry 60

5.1.1.3 Rising number of surgeries and target diseases requiring CO2 monitoring 61

5.1.2 RESTRAINTS 61

5.1.2.1 Complex regulatory framework for approval of capnography equipment 61

5.1.3 OPPORTUNITIES 62

5.1.3.1 Increased availability of clinical research evidence 62

5.1.3.2 Growth opportunities for healthcare industry in emerging economies 63

5.1.4 CHALLENGES 63

5.1.4.1 Lack of skilled technicians and specialized training for operating capnometers 63

5.2 INDUSTRY TRENDS 64

5.2.1 ADVANCEMENTS OF WEARABLE AND WIRELESS DEVICES 64

5.2.2 INTEGRATION WITH MULTIPARAMETER MONITORS 65

5.3 VALUE CHAIN ANALYSIS 65

5.4 PORTER’S FIVE FORCES ANALYSIS 67

5.4.1 THREAT OF NEW ENTRANTS 68

5.4.2 BARGAINING POWER OF SUPPLIERS 68

5.4.3 BARGAINING POWER OF BUYERS 68

5.4.4 THREAT OF SUBSTITUTES 68

5.4.5 INTENSITY OF COMPETITIVE RIVALRY 68

5.5 KEY STAKEHOLDERS & BUYING CRITERIA 69

5.5.1 KEY STAKEHOLDERS IN BUYING PROCESS 69

5.5.2 KEY BUYING CRITERIA 70

5.6 PATENT ANALYSIS 71

5.7 TRADE DATA ANALYSIS 73

5.7.1 IMPORT DATA FOR HS CODE 9018 73

5.7.2 EXPORT DATA FOR HS CODE 9018 74

5.8 KEY CONFERENCES & EVENTS, 2024–2025 75

5.9 UNMET NEEDS AND KEY PAIN POINTS 76

5.10 ECOSYSTEM ANALYSIS 77

5.11 SUPPLY CHAIN ANALYSIS 78

5.11.1 PROMINENT COMPANIES 78

5.11.2 SMALL AND MEDIUM-SIZED ENTERPRISES 78

5.11.3 END USERS 79

5.12 IMPACT OF AI/GEN AI ON CAPNOGRAPHY EQUIPMENT MARKET 79

5.13 TRENDS/DISRUPTIONS IMPACTING CUSTOMER’S BUSINESS 80

5.14 TECHNOLOGY ANALYSIS 81

5.14.1 KEY TECHNOLOGIES 81

5.14.1.1 Mainstream capnography 81

5.14.1.2 Side-stream capnography 82

5.14.1.3 Waveform capnography 82

5.14.2 COMPLEMENTARY TECHNOLOGIES 82

5.14.2.1 Pulse oximetry 82

5.14.2.2 Ventilators 82

5.14.3 ADJACENT TECHNOLOGIES 82

5.14.3.1 Microrotor technology 82

5.15 REGULATORY LANDSCAPE ANALYSIS 83

5.15.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS 83

5.15.2 REGULATORY FRAMEWORK 86

5.15.2.1 North America 86

5.15.2.1.1 US 86

5.15.2.2 Europe 88

5.15.2.3 Asia Pacific 89

5.15.2.3.1 Japan 89

5.15.2.3.2 India 89

5.15.2.3.3 China 90

5.16 REIMBURSEMENT SCENARIO ANALYSIS 91

5.16.1 REIMBURSEMENT CODES FOR CAPNOGRAPHY PROCEDURES 91

5.16.2 REIMBURSEMENT LANDSCAPE FOR CAPNOGRAPHY EQUIPMENT, BY REGION 92

5.17 INVESTMENT & FUNDING SCENARIO 93

5.18 PRICING ANALYSIS 94

5.18.1 INDICATIVE SELLING PRICE OF CAPNOGRAPHY EQUIPMENT, BY REGION 95

5.18.2 AVERAGE SELLING PRICE FOR TOP THREE APPLICATIONS,

BY KEY PLAYER, 2023 99

6 CAPNOGRAPHY EQUIPMENT MARKET, BY PRODUCT 100

6.1 INTRODUCTION 101

6.2 EQUIPMENT 101

6.2.1 MULTIPARAMETER CAPNOMETERS 104

6.2.1.1 Handheld multiparameter capnometers 106

6.2.1.1.1 Improved patient safety, portability, and inbuilt audible and visual alarm to aid adoption 106

6.2.1.2 Conventional multiparameter capnometers 109

