1 はじめに 29

1.1 調査目的 29

1.2 市場の定義 29

1.3 調査範囲 30

1.3.1 セラミック製衛生陶器市場のセグメンテーションと地理的広がり 30

1.3.2 陶磁器製衛生陶器市場:包含と除外 31

1.3.3 セラミック製衛生陶器市場:タイプ別市場の定義と包含範囲 31

1.3.4 セラミック製衛生陶器市場:技術別市場の定義と包含範囲 31

1.3.5 セラミック製衛生陶器市場:用途別市場の定義と包含範囲 32

1.3.6 セラミック製衛生陶器市場:流通経路別市場の定義と包含範囲 32

1.4 考慮した年数 32

1.5 考慮した通貨 33

1.6 単位の検討 33

1.7 利害関係者 33

1.8 変化のまとめ 33

2 調査方法 35

2.1 調査データ 35

2.1.1 二次データ 36

2.1.1.1 主要な二次情報源のリスト 36

2.1.1.2 二次資料からの主要データ 36

2.1.2 一次データ 37

2.1.2.1 主要な一次参加者 37

2.1.2.2 主要な業界インサイト 38

2.1.2.3 専門家へのインタビューの内訳 38

2.2 市場規模の推定 39

2.2.1 ボトムアップアプローチ 39

2.2.2 トップダウンアプローチ 41

2.3 データの三角測量 42

2.4 成長予測 43

2.4.1 供給サイド分析 44

2.4.2 需要サイド分析 44

2.5 前提条件 45

2.6 研究の限界 46

2.7 リスク評価 46

3 エグゼクティブ・サマリー 47

4 プレミアムインサイト 51

4.1 セラミック製衛生陶器市場におけるプレーヤーの機会 51

4.2 セラミック製衛生陶器市場:地域別 51

4.3 アジア太平洋地域のセラミック製衛生陶器市場:用途別、国別 52

4.4 セラミック製衛生陶器市場:技術別、地域別 52

4.5 セラミック製衛生陶器市場の魅力 53

5 市場の概要 54

5.1 はじめに 54

5.2 市場ダイナミクス 54

5.2.1 推進要因 54

5.2.1.1 住宅・商業空間の需要拡大 54

5.2.1.2 可処分所得の増加による購買力の向上 55

5.2.1.3 衛生意識に関する政府の取り組み 55

5.2.2 阻害要因 56

5.2.2.1 激しい競争 56

5.2.2.2 インフレの高まりと地理的紛争 56

5.2.3 機会 56

5.2.3.1 製品のカスタマイズとデザイン革新 56

5.2.3.2 スマートテクノロジーの統合 57

5.2.3.3 高級感、エネルギー効率、快適性を重視した環境の創造 57

5.2.4 課題 58

5.2.4.1 消費者の嗜好の変化 58

5.2.4.2 競合他社の技術進歩 58

5.2.4.3 CO2排出量と持続可能性への課題 58

5.3 ポーターの5つの力分析 58

5.3.1 新規参入の脅威 59

5.3.2 代替品の脅威 59

5.3.3 供給者の交渉力 59

5.3.4 買い手の交渉力 60

5.3.5 競合の激しさ 60

5.4 主要ステークホルダーと購買基準 61

5.4.1 購入プロセスにおける主要ステークホルダー 61

5.4.2 購買基準

5.5 マクロ経済指標 62

5.5.1 GDPの動向と予測 63

6 業界動向 64

6.1 サプライチェーン分析 64

6.1.1 原材料 64

6.1.2 製造 64

6.1.3 流通ネットワーク 65

6.1.4 アプリケーション 65

6.2 価格分析 65

6.2.1 主要企業の平均販売価格(タイプ別) 65

6.2.2 平均販売価格(地域別) 66

6.3 顧客ビジネスに影響を与えるトレンド/混乱 66

6.4 エコシステム分析 67

6.5 ケーススタディ分析 69

6.5.1 セラミック製衛生陶器におけるサプライチェーンの課題 69

6.5.2 美的魅力のためのセラミック洗面ボウルのデザイン向上 69

6.5.3 衛生陶器における持続可能性と節水 69

6.6 技術分析 70

6.6.1 主要技術 70

6.6.1.1 高圧鋳造 70

6.6.2 補足技術 70

6.6.2.1 ロボットグレージングシステム 70

6.7 貿易分析 71

6.7.1 輸入シナリオ(HSコード6910) 71

6.7.2 輸出シナリオ(HSコード6910) 72

6.8 規制情勢 72

6.8.1 規制機関、政府機関、その他の組織 74

6.8.2 規制の枠組み 75

6.8.2.1 製品の安全性と品質基準 75

