1. 方法論と範囲

1.1. 調査方法

1.2. 調査目的と調査範囲

2. 定義と概要

3. エグゼクティブ・サマリー

3.1. 製品別スニペット

3.2. ソース別スニペット

3.3. 技術別スニペット

3.4. 地域別スニペット

4. ダイナミクス

4.1. 影響要因

4.1.1. 推進要因

4.1.1.1. 持続可能な繊維と倫理的な製造方法の台頭

4.1.1.2. 環境負荷の増大

4.1.2. 阻害要因

4.1.2.1. リサイクルの難しさ

4.1.3. 機会

4.1.4. 影響分析

5. 産業分析

5.1. ポーターのファイブフォース分析

5.2. サプライチェーン分析

5.3. 価格分析

5.4. 規制分析

5.5. ロシア・ウクライナ戦争の影響分析

5.6. DMI意見

6. COVID-19分析

6.1. COVID-19の分析

6.1.1. COVID-19以前のシナリオ

6.1.2. COVID-19開催中のシナリオ

6.1.3. COVID-19後のシナリオ

6.2. COVID-19中の価格ダイナミクス

6.3. 需給スペクトラム

6.4. パンデミック時の市場に関連する政府の取り組み

6.5. メーカーの戦略的取り組み

6.6. 結論

7. 製品別

7.1. 製品紹介

7.1.1. 市場規模分析および前年比成長率分析(%), 製品別

7.1.2. 市場魅力度指数(製品別

7.2. オーガニック*市場

7.2.1. 序論

7.2.2. 市場規模分析と前年比成長率分析(%)

7.3. 人工/再生

7.4. リサイクル

7.5. 天然

7.6. その他

8. 供給源別

8.1. 導入

8.1.1. ソース別市場規模分析および前年比成長率分析(%).

8.1.2. 市場魅力度指数(ソース別

8.2. 植物由来

8.2.1. 導入

8.2.2. 市場規模分析と前年比成長率分析(%)

8.3. 動物性

8.4. リサイクル

9. 技術別

9.1. 導入

9.1.1. 市場規模分析および前年比成長率分析(%), 技術別

9.1.2. 市場魅力度指数、技術別

9.2. 環境にやさしい染料

9.2.1. 導入

9.2.2. 市場規模分析と前年比成長率分析(%)

9.3. 水なし染色技術

9.4. 生分解性繊維

9.5. クローズドループ生産システム

10. 地域別

10.1. はじめに

10.1.1. 地域別市場規模分析および前年比成長率分析(%)

