1 はじめに 27

1.1 調査目的 27

1.2 市場の定義 27

1.3 調査範囲 28

1.3.1 対象市場と地域範囲 28

1.3.2 考慮した年数 29

1.3.3 対象範囲と除外項目 29

1.4 考慮した通貨 30

1.5 考慮した単位 30

1.6 制限事項 30

1.7 利害関係者 30

1.8 変更点のまとめ 31

2 調査方法 32

2.1 調査データ 32

2.1.1 二次データ 33

2.1.1.1 主な二次情報源 34

2.1.1.2 二次資料からの主要データ 34

2.1.2 一次データ 34

2.1.2.1 一次面接の対象者 35

2.1.2.2 主要な一次インタビュー参加者 35

2.1.2.3 プライマリーの内訳 35

2.1.2.4 主要な業界インサイト 36

2.1.2.5 一次情報源からの主要データ 37

2.1.3 二次調査および一次調査 38

2.2 市場規模の推定 38

2.2.1 ボトムアップアプローチ 39

2.2.1.1 ボトムアップアプローチによる市場規模の推定 39

2.2.2 トップダウンアプローチ 40

2.2.2.1 市場規模推定のためのトップダウンアプローチ 40

2.3 市場の内訳とデータの三角測量 42

2.4 リサーチの前提 43

2.5 調査の限界 43

2.6 リスク評価 43

3 エグゼクティブサマリー 44

4 プレミアムインサイト 48

4.1 産業用撹拌機市場におけるプレーヤーの魅力的な機会 48

4.2 工業用撹拌機市場:モデルタイプ別 48

4.3 工業用攪拌機市場:取り付けタイプ別 49

4.4 工業用撹拌機市場:形状別 49

4.5 工業用撹拌機市場:地域別 50

5 市場の概要 51

5.1 はじめに 51

5.2 市場ダイナミクス 51

5.2.1 推進要因 52

5.2.1.1 排水処理の効率的な実施に対するニーズの高まり 53

5.2.1.2 エネルギー効率、流量の最大化、急速混合、廃棄物削減に対する需要の高まり 53

5.2.1.3 プロセス及び製造業の力強い成長 54

5.2.1.4 カスタマイズされた工業用撹拌機に対する需要の増加 54

5.2.1.5 自動化とスマート技術の進歩 54

5.2.1.6 食品・飲料産業の拡大と衛生順守の必要性 55

5.2.2 阻害要因 55

5.2.2.1 メンテナンスと修理の高コスト 55

5.2.2.2 カスタム機器のリードタイムの長さ 56

5.2.3 機会 57

5.2.3.1 複数の用途における混合技術の利用の拡大 57

5.2.3.2 予知保全のためのIoTとデータ分析の統合 57

5.2.4 課題 58

5.2.4.1 政府の厳しい安全規範と製品コンプライアンス基準 58

5.2.4.2 高コストまたは限定的な使用による撹拌機/ミキサー機器のリース傾向の台頭 59

5.2.4.3 低コストメーカーとの競争の激化 59

5.3 バリューチェーン分析 59

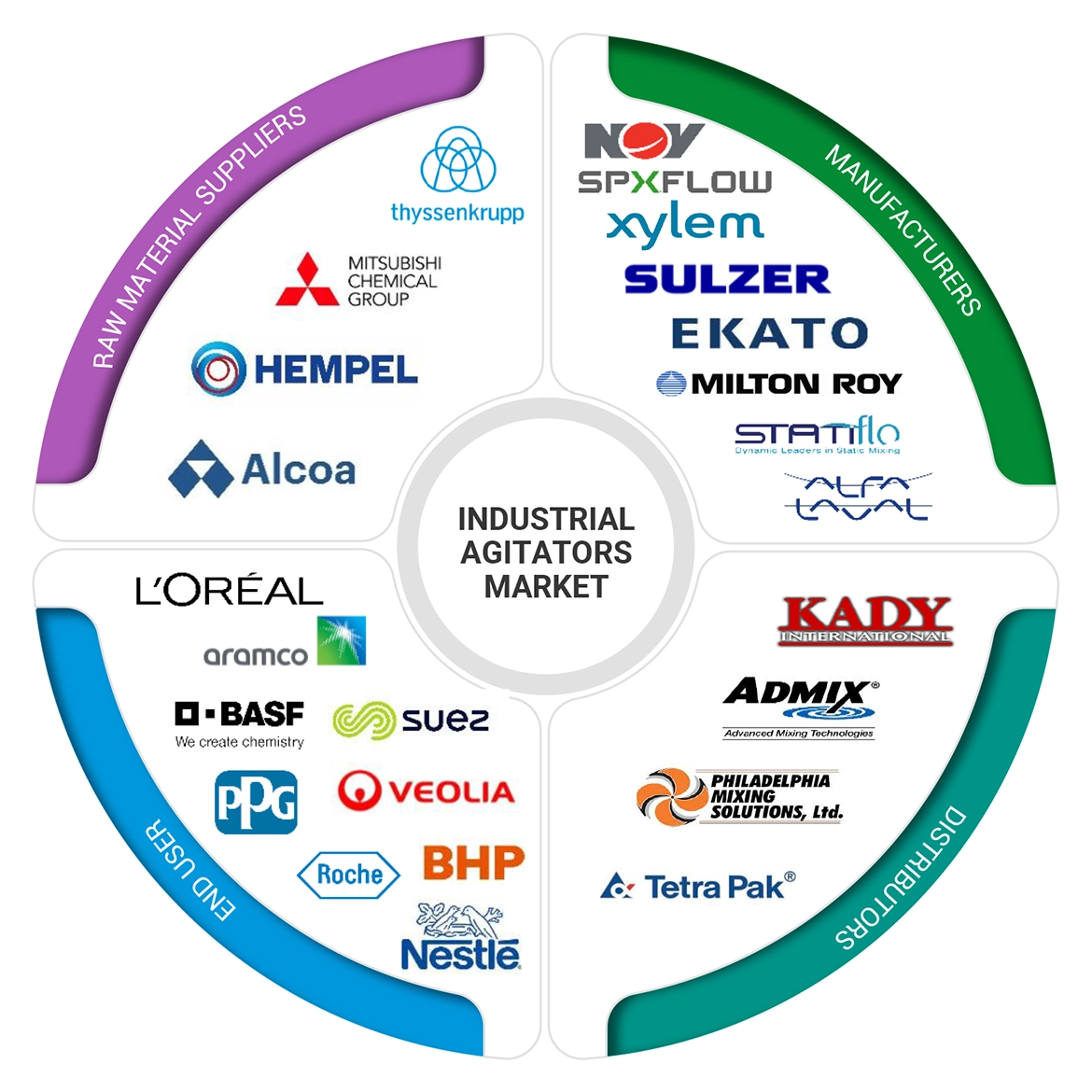

5.4 エコシステム分析 61

5.5 投資と資金調達のシナリオ 63

5.6 顧客ビジネスに影響を与えるトレンド/混乱 63

5.7 価格分析 64

5.7.1 工業用撹拌機の主要メーカー別平均販売価格 65

5.7.2 工業用攪拌機の指標価格(主要プレーヤー別) 66

5.8 技術分析 66

5.8.1 主要技術 66

5.8.1.1 混合ブレードとインペラ 66

5.8.1.2 可変速ドライブ(VSD) 66

5.8.1.3 制御システム(PLC と HMI) 67

5.8.2 補足技術 67

5.8.2.1 センサー(温度、圧力、粘度) 67

5.8.2.2 熱交換器 67

5.8.2.3 マテリアルハンドリングシステム 67

5.8.2.4 CIP(定置洗浄)システム 67

5.8.3 隣接技術 68

5.8.3.1 オートメーションとロボット工学 68

5.8.3.2 モノの産業用インターネット(IIoT) 68

5.9 産業用撹拌機市場におけるAIの影響 68

5.9.1 導入 68

5.9.2 ケーススタディ 69

5.10 ポーターの5つの力分析 70

5.10.1 競争相手の強さ 71

5.10.2 供給者の交渉力 71

5.10.3 買い手の交渉力 71

5.10.4 新規参入の脅威 72

5.10.5 代替品の脅威 72

5.11 主要ステークホルダーと購買基準 72

5.11.1 購入プロセスにおける主要ステークホルダー 72

5.11.2 購入基準 73

5.12 ケーススタディ分析 74

5.12.1 タクミナコーポレーションの連続混合システムは生産とコーティングの精度を向上 74

5.12.2 Spx Flow 社の mmr プログラムによる時間短縮と効率改善 74

5.12.3 xylem 社、生産強化と廃棄物処理の簡素化のために鉱山会社にミキサーとポンプを提供 75

5.13 貿易分析 75

5.13.1 輸入シナリオ(HS コード 847982) 75

5.13.2 輸出シナリオ(HSコード847982) 76

5.14 関税と規制の状況 77