6.8.2.2 環境コンプライアンス 75

6.8.2.3 リサイクルと廃棄物管理 75

6.8.2.4 節水基準 76

6.8.2.5 エネルギー効率基準 77

6.9 主要会議・イベント(2024~2025年) 77

6.10 投資と資金調達のシナリオ 78

6.11 特許分析 78

6.11.1 方法論 78

6.11.2 文書タイプ 78

6.11.3 上位出願者 80

6.11.4 管轄区域分析 83

6.12 セラミック製衛生陶器市場におけるAI/GEN AIの影響 84

7 セラミック製衛生陶器市場、技術別 85

7.1 導入 86

7.2 スリップキャスティング 87

7.2.1 低コストと容易な操作が市場を牽引 87

7.3 圧力鋳造 89

7.3.1 高級品への需要の高まりが市場を牽引 89

7.4 テープ鋳造 90

7.4.1 高度な自動化と効率が市場を牽引 90

7.5 等方性鋳造 92

7.5.1 環境に優しい技術への需要が市場を牽引 92

8 セラミック製衛生陶器市場:タイプ別 94

8.1 導入 95

8.2 トイレ用流し台/水栓 98

8.2.1 ワンピース 99

8.2.1.1 水漏れの少ないシステムへの高い需要が市場を牽引 99

8.2.2 ツーピース 99

8.2.2.1 低コストが需要を牽引 99

8.2.3 壁掛けクローゼット 99

8.2.3.1 省スペースへのニーズが需要を牽引 99

8.2.4 欧州製ウォータークローゼット(EWC) 100

8.2.4.1 水消費量の少なさが需要を牽引 100

8.2.5 その他のセラミック製洗面台/ウォータークローゼット 100

8.3 洗面ボウル 100

8.3.1 ペデスタル 101

8.3.1.1 高級バスルーム製品への需要が市場を牽引 101

8.3.2 壁掛け型 101

8.3.2.1 小型軽量デザインが需要を牽引 101

8.3.3 コーナー 102

8.3.3.1 コンパクトなデザインが需要を促進 102

8.3.4 テーブルトップ 102

8.3.4.1 ハイエンド製品の需要が市場を牽引 102

8.3.5 カウンター 102

8.3.5.1 高級品への需要の高まりが市場を後押し 102

8.4 小便器 102

8.4.1 公共施設や商業施設への設置需要が市場を促進 102

8.5 貯水槽 104

8.5.1 工業化の進展が市場を牽引 104

8.6 その他のタイプ 105

9 セラミック製衛生陶器市場(用途別) 107

9.1 導入 108

9.2 商業用 110

9.2.1 ホスピタリティ 112

9.2.1.1 観光産業の成長が市場を牽引 112

9.2.2 オフィス 112

9.2.2.1 都市化の進展が需要を促進 112

9.2.3 施設・小売 112

9.2.3.1 新興国からの需要増加が市場を牽引 112

9.2.4 工業 112

9.2.4.1 工業化の進展が市場を牽引 112

9.3 住宅用 112

9.3.1 一戸建て 114

9.3.1.1 先進国の需要が成長を支える 114

9.3.2 マルチファミリー 114

9.3.2.1 世界的な賃貸住宅居住者の増加と職業移植性が市場を牽引 114

10 セラミック製衛生陶器市場:流通チャネル別 115

10.1 導入 116

10.2 直接販売 116

10.2.1 競争激化が需要を牽引 116

10.3 間接的 116

10.3.1 技術的進歩と消費者の利便性が需要を促進 116

11 セラミック製衛生陶器市場:地域別 118

11.1 はじめに 119

11.2 アジア太平洋地域 121

11.2.1 中国 128

11.2.1.1 大規模な都市化と建築ネットワークが市場を牽引 128

11.2.2 日本 130

11.2.2.1 主要企業の存在感が市場を牽引 130

11.2.3 インド 132

11.2.3.1 大規模な都市化と建設セクターの急成長が市場を牽引 132

11.2.4 インドネシア 134

11.2.4.1 国内消費の拡大と直接投資が市場を押し上げる 134

11.2.5 タイ 136

11.2.5.1 建設セクターへの投資増加が市場成長を後押し 136

11.2.6 韓国 139

11.2.6.1 衛生面の重要性の高まりが市場を後押し 139

11.2.7 オーストラリア 140

11.2.7.1 エンジニアリング建設と住宅・非住宅建築活動が市場を押し上げる 140

11.2.8 マレーシア 142