10.1.2. 市場魅力度指数、地域別

10.2. 北米

10.2.1. 序論

10.2.2. 主な地域別ダイナミクス

10.2.3. 市場規模分析および前年比成長率分析(%), 製品別

10.2.4. 市場規模分析およびYoY成長率分析(%)、ソース別

10.2.5. 市場規模分析および前年比成長率分析(%), 技術別

10.2.6. 市場規模分析および前年比成長率分析(%), 国別

10.2.6.1. 米国

10.2.6.2. カナダ

10.2.6.3. メキシコ

10.3. ヨーロッパ

10.3.1. はじめに

10.3.2. 主な地域別ダイナミクス

10.3.3. 市場規模分析および前年比成長率分析(%), 製品別

10.3.4. 市場規模分析およびYoY成長率分析(%), 供給源別

10.3.5. 市場規模分析および前年比成長率分析(%), 技術別

10.3.6. 市場規模分析および前年比成長率分析(%), 国別

10.3.6.1. ドイツ

10.3.6.2. イギリス

10.3.6.3. フランス

10.3.6.4. イタリア

10.3.6.5. スペイン

10.3.6.6. その他のヨーロッパ

10.4. 南米

10.4.1. はじめに

10.4.2. 地域別主要市場

10.4.3. 市場規模分析および前年比成長率分析(%), 製品別

10.4.4. 市場規模分析およびYoY成長率分析(%)、ソース別

10.4.5. 市場規模分析およびYoY成長率分析(%)、技術別

10.4.6. 市場規模分析および前年比成長率分析(%), 国別

10.4.6.1. ブラジル

10.4.6.2. アルゼンチン

10.4.6.3. その他の南米諸国

10.5. アジア太平洋

10.5.1. 序論

10.5.2. 主な地域別ダイナミクス

10.5.3. 市場規模分析および前年比成長率分析(%)、コンポーネント別

10.5.4. 市場規模分析とYoY成長率分析(%)、製品別

10.5.5. 市場規模分析および前年比成長率分析(%)、ソース別

10.5.6. 市場規模分析および前年比成長率分析(%), 技術別

10.5.7. 市場規模分析および前年比成長率分析(%), 国別

10.5.7.1. 中国

10.5.7.2. インド

10.5.7.3. 日本

10.5.7.4. オーストラリア

10.5.7.5. その他のアジア太平洋地域

10.6. 中東・アフリカ

10.6.1. 序論

10.6.2. 主な地域別ダイナミクス

10.6.3. 市場規模分析および前年比成長率分析(%), 製品別

10.6.4. 市場規模分析およびYoY成長率分析(%)、ソース別

10.6.5. 市場規模分析と前年比成長率分析(%), 技術別

11. 競争環境

11.1. 競争シナリオ

11.2. 市場ポジショニング/シェア分析

11.3. M&A分析

12. 企業プロフィール

12.1. Lenzing AG*

12.1.1. Company Overview

12.1.2. Product Portfolio and Description

12.1.3. Financial Overview

12.1.4. Key Developments

12.2. US Fibers

12.3. Grasim Industries Ltd.

12.4. Shanghai Tenbro Bamboo Textile Co. Ltd.

12.5. China Bambro Textile (Group) Co., Ltd.

12.6. Pilipinas Ecofiber Corporation

12.7. Teijin Limited

12.8. Foss Performance Materials

12.9. BASF

12.10. Södra

リストは網羅的ではありません

13. 付録

13.1. 会社概要とサービス

13.2. お問い合わせ

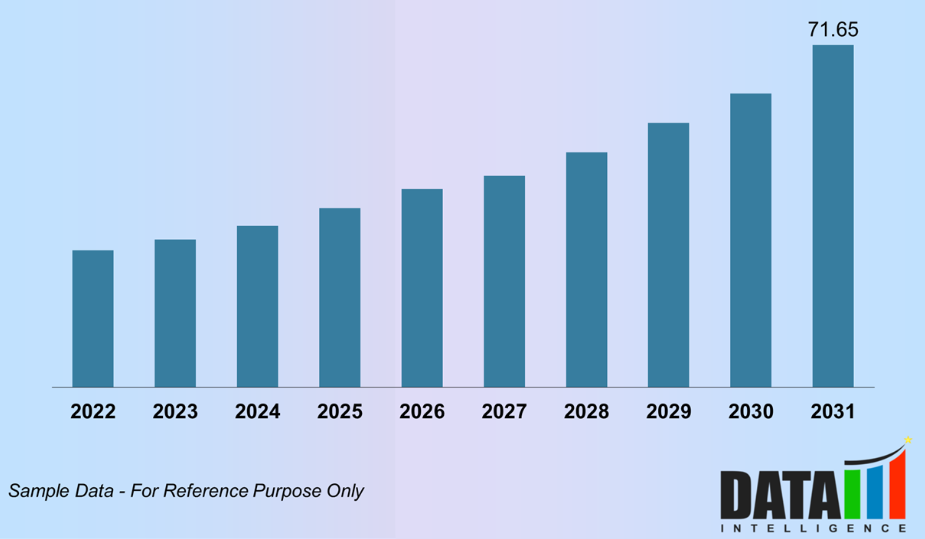

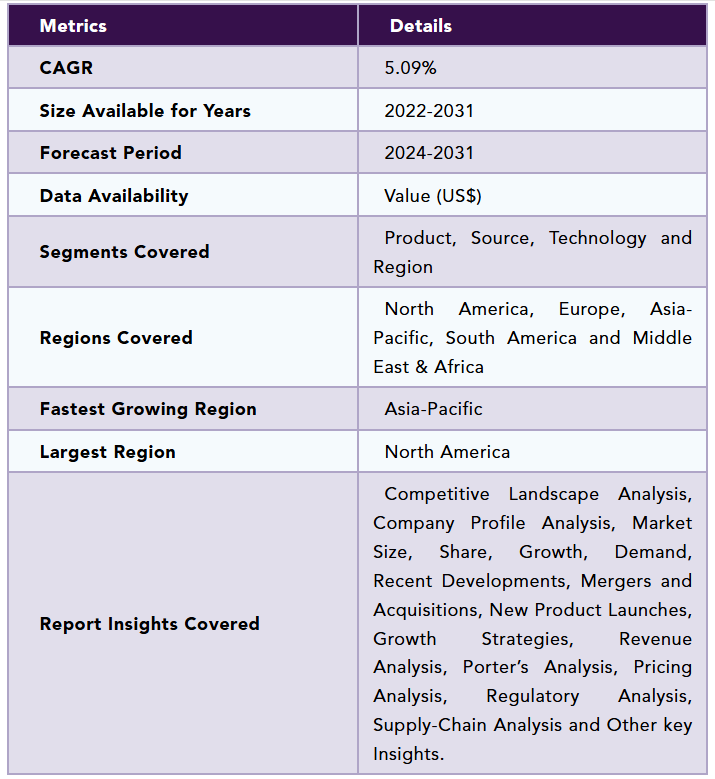

Global Sustainable Textile Fibers Market reached US$ 48.15 billion in 2023 and is expected to reach US$ 71.65 billion by 2031, growing with a CAGR of 5.09% during the forecast period 2024-2031.

The fashion business is experiencing a significant transition propelled by the increasing demand for sustainability and innovation. Although conventional textile fibers like cotton, polyester and wool have historically prevailed, their ecological repercussions have prompted the pursuit of more sustainable alternatives. Innovative textile fibers such as Mycotex, Piñatex and Orange Fibre are environmentally sustainable and frequently derived from food waste, providing a revolutionary alternative for the fashion industry.