5.14.1 関税分析 77

5.14.2 規制機関、政府機関、その他の組織 78

5.14.3 規格 81

5.15 特許分析 82

5.16 主要な会議とイベント(2024-2025年) 84

6 工業用撹拌機の流通チャネル 85

6.1 はじめに 85

6.2 直接チャネル 86

6.2.1 高収益のために大手企業が採用する直接販売チャネル 86

6.3 間接チャネル 86

6.3.1 代理店や仲介業者を通じた販売増加に対する世界的需要の高まり 86

7 工業用撹拌機の定格出力 88

7.1 導入 88

7.2 50 馬力未満 88

7.2.1 主に小/中タンクサイズの中規模運転で使用 88

7.3 50~100 馬力 89

7.3.1 大規模で要求の厳しい工業プロセスにおける需要が市場を牽引 89

7.4 100 馬力以上 89

7.4.1 主に化学、製薬産業で使用 89

8 工業用撹拌機の用途 90

8.1 導入 90

8.2 ホモジナイゼーション 90

8.3 懸濁 91

8.4 乳化 91

8.5 分散 92

8.6 中和 92

8.7 結晶化 93

8.8 発酵 93

8.9 煙道ガス脱硫(FGD) 94

9 工業用撹拌機市場、コンポーネント別 95

9.1 導入 96

9.2 頭部 97

9.2.1 化学・製薬産業における撹拌機需要の増加が市場を牽引 97

9.3 シールシステム 98

9.3.1 撹拌中の汚染を最小限に抑え、滑らかな動きを強化 98

9.4 羽根車 98

9.4.1 効率の達成には適切なインペラの選択が重要 98

9.5 その他の部品 99

10 工業用撹拌機市場、モデルタイプ別 100

10.1 導入 101

10.2 大型タンク用撹拌機 103

10.2.1 効率的な大量混合と連続運転の必要性の高まりが市場を牽引 103

10.3 ポータブル撹拌機 104

10.3.1 食品・飲料産業における混合・ブレンド用途の高い需要が市場を牽引 104

10.4 ドラム型撹拌機 106

10.4.1 製品の均一性を高め、廃棄物の最小化を可能にするニーズが市場成長を促進 106

10.5 その他のモデルタイプ 107

11 工業用撹拌機市場:形態別 108

11.1 導入 109

11.2 固体-固体混合物 110

11.2.1 医薬品産業におけるバルク混合への要求が市場を牽引 110

11.3 固液混合 111

11.3.1 固液混合物におけるトラブルのない湿潤と分散への需要の高まりが市場を牽引 111

11.4 液体-気体混合物 113

11.4.1 化学・生物学的プロセス技術における需要の増加が市場を牽引 113

11.5 液体-液体混合物 114

11.5.1 化学、食品・飲料、製薬産業での使用の増加が市場を牽引 114

12 工業用攪拌機市場(取り付け部別) 115

12.1 導入 116

12.2 トップマウント型撹拌機 118

12.2.1 様々な産業用途における高粘度流体の混合需要の増加が市場を牽引 118

12.3 横置き型撹拌機 120

12.3.1 生産と製品品質向上のための既存システムへの容易な統合が需要を牽引 120

12.4 底面設置型撹拌機 122

12.4.1 化学・バイオ産業における混合・ブレンドのニーズが市場成長を促進 122

13 工業用撹拌機市場:最終用途産業別 124

13.1 導入 125

13.2 化学 127

13.2.1 石油産業 127

13.2.1.1 石油・石油産業における泥の混合、原油の抽出、精製に利用される撹拌機 127

13.2.1.2 乳化 128

13.2.1.3 原油処理 128

13.2.1.4 液体とガスの混合 128

13.2.1.5 ガス分散・吸収 129

13.2.2 水・廃水処理 129

13.2.2.1 排水処理ニーズの増加と水浄化プロセスの改善が需要を牽引 129

13.2.2.2 ガス分散・吸収 129

13.2.2.3 洗浄と浸出 130

13.3 鉱業 134

13.3.1 水冶金プロセスおよび常圧浸出用途で使用されるようになっている攪拌機 134

13.3.2 浸出 135

13.3.3 スラリーの混合 135

13.3.4 選鉱 135

13.3.5 浮遊プロセス 135

13.3.6 シアン化 135

13.3.7 沈殿反応 135

13.3.8 カーボン・イン・パルプ(Cip)及びカーボン・イン・リーチ(Cil) 135

13.4 食品と飲料 140

13.4.1 効率的な食品・飲料加工に対する需要の高まりが需要を牽引 140

13.4.2 混合及びブレンド 140

13.4.3 発酵 141

13.4.4 均質化 141

13.4.5 糖類及び塩類の溶解 141

13.4.6 エアレーション 141

13.4.7 香料および添加物の混合 141

13.5 医薬品 147

13.5.1 錠剤の造粒やシロップの混合に広く使用される撹拌機 147

13.5.2 医薬品有効成分(アピス) 147

13.5.3 液剤の調製 147

13.5.4 ワクチン製造 147

13.5.5 抗生物質製造 147

13.5.6 制御放出製剤 148