11.2.8.1 人口の増加と所得の増加が市場を押し上げる 142

11.3 欧州 144

11.3.1 ドイツ 151

11.3.1.1 化学、自動車、塗料・コーティング産業が市場を促進 151

11.3.2 ロシア 153

11.3.2.1 膨大な人口が市場を牽引 153

11.3.3 フランス 155

11.3.3.1 ホスピタリティ産業が市場を牽引 155

11.3.4 イギリス 157

11.3.4.1 成長する建設セクターが市場を牽引 157

11.3.5 イタリア 159

11.3.5.1 新たなプロジェクトファイナンス規則と投資政策が市場を後押し 159

11.3.6 スペイン 161

11.3.6.1 産業部門の成長が市場を牽引 161

11.3.7 トルコ 163

11.3.7.1 建設産業の急速な拡大が市場を牽引 163

11.4 北米 165

11.4.1 米国 172

11.4.1.1 主要企業の強固な足場が市場を牽引 172

11.4.2 カナダ 174

11.4.2.1 海外貿易と建設プロジェクトの増加が需要を促進 174

11.4.3 メキシコ 176

11.4.3.1 観光産業の成長が市場を牽引 176

11.5 中東・アフリカ 178

11.5.1 GCC諸国 184

11.5.1.1 サウジアラビア 185

11.5.1.1.1 インフラ整備への多額の政府投資が需要を押し上げる 185

11.5.1.2 ウアイ 187

11.5.1.2.1 不動産とインフラプロジェクトの成長が市場を牽引 187

11.5.2 エジプト 189

11.5.2.1 インフラ整備を促進する経済成長が市場を牽引 189

11.6 南米 191

11.6.1 ブラジル 197

11.6.1.1 インフラプロジェクト実施の増加が市場を牽引 197

11.6.2 アルゼンチン 199

11.6.2.1 人口増加と経済状況の改善が市場を牽引 199

11.6.3 コロンビア 201

11.6.3.1 人口の増加が市場を牽引 201

12 競争環境 204

12.1 はじめに 204

12.2 主要企業の戦略/勝利への権利(2020年1月~2024年10月) 204

12.3 市場シェア分析(2023年) 205

12.4 上位5社の収益分析(2019-2023年) 208

12.5 企業評価マトリックス:主要プレイヤー(2023年) 208

12.5.1 スター企業 208

12.5.2 新興リーダー 208

12.5.3 浸透型プレーヤー 209

12.5.4 参加企業 209

12.5.5 企業フットプリント:主要プレーヤー、2023年 210

12.5.5.1 企業フットプリント 210

12.5.5.2 地域別フットプリント 211

12.5.5.3 アプリケーション別フットプリント 212

12.5.5.4 タイプ別フットプリント 213

12.5.5.5 技術のフットプリント 214

12.6 企業評価マトリクス:新興企業/SM(2023年) 215

12.6.1 進歩的企業 215

12.6.2 対応力のある企業 215

12.6.3 ダイナミックな企業 215

12.6.4 スターティングブロック 215

12.6.5 競争ベンチマーキング:新興企業/SM(2023年) 216

12.6.5.1 主要新興企業/SMESの詳細リスト 216

12.6.5.2 主要新興企業/SMEの競合ベンチマーキング 217

12.7 ブランド/製品比較分析 217

12.8 企業評価と財務指標 218

12.9 競争シナリオ 219

12.9.1 製品上市 219

12.9.2 取引 221

12.9.3 事業拡大 222

13 会社プロファイル 223

13.1 主要企業 223

Geberit AG (Switzerland)

LIXIL Corporation (Japan)

Villeroy & Boch AG (Germany)

RAK Ceramics (UAE)

TOTO Ltd. (Japan)

Roca Sanitario S.A.U. (Spain)

Huida Sanitary Ware Co.Ltd. (China)

Hindware Home Innovation Limited (India)

Duravit AG (Germany)

Kohler Co. (US)

Saudi Ceramics (Saudi Arabia)

CERA Sanitaryware Limited (India)