The fibers offer environmentally sustainable alternatives without compromising quality or versatility. The transition to sustainable fibers additionally yields economic advantages for farmers and producers. Transforming agricultural by-products into useful materials generates supplementary revenue opportunities and establishes new markets for sustainable products. As customers grow more ecologically conscious, the demand for sustainable fashion is anticipated to increase.

Brands that use these new fibers can attract environmentally concerned consumers and differentiate themselves in a competitive marketplace. The future of the synthetic fiber market is expected to be influenced by a growing emphasis on sustainability. As sustainable fibers become more prevalent, the market share of conventional synthetic fibers may decline. This transition offers the textile sector a chance to develop and adapt, promoting a more sustainable and resilient market that advantages both the environment and the economy.

Dynamics

Rise of Sustainable Fibers and Ethical Manufacturing Practices

The textile business significantly contributes to environmental degradation due to its dependence on conventional fibers like cotton and polyester, which necessitate substantial water, chemicals and energy for manufacture. Moreover, in recent years, consumers have become progressively aware of the environmental and social ramifications of their purchase choices. Consequently, increased knowledge has resulted in a change in customer desire for items that are ethically sourced, environmentally sustainable and manufactured under equitable labor conditions.

In recent periods, about over 15% of the fabric utilized in garment manufacturing is discarded, contributing to post-industrial waste. Consequently, several prominent clothing brands such as H&M, Hanes and Adidas have included recycling procedures inside their production processes and supply chains, thereby addressing waste disposal challenges. The repurposing and recycling of discarded garments and fiber materials have surged in popularity in recent years. This has rendered the textile production cycle more sustainable.