13.5.7 無菌混合 148

13.6 化粧品 153

13.6.1 乳化、粉体ウェットアウト、粒径低減のために化粧品産業で使用される撹拌機 153

13.6.2 ゲルの混合 153

13.6.3 色材分散 154

13.6.4 エアゾール推進剤の混合 154

13.6.5 粘度調整 154

13.6.6 固形成分の懸濁 154

13.6.7 化粧品成分の活性化 154

13.6.8 外用剤の混合 154

13.6.9 充填及び包装補助 154

13.7 塗料およびコーティング 159

13.7.1 塗料配合の複雑さを最小限に抑え、高品質の塗膜を確保するための支援 159

13.7.2 顔料分散 159

13.7.3 エマルション形成 159

13.7.4 粘度調整 160

13.7.5 重合 160

13.7.6 溶媒混合 160

13.7.7 充填剤の配合 160

13.7.8 粉体塗料の混合 160

13.7.9 スプレー塗装の準備 160

13.7.10 塗料のリサイクル 160

13.7.11 化学反応管理 161

13.7.12 バッチミキシング 161

13.7.13 添加剤混合 161

13.8 その他の最終用途産業 166

14 工業用撹拌機市場、地域別 172

14.1 はじめに 173

14.2 北米 175

14.2.1 北米のマクロ経済見通し 177

14.2.2 米国 177

14.2.2.1 化学産業と食品・飲料産業の成長が成長を牽引 177

14.2.3 カナダ 177

177 14.2.3.1 政府による化学産業への注力で撹拌機需要が増加 177

14.2.4 メキシコ 178

14.2.4.1 構造改革が様々なセクターの成長を促進 178

14.3 欧州 178

14.3.1 欧州のマクロ経済見通し 181

14.3.2 イギリス 181

14.3.2.1 製薬・化学産業における研究開発活動の急増が需要を促進 181

14.3.3 ドイツ 181

14.3.3.1 化学、製薬、塗料・コーティング産業からの需要が市場を牽引 181

14.3.4 フランス 182

14.3.4.1 化学産業の急増が市場成長を支える 182

14.3.5 その他の欧州 182

14.4 アジア太平洋 183

14.4.1 アジア太平洋地域のマクロ経済見通し 185

14.4.2 中国 185

14.4.2.1 国内化学製造業が市場プレーヤーに機会を提供 185

14.4.3 日本 186

14.4.3.1 特殊化学品へのパラダイムシフトが工業用撹拌機の需要を押し上げる 186

14.4.4 インド 186

14.4.4.1 政府の自給自足計画と様々な分野での拡大が需要を増加 186

14.4.5 その他のアジア太平洋地域 186

14.5 その他の地域 187

14.5.1 行のマクロ経済見通し 188

14.5.2 南米 188

14.5.2.1 食品・飲料業界が産業用撹拌機の需要を促進 188

14.5.3 中東 189

14.5.3.1 石油需要の急増が市場成長を支える 189

14.5.4 アフリカ 189

14.5.4.1 鉱業が産業用撹拌機の重要なエンドユーザーになる 189

15 競争環境 190

15.1 概要 190

15.2 主要企業の戦略/勝利への権利(2021~2024年) 190

15.3 収益分析、2019年~2023年 191

15.4 市場シェア分析、2023年 192

15.5 企業評価と財務指標 194

15.6 ブランド/製品の比較 195

15.7 企業評価マトリックス:主要企業、2023年 195

15.7.1 スター企業 195

15.7.2 新興リーダー 196

15.7.3 浸透型プレーヤー 196

15.7.4 参加企業 196

15.7.5 企業フットプリント:主要プレイヤー(2023年) 197

15.7.5.1 企業フットプリント 197

15.7.5.2 地域別フットプリント 198

15.7.5.3 モデルタイプのフットプリント 199

15.7.5.4 取り付けフットプリント 200

15.7.5.5 最終用途産業のフットプリント 201

15.8 企業評価マトリクス:新興企業/SM(2023年) 202

15.8.1 進歩的企業 202

15.8.2 対応力のある企業 202

15.8.3 ダイナミックな企業 202

15.8.4 スタートアップ・ブロック 202

15.8.5 競争ベンチマーキング(新興企業/SM)(2023年) 204

15.8.5.1 主要新興企業/中小企業の詳細リスト 204

15.8.5.2 主要新興企業/SMEの競争ベンチマーク 204

15.9 競争シナリオ 205

15.9.1 製品上市 205

15.9.2 取引 206

15.9.3 拡張 207

15.9.4 その他 208

16 企業プロフィール 209

16.1 主要企業 209

SPX Flow Inc. (US)

Xylem Inc. (US)

Ekato Group (Germany)

Sulzer Ltd. (Switzerland) and NOV Inc (US)