14 隣接市場および関連市場 259

14.1 はじめに 259

14.2 セラミックタイル市場 259

14.2.1 市場の定義 259

14.2.2 市場の概要 259

14.3 セラミックタイル市場(地域別) 260

14.3.1 アジア太平洋地域 261

14.3.2 北米 262

14.3.3 欧州 263

14.3.4 南米 264

14.3.5 中東・アフリカ 265

15 付録 267

15.1 ディスカッション・ガイド 267

15.2 Knowledgestore: Marketsandmarketsの購読ポータル 269

15.3 カスタマイズオプション 271

15.4 関連レポート 271

15.5 著者の詳細 272

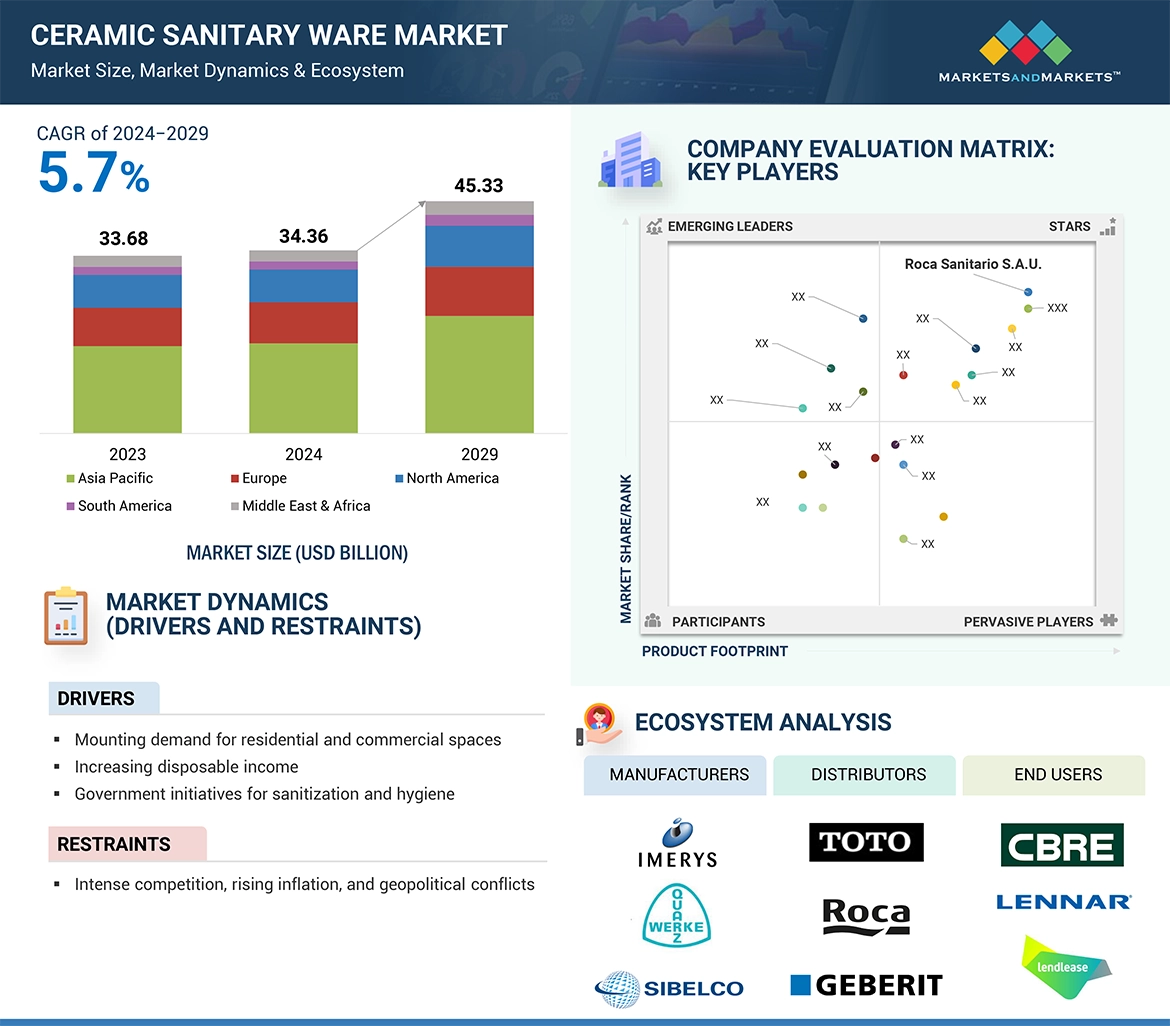

Demand regarding sanitation and hygiene awareness through Government campaigns has a lot to offer to the ceramic sanitary ware market. Most of the programs that aim at promoting health and cleanliness throughout the population are leading to the use of current and clean bathroom products within buildings. More initiatives from the government in the form of improvising clean water supply for its citizens; better sanitation facilities; and the provision of hygiene awareness are boosting the demand for high-quality, long-lasting ceramics specifically used in sanitary purposes and with water economy features. As governments focus their budgets at improving sanitation facilities there is ever increasing demand for better and high quality ceramics particularly in the developing countries. Moreover, the rising population in the Middle East & Africa and Asia Pacific, changing customer needs, increasing industrial expansion in Asia Pacific region are driving the ceramic sanitary ware market. In addition, due to changing sustanibility goals, environmental norms, and changing regulations, there is an escalating desire for water saving technologies in ceramic sanitary ware.

“Toilet sinks/water closets type was the largest type of ceramic sanitary ware market, in terms of value, in 2023.”

Toilet sinks or water closets (WCs) hold the biggest market share in the ceramic sanitary ware market because sanitary utilities are usual in households and companies. Due to its utilization in every family, businesses, commercial and social establishments, the market for water closets is always resistant. Ceramic is preferred because it is hard wearing, easy to clean and can be shaped into various forms to suit customer requirement. Also about recent enhancements in water-saving and environmentally friendly technologies like dual flush, it has even helped in increasing the popularity of water closets. Since toilet sinks are needed almost everywhere owing to considerations of hygiene, they occupy a large market share in the ceramic sanitary ware industry as they are the primary components of modern sanitary systems.

“Residential was second-largest application of ceramic sanitary ware market, in terms of value, in 2023.”

The second largest application for the ceramic sanitary ware market is the residential segment due to the increasing trend of using high quality advanced ceramic sanitary ware in residences. With growth of disposable income and consumer focus turning to the home, the world definitely starts shifting towards more durable as well as aesthetically appealing ceramics products such as washbasins, toilets, bathtub, etc. Also continued demand from the bathroom remodeling trend and the need for a luxurious bathrooms and living spaces. Due to the growing awareness on hygiene, sustainability, and design, the residential end use consumer segment demands technologically superior, water-saving, and attractive sanitary ware products.