Furthermore, sustainable fiber includes a variety of materials such as organic cotton, hemp, bamboo, lyocell and recycled polyester, among others. The fiber provides multiple environmental advantages, including less water usage, a reduced carbon footprint, biodegradability and limited application of pesticides and herbicides. The increasing demand for sustainable textiles propels the growth of the sustainable textile fiber market.

Growth in Environmental Impact

In recent years, sustainable textile fibers have aided climate stabilization by reducing CO2 emissions during manufacture. A recent Textile Exchange report on preferred fibers and materials reveals that cellulose fibers represent a considerable segment of the MMCF category, accounting for 6% of recycled MMCFs in the recent period, as they generate significantly lower emissions of pollutants and greenhouse gases during fabric production in comparison to synthetic fibers.

MMCFs are employed across many clothing categories, such as protective outerwear, home furnishings and fashion garments, to improve breathability, texture and luster, while principally alleviating negative skin reactions induced by toxic chemical fibers. Thus, the rising demand from the apparel sector is anticipated to propel the expansion of sustainable textile fibers.

The textile industry is one of the largest sectors worldwide, propelled by a growing population, rapid urbanization, rising disposable incomes and the increasing adoption of Western culture in developing countries such as China and India, along with ASEAN nations. Due to environmental concerns and stringent government regulations requiring manufacturing companies to reduce GHG emissions during production, the worldwide textile and apparel industries have witnessed increased demand for cellulosic fiber.

Recycling Difficulties

A significant issue is the insufficient infrastructure for textile recycling, especially in poorer nations, where textiles frequently gather in heaps, exacerbating environmental degradation instead of providing the expected supply chain advantages. This creates a detrimental cycle, wherein precious resources are squandered rather than recycled into new fibers, so diminishing the efficacy of textile recycling efforts. The intricacy of contemporary textiles, frequently composed of blended fibers like cotton and polyester, complicates the recycling procedure.

The separation of these combined materials is challenging, necessitating distinct processing techniques for each constituent. Consequently, the majority of textile recycling is confined to downcycling, wherein shredded fibers are converted into inferior items such as rags or carpet padding, instead of being reconstituted into high-quality fibers for new apparel. The absence of extensive, scalable recycling technology intensifies these challenges, hindering the shift towards a circular economy in the textile sector.

Segment Analysis

The global sustainable textile fibers market is segmented based on product, source, technology and region.

The Growing Demand For Eco-Friendly And Ethically Produced Textiles

Organic cotton is a key player in this subsegment, as it is grown using natural agricultural practices that avoid harmful chemicals, pesticides and genetically modified organisms (GMOs). This not only benefits the environment by promoting healthier soil and ecosystems but also provides a hypoallergenic, breathable and biodegradable fiber that is highly sought after by environmentally-conscious consumers.

The organic cotton production process focuses on resource conservation, using crop rotation and natural pest control, which further supports sustainable agriculture. To ensure transparency and accountability organic cotton products can be certified under the Global Organic Textile Standard (GOTS), which guarantees that textiles containing a minimum of 70% certified organic fibers (for the "made with organic" label) or 95% certified organic fibers (for the "organic" label) meet stringent environmental and social criteria.

In addition to organic cotton, other plant-based fibers such as hemp and bamboo are gaining popularity within the organic subsegment. Hemp, known for its minimal water usage and rapid growth, offers a highly durable and sustainable alternative to traditional fibers. Bamboo, with its fast growth cycle and low environmental impact, is also emerging as a key sustainable fiber. These fibers, along with organic cotton, align with the increasing demand for eco-conscious materials that contribute to reducing the environmental footprint of the textile industry.

Geographical Penetration

Growing Sustainable Clothing Demand In Asia-Pacific

The rising demand for clothing, together with a heightened necessity for sustainable fabrics in the Asia-Pacific region, is expected to propel market expansion. This tendency is anticipated to be more pronounced in major economies including India, China, Japan and Australia in the forthcoming years. India is set to become the fastest-growing market in the Asia Pacific region, driven by a burgeoning population, heightened per capita clothing consumption and escalating foreign investments.