17 付録 251

17.1 業界の専門家による洞察 251

17.2 ディスカッションガイド 252

17.3 Knowledgestore: マーケットサ ンドマーケッツの購読ポータル 256

17.4 カスタマイズオプション 258

17.5 関連レポート 258

17.6 著者の詳細 259

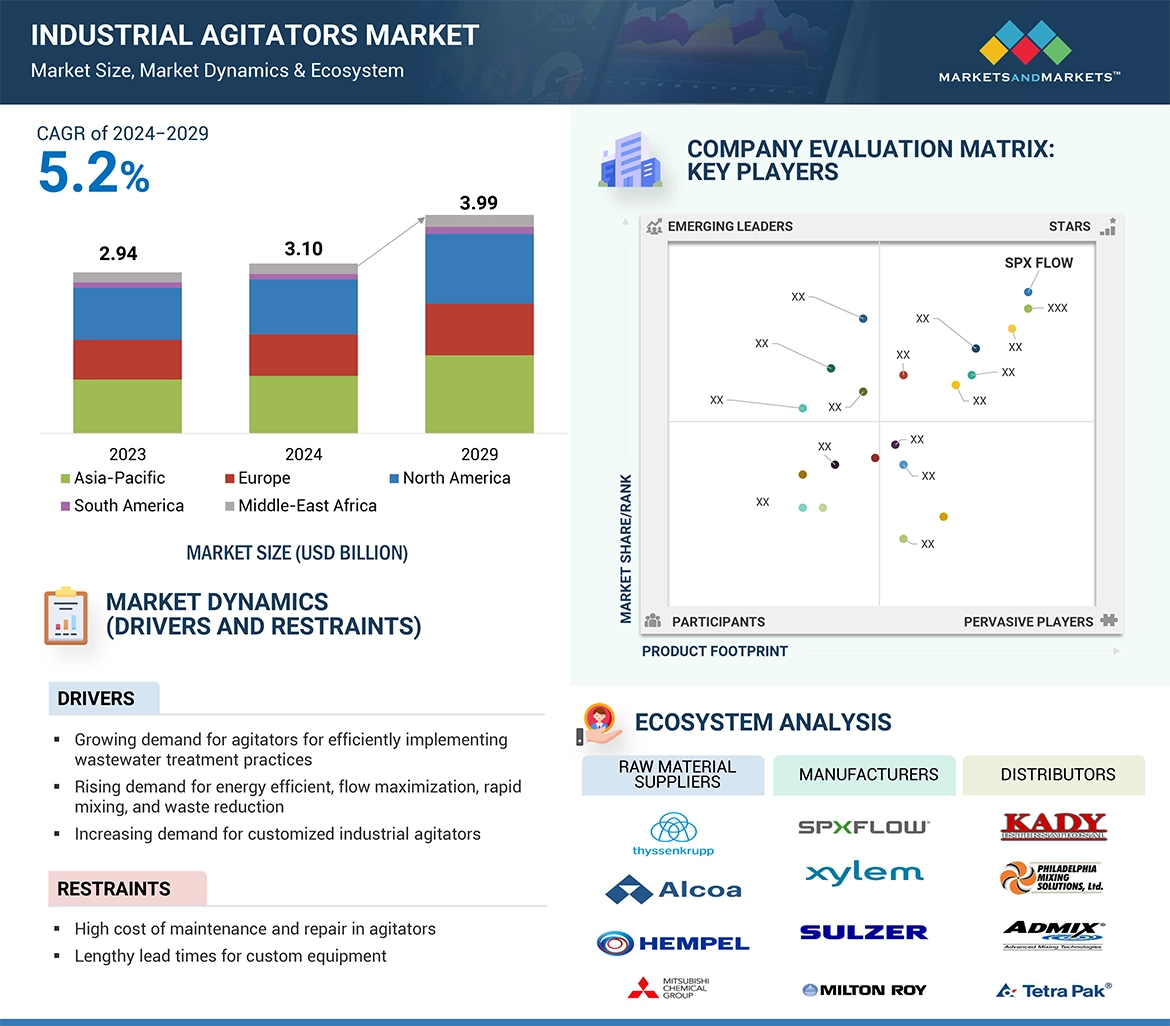

Rising urbanization, regulatory requirements, technological advancements have led to the development of highly efficient agitators designed to handle varying viscosities and densities, further driving their adoption of agitators in mixing processes. The rising focus on energy efficiency and process optimization has also boosted demand, as modern agitators are engineered to reduce power consumption while maintaining superior performance.t.

“Large Tank agitators to contribute significant share in industrial agitators market.”

Large tank agitators are used in large-scale industrial processes which demand consistent and efficient mixing. Therefore, significant share is expected to be contributed by large tank agitators. The large tank agitators are used in chemicals, oil and gas, food and beverages, and wastewater treatment, all of which rely on large tank agitators for handling high volumes of materials and ensuring uniformity in large storage vessels or reactors. These agitators are particularly needed for those more ordinary bulk processing applications like liquid homogenizing, additive mixing and suspension of solids.Large tank agitators are particularly very effective in operations involving high-viscosity fluids, considerable volumes of chemical solution, and long fermentation processes where other types of agitators may not adequately perform. Their capability to provide strong, reliable mixing ensures optimum chemical reactions, enhances heat transfer, and ensures prevention from sedimentation in the storage tank, all leading to operational efficiency and quality of product. Indicative of the growing demand for large-scale production in the food and beverage manufacturing, chemical processing, and energy production industries, among other sectors, while technological innovations prop up the design of energy-efficient and automated systems, the large tank agitators segment is driven further.

“Top-mounted to grow significantly in the industrial agitators market.”

In 2023, the top-mounted segment accounted for a larger market share, and a similar trend is likely to be observed during the forecast period, as the use of industrial agitators systems is on the rise in newly emerging applications such as cosmetics, pharmaceuticals and so on. Top-mounted agitators are also expected to contribute well to the industrial agitators market because of their applications that require efficient, high-performance mixing in various industries such as chemicals, pharmaceuticals, food and beverages, and water treatment, among others. The advantages these agitators possess include their ability to handle a broad range of fluid viscosities and densities, thereby achieving both light and heavy-duty applications. Their top-mounted design also affords easy installation and service while ensuring consistent mixing in large-scale production operations.

The critical need in industry, particularly in pharmaceuticals and food processing, to meet the strict quality standards can be achieved through good chemical reactions, efficient heat transfer, and product uniformity. Thus, there would be a growth in demand for energy-efficient, customizable, and durable mixing solutions that will lend to the high adoption rate of top-mounted agitators, keeping them at a considerable share in the global industrial agitators market.

“Asia Pacific will contribute significantly to the growth rate in industrial agitators market.”

Asia Pacific is poised to contribute a significant share to the industrial agitators market for several compelling reasons, by increasing adoption of energy-efficient technologie in Asia Pacific countries due to environmental regulations and more awareness towards sustainable practices. The Asia Pacific region is estimated to be the largest market for industrial agitators. The region has a good contribution because of the synergy of rapid industrialization, urbanization, as well as the growing demand for pharmaceuticals and chemical industry. It is also projected to be the fastest-growing market during the forecast period. Asia-Pacific has a strong industrial base in chemicals, food and beverage, and pharmaceuticals, which fuels demand for agitators. This raises a need for advanced mixing equipment for blending and suspension processes generates growth in the demand for such equipment.

In-depth interviews have been conducted with chief executive officers (CEOs), Directors, and other executives from various key organizations operating in the industrial agitators market place.