“The Middle East & AFrica is projected to be the third fastest-growing region, in terms of value, during the forecast period in the ceramic sanitary ware market.”

The Middle East & Africa followed by Asia Pacific region is identified to have the third highest CAGR in the ceramic sanitary ware market due to the increasing industrialization of the region and high investment on infrastructural. Large-scale investments in construction projects for mass housing applications and commerce and business establishments are pulling demand for superior ceramic sanitary wares. Also, population growth and urbanization around the region also complement the demand for high quality ceramic sanitary wares. There is also a rising trend towards sustainability with awareness of the same forcing technologies to embrace environment friendly sanitary wares. Similarly, the investment from the Middle East & African countries and emergence of new industrial projects also have a positive impact on the growth rate of ceramic sanitary ware industry in this area and therefore it is expected to register a good growth rate in the coming future.

• By Company Type: Tier 1 - 55%, Tier 2 - 25%, and Tier 20%

• By Designation: Directors - 50%, Managers - 30%, and Others - 20%

• By Region: North America - 40%, Europe - 35%, Asia Pacific - 20%, RoW - 5%,

The key players profiled in the report include Geberit AG (Switzerland), LIXIL Corporation (Japan), Villeroy & Boch AG (Germany), RAK Ceramics (UAE), TOTO Ltd. (Japan), Roca Sanitario S.A.U. (Spain), Huida Sanitary Ware Co., Ltd. (China), Hindware Home Innovation Limited (India), Duravit AG (Germany), Kohler Co. (US), Saudi Ceramics (Saudi Arabia), CERA Sanitaryware Limited (India), and among others.

Research Coverage

This report segments the market for ceramic sanitary ware based on type, technology, distribution channel, application, and region and provides estimations of volume (Units) and value (USD Million) for the overall market size across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, services, and key strategies, associated with the market for ceramic sanitary wares.

Reasons to Buy this Report

This research report is focused on various levels of analysis — industry analysis (industry trends), market share analysis of top players, and company profiles, which together provide an overall view of the competitive landscape, emerging and high-growth segments of the ceramic sanitary ware market; high-growth regions; and market drivers, restraints, and opportunities.

The report provides insights on the following pointers:

• Market Penetration: Comprehensive information on ceramic sanitary ware offered by top players in the global market

• Analysis of key drivers: (increasing demand for residential and commercial spaces, increasing disposal income, and government initiatives regarding sanitization and hygiene), restraints (Increasing inflation and geographical conflicts), opportunities (design and customization innovation, use of smart technologies, and expanding ceramic sanitary ware with heating solutions), and challenges (changing consumer preference, technological advancements by competitors, and CO2 emission and sustainability issues) influencing the growth of ceramic sanitary ware market.

• Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the ceramic sanitary ware market

• Market Development: Comprehensive information about lucrative emerging markets — the report analyzes the markets for ceramic sanitary ware across regions.

• Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global ceramic sanitary ware market

• Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the ceramic sanitary ware market