6.2.1.2.1 Increasing number of complex surgeries involving anesthesia to support segment growth 109

6.2.2 STANDALONE CAPNOMETERS 111

6.2.2.1 Handheld standalone capnometers 114

6.2.2.1.1 Increasing number of emergency care visits and complex surgeries to propel segment growth 114

6.2.2.2 Conventional standalone capnometers 116

6.2.2.2.1 Easy portability and use in critical care settings to boost segment growth 116

6.3 SOFTWARE 118

6.3.1 BETTER CLINICAL DECISION-MAKING AND PATIENT MANAGEMENT TO FUEL MARKET GROWTH 118

6.4 CAPNOGRAPHY ACCESSORIES & DISPOSABLES 121

6.4.1 FAVORABLE REIMBURSEMENT SCENARIO TO SUPPORT MARKET GROWTH 121

7 CAPNOGRAPHY EQUIPMENT MARKET, BY TECHNOLOGY 124

7.1 INTRODUCTION 125

7.2 MAINSTREAM CAPNOGRAPHY 125

7.2.1 HIGH ACCURACY, FAST RESPONSE TIME, AND IMPROVED SUITABILITY FOR NEONATES TO AID MARKET GROWTH 125

7.3 SIDE-STREAM CAPNOGRAPHY 128

7.3.1 RELIABLE MEASUREMENT OF END-TIDAL CO2 LEVELS TO PROPEL ADOPTION IN CLINICAL SETTINGS 128

7.4 MICROSTREAM CAPNOGRAPHY 130

7.4.1 LIMITATIONS IN BLACK-BODY INFRARED TECHNOLOGY TO LIMIT USAGE IN OPERATING ROOMS 130

8 CAPNOGRAPHY EQUIPMENT MARKET, BY APPLICATION 133

8.1 INTRODUCTION 134

8.2 CARDIAC CARE 134

8.2.1 INCREASING NUMBER OF CARDIOPULMONARY SURGERIES AND RISING PREFERENCE FOR MONITORING ETCO2 LEVELS TO DRIVE MARKET 134

8.3 TRAUMA & EMERGENCY CARE 137

8.3.1 INCREASING NUMBER OF ROAD ACCIDENTS TO SPUR MARKET GROWTH 137

8.4 RESPIRATORY MONITORING 139

8.4.1 RISING PREVALENCE OF TARGET RESPIRATORY CONDITIONS TO SUPPORT MARKET GROWTH 139

8.5 OTHER APPLICATIONS 142

9 CAPNOGRAPHY EQUIPMENT MARKET, BY END USER 145

9.1 INTRODUCTION 146

9.2 HOSPITALS 148

9.2.1 FOCUS ON REDUCING AIRWAY-RELATED DEATHS IN ICU PATIENTS TO ACCELERATE MARKET GROWTH 148

9.3 AMBULATORY SURGERY CENTERS & HOME CARE SETTINGS 151

9.3.1 INCREASING NUMBER OF REIMBURSEMENT-APPROVED MEDICAL PROCEDURES UNDER ASC PAYMENT SYSTEM TO DRIVE MARKET 151

9.4 OTHER END USERS 153

10 CAPNOGRAPHY EQUIPMENT MARKET, BY REGION 156

10.1 INTRODUCTION 157

10.2 NORTH AMERICA 157

10.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA 161

10.2.2 US 161

10.2.2.1 US to dominate North American capnography equipment market during forecast period 161

10.2.3 CANADA 164

10.2.3.1 Rising prevalence of target respiratory diseases to support market growth 164

10.3 EUROPE 167

10.3.1 MACROECONOMIC OUTLOOK FOR EUROPE 171

10.3.2 GERMANY 172

10.3.2.1 Developed healthcare infrastructure and high government investments to spur market growth 172

10.3.3 UK 175

10.3.3.1 Increasing target patient population and rising healthcare expenditure to propel market growth 175

10.3.4 FRANCE 177

10.3.4.1 Growing awareness of capnography monitoring procedures and increasing number of trauma cases to augment market growth 177