• By Company Type: Tier 1 – 40%, Tier 2 – 35%, and Tier 3 – 25%

• By Designation: C-level Executives – 48%, Directors – 33%, and Others – 19%

• By Region: North America– 35%, Europe – 18%, Asia Pacific– 40% and RoW- 7%

The study includes an in-depth competitive analysis of these key players in the industrial agitators market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the industrial agitators market by type, form, mounting, component, industry and region (North America, Europe, Asia Pacific). The report scope covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the industrial agitators market. A detailed analysis of the key industry players has provided insights into their business overview, solutions and services, key strategies, Contracts, partnerships, and agreements. New product and service launches, acquisitions, and recent developments associated with the industrial agitators market. This report covers competitive analysis of upcoming startups in the industrial agitators market ecosystem.

Reasons to buy this report

The report will help the market leaders/new entrants with information on the closest approximations of the revenue numbers for the industrial agitators market, and subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

• Analysis of key drivers (Growing demand for agitators for efficiently implementing wastewater treatment practices, Rising demand for energy efficient, flow maximization, rapid mixing, and waste reduction, Robust growth of process and manufacturing industries, Increasing demand for customized industrial agitators, Advancements in automation and smart technologies in agitators

Expansion of food & beverage industry and demand for hygiene compliance), restraints (High cost of maintenance and repair in agitators, Lengthy lead times for custom equipment), opportunities (Growing use of mixing technologies in multiple applicationsIntegration of IoT and data analytics for predictive maintenance), and challenges (Stringent government safety norms and product compliance standards, Emerging trend of agitators/mixer equipment leasing due to high cost or limited usage, Increasing competition from low-cost manufacturers) influencing the growth of the industrial agitators market.

• Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the industrial agitators market

• Market Development: Comprehensive information about lucrative markets – the report analyses the industrial agitators market across varied regions.

• Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the industrial agitators market

• Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like as SPX Flow, Inc. (US), Xylem Inc. (US), Ekato Group (Germany), Sulzer Ltd. (Switzerland) and NOV Inc (US) among others in the industrial agitators market.

1 INTRODUCTION 27

1.1 STUDY OBJECTIVES 27

1.2 MARKET DEFINITION 27

1.3 STUDY SCOPE 28

1.3.1 MARKETS COVERED AND REGIONAL SCOPE 28

1.3.2 YEARS CONSIDERED 29

1.3.3 INCLUSIONS AND EXCLUSIONS 29

1.4 CURRENCY CONSIDERED 30

1.5 UNITS CONSIDERED 30

1.6 LIMITATIONS 30

1.7 STAKEHOLDERS 30

1.8 SUMMARY OF CHANGES 31

2 RESEARCH METHODOLOGY 32

2.1 RESEARCH DATA 32

2.1.1 SECONDARY DATA 33

2.1.1.1 Key secondary sources 34

2.1.1.2 Key data from secondary sources 34

2.1.2 PRIMARY DATA 34

2.1.2.1 Intended participants in primary interviews 35

2.1.2.2 Key primary interview participants 35

2.1.2.3 Breakdown of primaries 35

2.1.2.4 Key industry insights 36

2.1.2.5 Key data from primary sources 37

2.1.3 SECONDARY AND PRIMARY RESEARCH 38

2.2 MARKET SIZE ESTIMATION 38

2.2.1 BOTTOM-UP APPROACH 39

2.2.1.1 Bottom-up approach for estimating market size 39

2.2.2 TOP-DOWN APPROACH 40

2.2.2.1 Top-down approach for estimating market size 40

2.3 MARKET BREAKDOWN AND DATA TRIANGULATION 42

2.4 RESEARCH ASSUMPTIONS 43

2.5 RESEARCH LIMITATIONS 43

2.6 RISK ASSESSMENT 43

3 EXECUTIVE SUMMARY 44

4 PREMIUM INSIGHTS 48

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN INDUSTRIAL AGITATORS MARKET 48

4.2 INDUSTRIAL AGITATORS MARKET, BY MODEL TYPE 48

4.3 INDUSTRIAL AGITATORS MARKET, BY MOUNTING 49

4.4 INDUSTRIAL AGITATORS MARKET, BY FORM 49

4.5 INDUSTRIAL AGITATORS MARKET, BY REGION 50

5 MARKET OVERVIEW 51

5.1 INTRODUCTION 51

5.2 MARKET DYNAMICS 51

5.2.1 DRIVERS 52

5.2.1.1 increasing need for efficient implementation of wastewater treatment practices 53