1 INTRODUCTION 29

1.1 STUDY OBJECTIVES 29

1.2 MARKET DEFINITION 29

1.3 STUDY SCOPE 30

1.3.1 CERAMIC SANITARY WARE MARKET SEGMENTATION AND GEOGRAPHICAL SPREAD 30

1.3.2 CERAMIC SANITARY WARE MARKET: INCLUSIONS AND EXCLUSIONS 31

1.3.3 CERAMIC SANITARY WARE MARKET: MARKET DEFINITION AND INCLUSIONS, BY TYPE 31

1.3.4 CERAMIC SANITARY WARE MARKET: MARKET DEFINITION AND INCLUSIONS, BY TECHNOLOGY 31

1.3.5 CERAMIC SANITARY WARE MARKET: MARKET DEFINITION AND INCLUSIONS, BY APPLICATION 32

1.3.6 CERAMIC SANITARY WARE MARKET: MARKET DEFINITION AND INCLUSIONS, BY DISTRIBUTION CHANNEL 32

1.4 YEARS CONSIDERED 32

1.5 CURRENCY CONSIDERED 33

1.6 UNITS CONSIDERED 33

1.7 STAKEHOLDERS 33

1.8 SUMMARY OF CHANGES 33

2 RESEARCH METHODOLOGY 35

2.1 RESEARCH DATA 35

2.1.1 SECONDARY DATA 36

2.1.1.1 List of key secondary sources 36

2.1.1.2 Key data from secondary sources 36

2.1.2 PRIMARY DATA 37

2.1.2.1 Key primary participants 37

2.1.2.2 Key industry insights 38

2.1.2.3 Breakdown of interviews with experts 38

2.2 MARKET SIZE ESTIMATION 39

2.2.1 BOTTOM-UP APPROACH 39

2.2.2 TOP-DOWN APPROACH 41

2.3 DATA TRIANGULATION 42

2.4 GROWTH FORECAST 43

2.4.1 SUPPLY-SIDE ANALYSIS 44

2.4.2 DEMAND-SIDE ANALYSIS 44

2.5 ASSUMPTIONS 45

2.6 RESEARCH LIMITATIONS 46

2.7 RISK ASSESSMENT 46

3 EXECUTIVE SUMMARY 47

4 PREMIUM INSIGHTS 51

4.1 OPPORTUNITIES FOR PLAYERS IN CERAMIC SANITARY WARE MARKET 51

4.2 CERAMIC SANITARY WARE MARKET, BY REGION 51

4.3 ASIA PACIFIC CERAMIC SANITARY WARE MARKET, BY APPLICATION AND COUNTRY 52

4.4 CERAMIC SANITARY WARE MARKET, BY TECHNOLOGY AND REGION 52

4.5 CERAMIC SANITARY WARE MARKET ATTRACTIVENESS 53

5 MARKET OVERVIEW 54

5.1 INTRODUCTION 54

5.2 MARKET DYNAMICS 54

5.2.1 DRIVERS 54

5.2.1.1 Growing demand for residential and commercial spaces 54

5.2.1.2 Rising disposable income increasing purchasing power 55

5.2.1.3 Government initiatives related to awareness of sanitation and hygiene 55

5.2.2 RESTRAINTS 56

5.2.2.1 Intense competition 56

5.2.2.2 Rising inflation and geographical conflicts 56

5.2.3 OPPORTUNITIES 56

5.2.3.1 Customization and design innovations in products 56

5.2.3.2 Integration of smart technologies 57

5.2.3.3 Creation of luxurious, energy-efficient, and comfort-oriented environments 57

5.2.4 CHALLENGES 58

5.2.4.1 Changing consumer preferences 58

5.2.4.2 Technological advancements by competitors 58

5.2.4.3 CO2 emissions and challenges in sustainability 58

5.3 PORTER’S FIVE FORCES ANALYSIS 58

5.3.1 THREAT OF NEW ENTRANTS 59

5.3.2 THREAT OF SUBSTITUTES 59

5.3.3 BARGAINING POWER OF SUPPLIERS 59

5.3.4 BARGAINING POWER OF BUYERS 60

5.3.5 INTENSITY OF COMPETITIVE RIVALRY 60

5.4 KEY STAKEHOLDERS AND BUYING CRITERIA 61

5.4.1 KEY STAKEHOLDERS IN BUYING PROCESS 61

5.4.2 BUYING CRITERIA 61

5.5 MACROECONOMIC INDICATORS 62

5.5.1 GDP TRENDS AND FORECAST 63

6 INDUSTRY TRENDS 64

6.1 SUPPLY CHAIN ANALYSIS 64

6.1.1 RAW MATERIALS 64

6.1.2 MANUFACTURING 64

6.1.3 DISTRIBUTION NETWORK 65

6.1.4 APPLICATIONS 65

6.2 PRICING ANALYSIS 65

6.2.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY TYPE 65

6.2.2 AVERAGE SELLING PRICE, BY REGION 66

6.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS 66

6.4 ECOSYSTEM ANALYSIS 67

6.5 CASE STUDY ANALYSIS 69

6.5.1 SUPPLY CHAIN CHALLENGES IN CERAMIC SANITARY WARE 69

6.5.2 UPGRADING DESIGN OF CERAMIC WASHBASINS FOR ESTHETIC APPEAL 69

6.5.3 SUSTAINABILITY AND WATER CONSERVATION IN SANITARY WARE 69

6.6 TECHNOLOGY ANALYSIS 70

6.6.1 KEY TECHNOLOGIES 70

6.6.1.1 High pressure casting 70

6.6.2 COMPLEMENTARY TECHNOLOGIES 70

6.6.2.1 Robotic glazing system 70

6.7 TRADE ANALYSIS 71

6.7.1 IMPORT SCENARIO (HS CODE 6910) 71

6.7.2 EXPORT SCENARIO (HS CODE 6910) 72

6.8 REGULATORY LANDSCAPE 72

6.8.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS 74

6.8.2 REGULATORY FRAMEWORK 75

6.8.2.1 Product safety and quality standards 75