10.3.5 ITALY 180

10.3.5.1 Rise in diabetes cases and high geriatric population to boost market growth 180

10.3.6 SPAIN 183

10.3.6.1 Increasing prevalence of lifestyle diseases to drive demand for capnography equipment 183

10.3.7 REST OF EUROPE 185

10.4 ASIA PACIFIC 188

10.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC 193

10.4.2 JAPAN 193

10.4.2.1 Rising geriatric population and growing prevalence of obesity to augment market growth 193

10.4.3 CHINA 196

10.4.3.1 High target patient population and improved inpatient service availability to support market growth 196

10.4.4 INDIA 199

10.4.4.1 Favorable regulatory policies and high public healthcare expenditure to aid market growth 199

10.4.5 AUSTRALIA 202

10.4.5.1 Growing patient population and rising availability of grants to fuel market growth 202

10.4.6 SOUTH KOREA 205

10.4.6.1 Increased focus on R&D activities and high penetration of health insurance to propel market growth 205

10.4.7 REST OF ASIA PACIFIC 208

10.5 LATIN AMERICA 211

10.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA 214

10.5.2 BRAZIL 214

10.5.2.1 Improved healthcare sector and increased private-public investments to drive market 214

10.5.3 MEXICO 217

10.5.3.1 Favorable trade environment and easy entry of foreign players to fuel market growth 217

10.5.4 REST OF LATIN AMERICA 220

10.6 MIDDLE EAST & AFRICA 223

10.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA 226

10.6.2 GCC COUNTRIES 227

10.6.2.1 Healthcare infrastructural developments and increased focus on patient safety to drive market 227

10.6.3 REST OF MIDDLE EAST & AFRICA 230

11 COMPETITIVE LANDSCAPE 233

11.1 INTRODUCTION 233

11.2 KEY PLAYER STRATEGY/RIGHT TO WIN 233

11.2.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN CAPNOGRAPHY EQUIPMENT MARKET 234