5.2.1.2 Rising demand for energy efficiency, flow maximization, rapid mixing, and waste reduction 53

5.2.1.3 Strong growth of process and manufacturing industries 54

5.2.1.4 Increasing demand for customized industrial agitators 54

5.2.1.5 Advancements in automation and smart technologies 54

5.2.1.6 Expansion of food & beverage industry and need for hygiene compliance 55

5.2.2 RESTRAINTS 55

5.2.2.1 High cost of maintenance and repair 55

5.2.2.2 Lengthy lead times for custom equipment 56

5.2.3 OPPORTUNITIES 57

5.2.3.1 Growing use of mixing technologies in multiple applications 57

5.2.3.2 Integration of IoT and data analytics for predictive maintenance 57

5.2.4 CHALLENGES 58

5.2.4.1 Stringent government safety norms and product compliance standards 58

5.2.4.2 Emerging trend of agitators/mixer equipment leasing due to high cost or limited usage 59

5.2.4.3 Increasing competition from low-cost manufacturers 59

5.3 VALUE CHAIN ANALYSIS 59

5.4 ECOSYSTEM ANALYSIS 61

5.5 INVESTMENT AND FUNDING SCENARIO 63

5.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS 63

5.7 PRICING ANALYSIS 64

5.7.1 AVERAGE SELLING PRICE OF INDUSTRIAL AGITATORS, BY KEY PLAYERS 65

5.7.2 INDICATIVE PRICING OF INDUSTRIAL AGITATORS, BY KEY PLAYERS 66

5.8 TECHNOLOGY ANALYSIS 66

5.8.1 KEY TECHNOLOGIES 66

5.8.1.1 Mixing blades and impellers 66

5.8.1.2 Variable speed drives (VSD) 66

5.8.1.3 Control systems (PLC and HMI) 67

5.8.2 COMPLEMENTARY TECHNOLOGIES 67

5.8.2.1 Sensors (temperature, pressure, viscosity) 67

5.8.2.2 Heat exchangers 67

5.8.2.3 Material handling systems 67

5.8.2.4 Cleaning-in-place (CIP) systems 67

5.8.3 ADJACENT TECHNOLOGIES 68

5.8.3.1 Automation and robotics 68

5.8.3.2 Industrial Internet of Things (IIoT) 68

5.9 IMPACT OF AI ON INDUSTRIAL AGITATORS MARKET 68

5.9.1 INTRODUCTION 68

5.9.2 CASE STUDIES 69

5.10 PORTER'S FIVE FORCES ANALYSIS 70

5.10.1 INTENSITY OF COMPETITIVE RIVALRY 71

5.10.2 BARGAINING POWER OF SUPPLIERS 71

5.10.3 BARGAINING POWER OF BUYERS 71

5.10.4 THREAT OF NEW ENTRANTS 72

5.10.5 THREAT OF SUBSTITUTES 72

5.11 KEY STAKEHOLDERS AND BUYING CRITERIA 72

5.11.1 KEY STAKEHOLDERS IN BUYING PROCESS 72

5.11.2 BUYING CRITERIA 73

5.12 CASE STUDY ANALYSIS 74

5.12.1 TACMINA CORPORATION'S CONTINUOUS MIXING SYSTEM ENHANCES PRODUCTION AND COATING ACCURACY 74

5.12.2 SPX FLOW'S MMR PROGRAM OFFERS TIME REDUCTION AND IMPROVEMENT IN EFFICIENCY 74

5.12.3 XYLEM OFFERED MIXER AND PUMP TO MINING COMPANY FOR ENHANCED PRODUCTION AND SIMPLIFIED WASTE DISPOSAL 75

5.13 TRADE ANALYSIS 75

5.13.1 IMPORT SCENARIO (HS CODE 847982) 75

5.13.2 EXPORT SCENARIO (HS CODE 847982) 76

5.14 TARIFF AND REGULATORY LANDSCAPE 77

5.14.1 TARIFF ANALYSIS 77

5.14.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS 78

5.14.3 STANDARDS 81

5.15 PATENT ANALYSIS 82

5.16 KEY CONFERENCES AND EVENTS, 2024–2025 84

6 DISTRIBUTION CHANNELS FOR INDUSTRIAL AGITATORS 85

6.1 INTRODUCTION 85

6.2 DIRECT CHANNELS 86

6.2.1 DIRECT DISTRIBUTION CHANNELS ADOPTED BY MAJOR COMPANIES FOR HIGHER PROFITS 86

6.3 INDIRECT CHANNELS 86

6.3.1 RISING GLOBAL DEMAND TO INCREASE SALES THROUGH DISTRIBUTORS AND INTERMEDIARIES 86

7 POWER RATINGS OF INDUSTRIAL AGITATORS 88

7.1 INTRODUCTION 88

7.2 LESS THAN 50 HP 88

7.2.1 USED PRIMARILY IN MEDIUM-SCALE OPERATIONS WITH SMALL/MEDIUM TANK SIZES 88

7.3 50 TO 100 HP 89

7.3.1 DEMAND IN LARGE-SCALE AND DEMANDING INDUSTRIAL PROCESSES TO DRIVE MARKET 89

7.4 MORE THAN 100 HP 89

7.4.1 MOSTLY USED IN CHEMICALS AND PHARMACEUTICAL INDUSTRIES 89

8 APPLICATIONS OF INDUSTRIAL AGITATORS 90

8.1 INTRODUCTION 90

8.2 HOMOGENIZATION 90

8.3 SUSPENSION 91

8.4 EMULSIFICATION 91

8.5 DISPERSION 92

8.6 NEUTRALIZATION 92

8.7 CRYSTALLIZATION 93

8.8 FERMENTATION 93

8.9 FLUE GAS DESULFURIZATION (FGD) 94

9 INDUSTRIAL AGITATORS MARKET, BY COMPONENT 95

9.1 INTRODUCTION 96

9.2 HEADS 97

9.2.1 RISING DEMAND FOR AGITATORS IN CHEMICAL AND PHARMACEUTICAL INDUSTRIES TO DRIVE MARKET 97

9.3 SEALING SYSTEMS 98

9.3.1 ENHANCES SMOOTH MOVEMENT WITH MINIMUM CONTAMINATION DURING AGITATION 98

9.4 IMPELLERS 98

9.4.1 SELECTION OF APPROPRIATE IMPELLER CRITICAL FOR ACHIEVING EFFICIENCY 98

9.5 OTHER COMPONENTS 99

10 INDUSTRIAL AGITATORS MARKET, BY MODEL TYPE 100

10.1 INTRODUCTION 101

10.2 LARGE TANK AGITATORS 103

10.2.1 RISING NEED TO ENSURE EFFICIENT HEAVY MIXING WITH CONTINUOUS OPERATION TO DRIVE MARKET 103

10.3 PORTABLE AGITATORS 104

10.3.1 HIGH DEMAND FOR MIXING AND BLENDING APPLICATIONS IN FOOD & BEVERAGE INDUSTRY TO DRIVE MARKET 104

10.4 DRUM AGITATORS 106

10.4.1 NEED TO ENHANCE PRODUCT UNIFORMITY AND ENABLE WASTE MINIMIZATION TO FUEL MARKET GROWTH 106

10.5 OTHER MODEL TYPES 107

11 INDUSTRIAL AGITATORS MARKET, BY FORM 108

11.1 INTRODUCTION 109

11.2 SOLID–SOLID MIXTURE 110

11.2.1 REQUIREMENT FOR BULK MIXING IN PHARMACEUTICAL INDUSTRY TO DRIVE MARKET 110

11.3 SOLID–LIQUID MIXTURE 111