6.8.2.2 Environmental compliance 75

6.8.2.3 Recycling and waste management 75

6.8.2.4 Water conservation standards 76

6.8.2.5 Energy efficiency standards 77

6.9 KEY CONFERENCES AND EVENTS, 2024–2025 77

6.10 INVESTMENT AND FUNDING SCENARIO 78

6.11 PATENT ANALYSIS 78

6.11.1 METHODOLOGY 78

6.11.2 DOCUMENT TYPES 78

6.11.3 TOP APPLICANTS 80

6.11.4 JURISDICTION ANALYSIS 83

6.12 IMPACT OF AI/GEN AI ON CERAMIC SANITARY WARE MARKET 84

7 CERAMIC SANITARY WARE MARKET, BY TECHNOLOGY 85

7.1 INTRODUCTION 86

7.2 SLIP CASTING 87

7.2.1 LOW COST AND EASY OPERATION TO DRIVE MARKET 87

7.3 PRESSURE CASTING 89

7.3.1 RISING DEMAND FOR LUXURY PRODUCTS TO DRIVE MARKET 89

7.4 TAPE CASTING 90

7.4.1 HIGH DEGREE OF AUTOMATION AND EFFICIENCY TO DRIVE MARKET 90

7.5 ISOSTATIC CASTING 92

7.5.1 DEMAND FOR ECO-FRIENDLY TECHNOLOGY TO DRIVE MARKET 92

8 CERAMIC SANITARY WARE MARKET, BY TYPE 94

8.1 INTRODUCTION 95

8.2 TOILET SINKS/WATER CLOSETS 98

8.2.1 ONE PIECE 99

8.2.1.1 High demand for low water leakage systems to drive market 99

8.2.2 TWO PIECE 99

8.2.2.1 Low cost to drive demand 99

8.2.3 WALL HUNG CLOSETS 99

8.2.3.1 Need for less space to drive demand 99

8.2.4 EUROPEAN WATER CLOSETS (EWC) 100

8.2.4.1 Low water consumption to drive demand 100

8.2.5 OTHER CERAMIC-BASED TOILET SINKS/WATER CLOSETS 100

8.3 WASHBASINS 100

8.3.1 PEDESTAL 101

8.3.1.1 Demand for luxurious bathroom products to drive market 101

8.3.2 WALL HUNG 101

8.3.2.1 Small and lightweight design to drive demand 101

8.3.3 CORNER 102

8.3.3.1 Compact design to propel demand 102

8.3.4 TABLE TOP 102

8.3.4.1 Demand for high-end products to drive market 102

8.3.5 COUNTER 102

8.3.5.1 Rising demand for luxury to fuel market 102

8.4 URINALS 102

8.4.1 DEMAND FOR INSTALLATION IN PUBLIC AND COMMERCIAL PLACES TO PROPEL MARKET 102

8.5 CISTERNS 104

8.5.1 RISING INDUSTRIALIZATION TO DRIVE MARKET 104

8.6 OTHER TYPES 105

9 CERAMIC SANITARY WARE MARKET, BY APPLICATION 107

9.1 INTRODUCTION 108

9.2 COMMERCIAL 110

9.2.1 HOSPITALITY 112

9.2.1.1 Growth of tourism industry to drive market 112

9.2.2 OFFICE 112

9.2.2.1 Rising urbanization to fuel demand 112

9.2.3 INSTITUTIONAL & RETAIL 112

9.2.3.1 Increasing demand from emerging nations to drive market 112

9.2.4 INDUSTRIAL 112

9.2.4.1 Rising industrialization to propel market 112

9.3 RESIDENTIAL 112

9.3.1 SINGLE FAMILY 114

9.3.1.1 Demand from developed nations to support growth 114

9.3.2 MULTI FAMILY 114

9.3.2.1 Growing numbers of renters and job portability globally to drive market 114

10 CERAMIC SANITARY WARE MARKET, BY DISTRIBUTION CHANNEL 115

10.1 INTRODUCTION 116

10.2 DIRECT 116

10.2.1 RISING COMPETITION TO DRIVE DEMAND 116

10.3 INDIRECT 116

10.3.1 TECHNOLOGICAL ADVANCEMENTS AND CONSUMER CONVENIENCE TO FUEL DEMAND 116

11 CERAMIC SANITARY WARE MARKET, BY REGION 118

11.1 INTRODUCTION 119

11.2 ASIA PACIFIC 121

11.2.1 CHINA 128

11.2.1.1 Massive growth in urbanization and architectural network to drive market 128

11.2.2 JAPAN 130

11.2.2.1 Strong presence of key players to drive market 130

11.2.3 INDIA 132

11.2.3.1 Large-scale urbanization and rapid growth of construction sector to drive market 132

11.2.4 INDONESIA 134

11.2.4.1 Growing domestic consumption and FDI to boost market 134

11.2.5 THAILAND 136

11.2.5.1 Rising investments in construction sector to support market growth 136

11.2.6 SOUTH KOREA 139

11.2.6.1 Increased importance of hygiene to boost market 139

11.2.7 AUSTRALIA 140

11.2.7.1 Engineering construction and residential and non-residential building activities to boost market 140

11.2.8 MALAYSIA 142

11.2.8.1 Growing population and rising income to boost market 142

11.3 EUROPE 144

11.3.1 GERMANY 151

11.3.1.1 Chemical, automotive, and paints & coatings industries to propel market 151

11.3.2 RUSSIA 153

11.3.2.1 Huge population to drive market 153

11.3.3 FRANCE 155