11.3 REVENUE ANALYSIS, 2019–2023 235

11.4 MARKET SHARE ANALYSIS, 2023 237

11.4.1 RANKING OF KEY MARKET PLAYERS 238

11.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023 239

11.5.1 STARS 239

11.5.2 EMERGING LEADERS 239

11.5.3 PERVASIVE PLAYERS 239

11.5.4 PARTICIPANTS 239

11.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023 241

11.5.5.1 Company footprint 241

11.5.5.2 Product footprint 242

11.5.5.3 Technology footprint 242

11.5.5.4 Application footprint 243

11.5.5.5 End-user footprint 244

11.5.5.6 Region footprint 245

11.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023 246

11.6.1 PROGRESSIVE COMPANIES 246

11.6.2 RESPONSIVE COMPANIES 246

11.6.3 DYNAMIC COMPANIES 246

11.6.4 STARTING BLOCKS 246

11.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2023 248

11.7 COMPANY VALUATION & FINANCIAL METRICS 249

11.7.1 FINANCIAL METRICS 249

11.7.2 COMPANY VALUATION 249

11.8 BRAND/PRODUCT COMPARISON 250

11.9 COMPETITIVE SCENARIO 251

11.9.1 PRODUCT LAUNCHES AND APPROVALS 251

11.9.2 DEALS 252

12 COMPANY PROFILES 253

12.1 KEY PLAYERS 253

12.1.1 BECTON, DICKINSON AND COMPANY 253

12.1.1.1 Business overview 253

12.1.1.2 Products/Services/Solutions offered 254

12.1.1.3 MnM view 255

12.1.1.3.1 Right to win 255

12.1.1.3.2 Strategic choices 255

12.1.1.3.3 Weaknesses and competitive threats 255

12.1.2 MEDTRONIC 256

12.1.2.1 Business overview 256

12.1.2.2 Products/Services/Solutions offered 257

12.1.2.3 Recent developments 258

12.1.2.3.1 Product approvals 258

12.1.2.3.2 Deals 259

12.1.2.4 MnM view 259

12.1.2.4.1 Right to win 259

12.1.2.4.2 Strategic choices 259

12.1.2.4.3 Weaknesses and competitive threats 259

12.1.3 KONINKLIJKE PHILIPS N.V. 260

12.1.3.1 Business overview 260

12.1.3.2 Products/Services/Solutions offered 261

12.1.3.3 Recent developments 262

12.1.3.3.1 Deals 262

12.1.3.4 MnM view 263

12.1.3.4.1 Right to win 263

12.1.3.4.2 Strategic choices 263

12.1.3.4.3 Weaknesses and competitive threats 263

12.1.4 GE HEALTHCARE 264

12.1.4.1 Business overview 264

12.1.4.2 Products/Services/Solutions offered 265

12.1.4.3 Recent developments 266

12.1.4.3.1 Deals 266

12.1.4.4 MnM view 266

12.1.4.4.1 Right to win 266

12.1.4.4.2 Strategic choices 267

12.1.4.4.3 Weaknesses and competitive threats 267

12.1.5 DRÄGERWERK AG & CO. KGAA 268

12.1.5.1 Business overview 268

12.1.5.2 Products/Services/Solutions offered 269

12.1.5.3 MnM view 270

12.1.5.3.1 Right to win 270

12.1.5.3.2 Strategic choices 270

12.1.5.3.3 Weaknesses and competitive threats 270

12.1.6 NIHON KOHDEN CORPORATION 272

12.1.6.1 Business overview 272

12.1.6.2 Products/Services/Solutions offered 273

12.1.6.3 Recent developments 274

12.1.6.3.1 Deals 274

12.1.7 ZOLL MEDICAL CORPORATION 275

12.1.7.1 Business overview 275

12.1.7.2 Products/Services/Solutions offered 275

12.1.7.3 Recent developments 276

12.1.7.3.1 Deals 276

12.1.8 EDAN INSTRUMENTS, INC. 277

12.1.8.1 Business overview 277

12.1.8.2 Products/Services/Solutions offered 277

12.1.9 HAMILTON MEDICAL 278

12.1.9.1 Business overview 278

12.1.9.2 Products/Services/Solutions offered 278

12.1.9.3 Recent developments 279

12.1.9.3.1 Product launches 279

12.1.10 MASIMO 280

12.1.10.1 Business overview 280

12.1.10.2 Products/Services/Solutions offered 281

12.1.10.3 Recent developments 282

12.1.10.3.1 Product approvals 282

12.1.11 MINDRAY 283

12.1.11.1 Business overview 283

12.1.11.2 Products/Services/Solutions offered 284

12.1.11.3 Recent developments 285

12.1.11.3.1 Product launches 285

12.1.11.3.2 Deals 286

12.1.12 NONIN 287

12.1.12.1 Business overview 287

12.1.12.2 Products/Services/Solutions offered 287

12.1.12.3 Recent developments 288

12.1.12.3.1 Product launches 288

12.1.12.3.2 Deals 289

12.1.13 SCHILLER 290

12.1.13.1 Business overview 290

12.1.13.2 Products/Services/Solutions offered 290

12.1.14 AVANTE 291

12.1.14.1 Business overview 291

12.1.14.2 Products/Services/Solutions offered 291

12.1.15 ICU MEDICAL, INC. 293

12.1.15.1 Business overview 293

12.1.15.2 Products/Services/Solutions offered 295

12.1.15.3 Recent developments 295

12.1.15.3.1 Deals 295

12.2 OTHER PLAYERS 296

12.2.1 BIONICS CO., LTD. 296

12.2.2 BPL MEDICAL TECHNOLOGIES 297

12.2.3 BURTONS MEDICAL EQUIPMENT, LTD. 298

12.2.4 CRITICARE TECHNOLOGIES, INC. 299

12.2.5 DIAMEDICA (UK) LIMITED 300

12.2.6 INFINIUM MEDICAL 301

12.2.7 SPACELABS HEALTHCARE 302

12.2.8 NIDEK MEDICAL INDIA 303

12.2.9 RESMED 304

12.2.10 RECORDERS & MEDICARE SYSTEMS PVT. LTD. 305

12.2.11 SHENZHEN COMEN MEDICAL INSTRUMENTS CO., LTD. 306

12.2.12 SLE LTD. 307

12.2.13 ZOE MEDICAL 308

12.2.14 EMCO MEDITEK PVT. LTD. 309

12.2.15 MONARCH MEDITECH 310

13 APPENDIX 311

13.1 DISCUSSION GUIDE 311

13.2 KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL 316

13.3 CUSTOMIZATION OPTIONS 318

13.4 RELATED REPORTS 318

13.5 AUTHOR DETAILS 319

❖ 世界のカプノグラフィ装置市場に関するよくある質問(FAQ) ❖

・カプノグラフィ装置の世界市場規模は?

→MarketsandMarkets社は2024年のカプノグラフィ装置の世界市場規模を3億7420万米ドルと推定しています。

・カプノグラフィ装置の世界市場予測は?

→MarketsandMarkets社は2029年のカプノグラフィ装置の世界市場規模を4億5880万米ドルと予測しています。

・カプノグラフィ装置市場の成長率は?

→MarketsandMarkets社はカプノグラフィ装置の世界市場が2024年~2029年に年平均4.2%成長すると予測しています。

・世界のカプノグラフィ装置市場における主要企業は?

→MarketsandMarkets社は「Becton, Dickinson and company (US), Medtronic (US), Koninklijke Philips N.V.(Netherlands), GE Healthcare (US), Drägerwerk AG (Germany), Nihon Kohden (Japan), Zoll Medical (US), Edan Instruments Inc (China), Hamilton Medical (Switzerland ), Masimo Corporation (US), Mindray (China)など ...」をグローバルカプノグラフィ装置市場の主要企業として認識しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、納品レポートの情報と少し異なる場合があります。