11.3.1 GROWING DEMAND FOR TROUBLE-FREE WETTING AND DISPERSION IN SOLID–LIQUID MIXTURE TO DRIVE MARKET 111

11.4 LIQUID–GAS MIXTURE 113

11.4.1 GROWING DEMAND IN CHEMICAL AND BIOLOGICAL PROCESS TECHNOLOGIES TO DRIVE MARKET 113

11.5 LIQUID–LIQUID MIXTURE 114

11.5.1 INCREASING USAGE IN CHEMICAL, FOOD & BEVERAGE, AND PHARMACEUTICAL INDUSTRIES TO DRIVE MARKET 114

12 INDUSTRIAL AGITATORS MARKET, BY MOUNTING 115

12.1 INTRODUCTION 116

12.2 TOP-MOUNTED AGITATORS 118

12.2.1 INCREASING DEMAND FOR MIXING OF HIGH-VISCOSITY FLUIDS IN VARIOUS INDUSTRIAL APPLICATIONS TO DRIVE MARKET 118

12.3 SIDE-MOUNTED AGITATORS 120

12.3.1 EASY INTEGRATION INTO EXISTING SYSTEMS FOR ENHANCEMENT OF PRODUCTION AND PRODUCT QUALITY TO DRIVE DEMAND 120

12.4 BOTTOM-MOUNTED AGITATORS 122

12.4.1 NEED FOR MIXING AND BLENDING IN CHEMICAL AND BIOTECHNOLOGY INDUSTRIES TO FUEL MARKET GROWTH 122

13 INDUSTRIAL AGITATORS MARKET, BY END-USE INDUSTRY 124

13.1 INTRODUCTION 125

13.2 CHEMICAL 127

13.2.1 OIL & PETROLEUM 127

13.2.1.1 Agitators utilized in mud mixing, extracting, and refining crude oil in oil & petroleum industry 127

13.2.1.2 Emulsification 128

13.2.1.3 Crude oil processing 128

13.2.1.4 Liquid & gas blending 128

13.2.1.5 Gas dispersion & absorption 129

13.2.2 WATER & WASTEWATER TREATMENT 129

13.2.2.1 Increasing need for wastewater treatment and improvements in water purification processes to drive demand 129

13.2.2.2 Gas dispersion & absorption 129

13.2.2.3 Washing & leaching 130

13.3 MINING 134

13.3.1 AGITATORS INCREASINGLY USED FOR HYDROMETALLURGICAL PROCESSES AND ATMOSPHERIC LEACH APPLICATIONS 134

13.3.2 LEACHING 135

13.3.3 SLURRY MIXING 135

13.3.4 ORE BENEFICIATION 135

13.3.5 FLOTATION PROCESSES 135

13.3.6 CYANIDATION 135

13.3.7 PRECIPITATION REACTIONS 135

13.3.8 CARBON-IN-PULP (CIP) & CARBON-IN-LEACH (CIL) 135

13.4 FOOD & BEVERAGE 140

13.4.1 RISING DEMAND FOR EFFICIENT FOOD & BEVERAGE PROCESSING TO DRIVE DEMAND 140

13.4.2 MIXING & BLENDING 140

13.4.3 FERMENTATION 141

13.4.4 HOMOGENIZATION 141

13.4.5 DISSOLVING SUGAR & SALTS 141

13.4.6 AERATION 141

13.4.7 FLAVORING AND ADDITIVE MIXING 141

13.5 PHARMACEUTICAL 147

13.5.1 AGITATORS WIDELY USED IN TABLET GRANULATIONS AND MIXING SYRUPS 147

13.5.2 ACTIVE PHARMACEUTICAL INGREDIENTS (APIS) 147

13.5.3 LIQUID DOSAGE FORM PREPARATION 147

13.5.4 VACCINE PRODUCTION 147

13.5.5 ANTIBIOTIC PRODUCTION 147

13.5.6 CONTROLLED RELEASE FORMULATION 148

13.5.7 STERILE MIXING 148

13.6 COSMETICS 153

13.6.1 AGITATORS USED IN COSMETICS INDUSTRY FOR EMULSIFICATION, POWDER WET-OUT, AND PARTICLE SIZE REDUCTION 153

13.6.2 GEL MIXING 153

13.6.3 COLORANT DISPERSION 154

13.6.4 AEROSOL PROPELLANT MIXING 154

13.6.5 VISCOSITY CONTROL 154

13.6.6 SUSPENSION OF SOLID INGREDIENTS 154

13.6.7 COSMETIC INGREDIENT ACTIVATION 154

13.6.8 TOPICAL FORMULATION MIXING 154

13.6.9 FILLING AND PACKAGING ASSISTANCE 154

13.7 PAINT & COATING 159

13.7.1 HELPS MINIMIZE COMPLEXITIES IN PAINT FORMULATIONS AND ENSURE QUALITY COATING 159

13.7.2 PIGMENT DISPERSION 159

13.7.3 EMULSION FORMATION 159

13.7.4 VISCOSITY CONTROL 160

13.7.5 POLYMERIZATION 160

13.7.6 SOLVENT MIXING 160

13.7.7 FILLER INCORPORATION 160

13.7.8 POWDER COATING MIXING 160

13.7.9 SPRAY COATING PREPARATION 160

13.7.10 PAINT RECYCLING 160

13.7.11 CHEMICAL REACTION MANAGEMENT 161

13.7.12 BATCH MIXING 161

13.7.13 ADDITIVE MIXING 161

13.8 OTHER END-USE INDUSTRIES 166

14 INDUSTRIAL AGITATORS MARKET, BY REGION 172

14.1 INTRODUCTION 173

14.2 NORTH AMERICA 175

14.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA 177

14.2.2 US 177

14.2.2.1 Growth in chemical and food & beverage industries to drive growth 177

14.2.3 CANADA 177

14.2.3.1 Government's focus on chemical industry to fuel demand for agitators 177

14.2.4 MEXICO 178

14.2.4.1 Structural reforms to boost growth of various sectors 178

14.3 EUROPE 178

14.3.1 MACROECONOMIC OUTLOOK FOR EUROPE 181

14.3.2 UK 181

14.3.2.1 Surging R&D activities in pharmaceutical and chemical industries to fuel demand 181

14.3.3 GERMANY 181

14.3.3.1 Demand from chemical, pharmaceutical, and paint & coating industries to drive market 181

14.3.4 FRANCE 182

14.3.4.1 Surging chemical industry to support market growth 182

14.3.5 REST OF EUROPE 182

14.4 ASIA PACIFIC 183

14.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC 185

14.4.2 CHINA 185

14.4.2.1 Domestic chemical manufacturing to provide opportunities for market players 185

14.4.3 JAPAN 186

14.4.3.1 Paradigm shift toward specialty chemicals to push demand for industrial agitators 186

14.4.4 INDIA 186

14.4.4.1 Government's plans to achieve self-sufficiency and expansion in various sectors to increase demand 186

14.4.5 REST OF ASIA PACIFIC 186

14.5 REST OF THE WORLD 187

14.5.1 MACROECONOMIC OUTLOOK FOR ROW 188

14.5.2 SOUTH AMERICA 188

14.5.2.1 Food & beverage industry to propel demand for industrial agitators 188

14.5.3 MIDDLE EAST 189

14.5.3.1 Surging demand for oil to support market growth 189