11.3.3.1 Hospitality sector to fuel market 155

11.3.4 UK 157

11.3.4.1 Growing construction sector to drive market 157

11.3.5 ITALY 159

11.3.5.1 New project finance rules and investment policies to boost market 159

11.3.6 SPAIN 161

11.3.6.1 Growing industrial sector to drive market 161

11.3.7 TURKEY 163

11.3.7.1 Rapid expansion of construction industry to propel market 163

11.4 NORTH AMERICA 165

11.4.1 US 172

11.4.1.1 Strong foothold of key players to propel market 172

11.4.2 CANADA 174

11.4.2.1 Foreign trade and increasing construction projects to fuel demand 174

11.4.3 MEXICO 176

11.4.3.1 Growth of tourism industry to propel market 176

11.5 MIDDLE EAST & AFRICA 178

11.5.1 GCC COUNTRIES 184

11.5.1.1 Saudi Arabia 185

11.5.1.1.1 Significant government investments in infrastructure development to boost demand 185

11.5.1.2 UAE 187

11.5.1.2.1 Growth in real estate and infrastructure projects to drive market 187

11.5.2 EGYPT 189

11.5.2.1 Economic growth facilitating infrastructural development to drive market 189

11.6 SOUTH AMERICA 191

11.6.1 BRAZIL 197

11.6.1.1 Growing implementation of infrastructure projects to drive market 197

11.6.2 ARGENTINA 199

11.6.2.1 Increase in population and improved economic conditions to drive market 199

11.6.3 COLOMBIA 201

11.6.3.1 Growing population to drive market 201

12 COMPETITIVE LANDSCAPE 204

12.1 INTRODUCTION 204

12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, JANUARY 2020–OCTOBER 2024 204

12.3 MARKET SHARE ANALYSIS, 2023 205

12.4 REVENUE ANALYSIS OF TOP FIVE PLAYERS, 2019–2023 208

12.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023 208

12.5.1 STARS 208

12.5.2 EMERGING LEADERS 208

12.5.3 PERVASIVE PLAYERS 209

12.5.4 PARTICIPANTS 209

12.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023 210

12.5.5.1 Company footprint 210

12.5.5.2 Region footprint 211

12.5.5.3 Application footprint 212

12.5.5.4 Type footprint 213

12.5.5.5 Technology footprint 214

12.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023 215

12.6.1 PROGRESSIVE COMPANIES 215

12.6.2 RESPONSIVE COMPANIES 215

12.6.3 DYNAMIC COMPANIES 215

12.6.4 STARTING BLOCKS 215

12.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2023 216

12.6.5.1 Detailed list of key startups/SMES 216

12.6.5.2 Competitive benchmarking of key startups/SMEs 217

12.7 BRAND/PRODUCT COMPARISON ANALYSIS 217

12.8 COMPANY VALUATION AND FINANCIAL METRICS 218

12.9 COMPETITIVE SCENARIO 219

12.9.1 PRODUCT LAUNCHES 219

12.9.2 DEALS 221

12.9.3 EXPANSIONS 222

13 COMPANY PROFILES 223

13.1 KEY PLAYERS 223

14 ADJACENT AND RELATED MARKETS 259

14.1 INTRODUCTION 259

14.2 CERAMIC TILES MARKET 259

14.2.1 MARKET DEFINITION 259

14.2.2 MARKET OVERVIEW 259

14.3 CERAMIC TILES MARKET, BY REGION 260

14.3.1 ASIA PACIFIC 261

14.3.2 NORTH AMERICA 262

14.3.3 EUROPE 263

14.3.4 SOUTH AMERICA 264

14.3.5 MIDDLE EAST & AFRICA 265

15 APPENDIX 267

15.1 DISCUSSION GUIDE 267

15.2 KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL 269

15.3 CUSTOMIZATION OPTIONS 271

15.4 RELATED REPORTS 271

15.5 AUTHOR DETAILS 272

❖ 世界のセラミック製衛生陶器市場に関するよくある質問(FAQ) ❖

・セラミック製衛生陶器の世界市場規模は?

→MarketsandMarkets社は2024年のセラミック製衛生陶器の世界市場規模を343.6億米ドルと推定しています。

・セラミック製衛生陶器の世界市場予測は?

→MarketsandMarkets社は2029年のセラミック製衛生陶器の世界市場規模を453.3億米ドルと予測しています。

・セラミック製衛生陶器市場の成長率は?

→MarketsandMarkets社はセラミック製衛生陶器の世界市場が2024年~2029年に年平均5.7%成長すると予測しています。

・世界のセラミック製衛生陶器市場における主要企業は?

→MarketsandMarkets社は「Geberit AG (Switzerland), LIXIL Corporation (Japan), Villeroy & Boch AG (Germany), RAK Ceramics (UAE), TOTO Ltd. (Japan), Roca Sanitario S.A.U. (Spain), Huida Sanitary Ware Co., Ltd. (China), Hindware Home Innovation Limited (India), Duravit AG (Germany), Kohler Co. (US), Saudi Ceramics (Saudi Arabia), CERA Sanitaryware Limited (India)など ...」をグローバルセラミック製衛生陶器市場の主要企業として認識しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、納品レポートの情報と少し異なる場合があります。