The market is undergoing substantial growth in multiple emerging economies, propelled by heightened sustainability awareness, increasing disposable incomes and a rising inclination towards environmentally friendly raw materials in diverse applications such as textiles, home furnishings and industrial uses. Accelerated urbanization, along with increasing demand from the automotive and textile sectors, is propelling the adoption of eco fibers. In India, eco fibers are especially used in the textile and clothing industries, where they improve the quality and durability of various materials.

Competitive Landscape

The major global players in the market include Lenzing AG, US Fibers, Grasim Industries Ltd., Shanghai Tenbro Bamboo Textile Co. Ltd., China Bambro Textile (Group) Co., Ltd., Pilipinas Ecofiber Corporation, Teijin Limited, Foss Performance Materials, BASF and Södra.

Russia-Ukraine War Impact Analysis

The persistent conflict between Russia and Ukraine has resulted in considerable disturbances to global markets, particularly influencing the logistics and commodity sectors, so impacting the sustainable textile fiber industry. The escalating prices of vital commodities, such as crude oil, food and fuel, are contributing to rising inflation in major economies, especially in Europe.

This economic uncertainty is exerting pressure on Asian textile businesses dependent on raw resources from these regions. Prominent textile-exporting nations such as India, Bangladesh and China, which supply a substantial volume of items to Russia, are anticipated to experience a reduction in exports due to sanctions and trade limitations, leading to diminished revenue and heightened production expenses.

Moreover, the apparel retail industry has faced unparalleled difficulties as a result of the war. Numerous worldwide brands, such as H&M, Zara and Nike, have halted their activities in Russia, resulting in diminished demand for textile products in the area. This has generated a ripple effect throughout global supply networks, impacting the distribution of sustainable fibers.

Product

• Organic

• Manmade/Regenerated

• Recycled

• Natural

• Others

Source

• Plant-based

• Animal-based

• Recycled

Technology

• Eco-friendly Dyes

• Waterless Dyeing Technologies

• Biodegradable Fibers

• Closed-loop Production Systems

By Region

• North America

o US

o Canada

o Mexico

• Europe

o Germany

o UK

o France

o Italy

o Spain

o Rest of Europe

• South America

o Brazil

o Argentina

o Rest of South America

• Asia-Pacific

o China

o India

o Japan

o Australia

o Rest of Asia-Pacific

• Middle East and Africa

Key Developments

• In December 2022, the Lenzing Group and Renewcell, a Swedish innovator in textile-to-textile recycling, entered up a multi-year supply deal to expedite the textile industry's shift from a linear to a circular business model.

Why Purchase the Report?

• To visualize the global sustainable textile fibers market segmentation based on product, source, technology and region, as well as understand key commercial assets and players.

• Identify commercial opportunities by analyzing trends and co-development.

• Excel data sheet with numerous data points of the sustainable textile fibers market-level with all segments.

• PDF report consists of a comprehensive analysis after exhaustive qualitative interviews and an in-depth study.

• Product mapping available as excel consisting of key products of all the major players.

The global sustainable textile fibers market report would provide approximately 62 tables, 55 figures and 205 pages.