14.5.4 AFRICA 189

14.5.4.1 Mining industry to be significant end user of industrial agitators 189

15 COMPETITIVE LANDSCAPE 190

15.1 OVERVIEW 190

15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021–2024 190

15.3 REVENUE ANALYSIS, 2019–2023 191

15.4 MARKET SHARE ANALYSIS, 2023 192

15.5 COMPANY VALUATION AND FINANCIAL METRICS 194

15.6 BRAND/PRODUCT COMPARISON 195

15.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023 195

15.7.1 STARS 195

15.7.2 EMERGING LEADERS 196

15.7.3 PERVASIVE PLAYERS 196

15.7.4 PARTICIPANTS 196

15.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023 197

15.7.5.1 Company footprint 197

15.7.5.2 Region footprint 198

15.7.5.3 Model type footprint 199

15.7.5.4 Mounting footprint 200

15.7.5.5 End-use industry footprint 201

15.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023 202

15.8.1 PROGRESSIVE COMPANIES 202

15.8.2 RESPONSIVE COMPANIES 202

15.8.3 DYNAMIC COMPANIES 202

15.8.4 STARTING BLOCKS 202

15.8.5 COMPETITIVE BENCHMARKING, STARTUPS/SMES, 2023 204

15.8.5.1 Detailed list of key startups/SMEs 204

15.8.5.2 Competitive benchmarking of key startups/SMEs 204

15.9 COMPETITIVE SCENARIO 205

15.9.1 PRODUCT LAUNCHES 205

15.9.2 DEALS 206

15.9.3 EXPANSIONS 207

15.9.4 OTHERS 208

16 COMPANY PROFILES 209

16.1 KEY PLAYERS 209

16.1.1 SPX FLOW 209

16.1.1.1 Business overview 209

16.1.1.2 Products/Services/Solutions offered 210

16.1.1.3 Recent developments 211

16.1.1.3.1 Product launches 211

16.1.1.3.2 Deals 212

16.1.1.3.3 Expansions 213

16.1.1.3.4 Others 213

16.1.1.4 MnM view 214

16.1.1.4.1 Key strengths 214

16.1.1.4.2 Strategic choices 214

16.1.1.4.3 Weaknesses and competitive threats 214

16.1.2 XYLEM 215

16.1.2.1 Business overview 215

16.1.2.2 Products/Services/Solutions offered 216

16.1.2.3 Recent developments 217

16.1.2.3.1 Deal 217

16.1.2.4 MnM view 217

16.1.2.4.1 Key strengths 217

16.1.2.4.2 Strategic choices 217

16.1.2.4.3 Weaknesses and competitive threats 217

16.1.3 EKATO GROUP 218

16.1.3.1 Business overview 218

16.1.3.2 Products/Services/Solutions offered 218

16.1.3.3 Recent developments 219

16.1.3.4 MnM view 220

16.1.3.4.1 Key strengths 220

16.1.3.4.2 Strategic choices 220

16.1.3.4.3 Weaknesses and competitive threats 220

16.1.4 NOV 221

16.1.4.1 Business overview 221

16.1.4.2 Products/Services/Solutions offered 222

16.1.4.3 Recent developments 223

16.1.4.3.1 Product launches 223

16.1.4.3.2 Deals 224

16.1.4.4 MnM view 224

16.1.4.4.1 Key strengths 224

16.1.4.4.2 Strategic choices 224

16.1.4.4.3 Weaknesses and competitive threats 224

16.1.5 SULZER 225

16.1.5.1 Business overview 225

16.1.5.2 Products/Services/Solutions offered 227

16.1.5.3 Recent developments 227

16.1.5.3.1 Product launches 227

16.1.5.4 MnM view 228

16.1.5.4.1 Key strengths 228

16.1.5.4.2 Strategic choices 228

16.1.5.4.3 Weaknesses and competitive threats 228

16.1.6 INGERSOLL RAND 229

16.1.6.1 Business overview 229

16.1.6.2 Products/Services/Solutions offered 230

16.1.6.3 Recent developments 231

16.1.6.3.1 Product launches 231

16.1.6.3.2 Deals 231

16.1.7 DYNAMIX AGITATORS INC. 232

16.1.7.1 Business overview 232

16.1.7.2 Products/Services/Solutions offered 232

16.1.8 MIXER DIRECT 233

16.1.8.1 Business overview 233

16.1.8.2 Products/Services/Solutions offered 233

16.1.9 SILVERSON 234

16.1.9.1 Business overview 234

16.1.9.2 Products/Services/Solutions offered 234

16.1.10 STATIFLO GROUP 235

16.1.10.1 Business overview 235

16.1.10.2 Products/Services/Solutions offered 235

16.1.10.3 Recent developments 236

16.1.10.3.1 Deal 236

16.1.10.3.2 Expansions 236

16.1.11 TACMINA CORPORATION 237

16.1.11.1 Business overview 237

16.1.11.2 Products/Services/Solutions offered 237

16.2 OTHER PLAYERS 238

16.2.1 ALFA LAVAL 238

16.2.2 DE DIETRICH PROCESS SYSTEMS 239

16.2.3 EUROMIXERS 240

16.2.4 FAWCETT 241

16.2.5 MIXEL AGITATORS 242

16.2.6 PRG AGITATORS 243

16.2.7 PROQUIP 244

16.2.8 SAVINO BARBERA 245

16.2.9 SHARPE MIXERS 246

16.2.10 SHUANGLONG GROUP 247

16.2.11 SUMA RÜHRTECHNIK 247

16.2.12 TERALBA INDUSTRIES 248

16.2.13 TIMSA 249

16.2.14 WOODMAN AGITATORS 249

16.2.15 ZHEJIANG GREATWALL MIXERS 250

17 APPENDIX 251

17.1 INSIGHTS FROM INDUSTRY EXPERTS 251

17.2 DISCUSSION GUIDE 252

17.3 KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL 256

17.4 CUSTOMIZATION OPTIONS 258

17.5 RELATED REPORTS 258

17.6 AUTHOR DETAILS 259

❖ 世界の産業用攪拌機市場に関するよくある質問(FAQ) ❖

・産業用攪拌機の世界市場規模は?

→MarketsandMarkets社は2024年の産業用攪拌機の世界市場規模を31.0億米ドルと推定しています。

・産業用攪拌機の世界市場予測は?

→MarketsandMarkets社は2029年の産業用攪拌機の世界市場規模を39.9億米ドルと予測しています。

・産業用攪拌機市場の成長率は?

→MarketsandMarkets社は産業用攪拌機の世界市場が2024年~2029年に年平均5.2%成長すると予測しています。

・世界の産業用攪拌機市場における主要企業は?

→MarketsandMarkets社は「SPX Flow, Inc. (US), Xylem Inc. (US), Ekato Group (Germany), Sulzer Ltd. (Switzerland) and NOV Inc (US)など ...」をグローバル産業用攪拌機市場の主要企業として認識しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、納品レポートの情報と少し異なる場合があります。