Target Audience 2024

• Manufacturers/ Buyers

• Industry Investors/Investment Bankers

• Research Professionals

• Emerging Companies

1. Methodology and Scope

1.1. Research Methodology

1.2. Research Objective and Scope of the Report

2. Definition and Overview

3. Executive Summary

3.1. Snippet by Product

3.2. Snippet by Source

3.3. Snippet by Technology

3.4. Snippet by Region

4. Dynamics

4.1. Impacting Factors

4.1.1. Drivers

4.1.1.1. Rise of Sustainable Fibers and Ethical Manufacturing Practices

4.1.1.2. Growth in Environmental Impact

4.1.2. Restraints

4.1.2.1. Recycling Difficulties

4.1.3. Opportunity

4.1.4. Impact Analysis

5. Industry Analysis

5.1. Porter's Five Force Analysis

5.2. Supply Chain Analysis

5.3. Pricing Analysis

5.4. Regulatory Analysis

5.5. Russia-Ukraine War Impact Analysis

5.6. DMI Opinion

6. COVID-19 Analysis

6.1. Analysis of COVID-19

6.1.1. Scenario Before COVID-19

6.1.2. Scenario During COVID-19

6.1.3. Scenario Post COVID-19

6.2. Pricing Dynamics Amid COVID-19

6.3. Demand-Supply Spectrum

6.4. Government Initiatives Related to the Market During Pandemic

6.5. Manufacturers Strategic Initiatives

6.6. Conclusion

7. By Product

7.1. Introduction

7.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product

7.1.2. Market Attractiveness Index, By Product

7.2. Organic*

7.2.1. Introduction

7.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

7.3. Manmade/Regenerated

7.4. Recycled

7.5. Natural

7.6. Others

8. By Source

8.1. Introduction

8.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Source

8.1.2. Market Attractiveness Index, By Source

8.2. Plant-based*

8.2.1. Introduction

8.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

8.3. Animal-based

8.4. Recycled

9. By Technology

9.1. Introduction

9.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

9.1.2. Market Attractiveness Index, By Technology

9.2. Eco-friendly Dyes*

9.2.1. Introduction

9.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

9.3. Waterless Dyeing Technologies

9.4. Biodegradable Fibers

9.5. Closed-loop Production Systems

10. By Region

10.1. Introduction

10.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Region

10.1.2. Market Attractiveness Index, By Region

10.2. North America

10.2.1. Introduction

10.2.2. Key Region-Specific Dynamics

10.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product

10.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Source

10.2.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

10.2.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.2.6.1. US

10.2.6.2. Canada

10.2.6.3. Mexico

10.3. Europe

10.3.1. Introduction

10.3.2. Key Region-Specific Dynamics

10.3.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product

10.3.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Source

10.3.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

10.3.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.3.6.1. Germany

10.3.6.2. UK

10.3.6.3. France

10.3.6.4. Italy

10.3.6.5. Spain

10.3.6.6. Rest of Europe

10.4. South America

10.4.1. Introduction

10.4.2. Key Region-Specific Dynamics

10.4.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product

10.4.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Source

10.4.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

10.4.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.4.6.1. Brazil

10.4.6.2. Argentina

10.4.6.3. Rest of South America

10.5. Asia-Pacific

10.5.1. Introduction

10.5.2. Key Region-Specific Dynamics

10.5.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Component

10.5.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product

10.5.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Source

10.5.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

10.5.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.5.7.1. China

10.5.7.2. India

10.5.7.3. Japan

10.5.7.4. Australia

10.5.7.5. Rest of Asia-Pacific

10.6. Middle East and Africa

10.6.1. Introduction

10.6.2. Key Region-Specific Dynamics

10.6.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product

10.6.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Source

10.6.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

11. Competitive Landscape

11.1. Competitive Scenario

11.2. Market Positioning/Share Analysis

11.3. Mergers and Acquisitions Analysis

12. Company Profiles

12.1. Lenzing AG*

12.1.1. Company Overview

12.1.2. Product Portfolio and Description

12.1.3. Financial Overview

12.1.4. Key Developments

12.2. US Fibers

12.3. Grasim Industries Ltd.

12.4. Shanghai Tenbro Bamboo Textile Co. Ltd.

12.5. China Bambro Textile (Group) Co., Ltd.

12.6. Pilipinas Ecofiber Corporation

12.7. Teijin Limited

12.8. Foss Performance Materials

12.9. BASF

12.10. Södra

LIST NOT EXHAUSTIVE

13. Appendix

13.1. About Us and Services

13.2. Contact Us

❖ 世界の持続可能なテキスタイル繊維市場に関するよくある質問(FAQ) ❖

・持続可能なテキスタイル繊維の世界市場規模は?

→DataM Intelligence社は2023年の持続可能なテキスタイル繊維の世界市場規模を481億5,000万米ドルと推定しています。

・持続可能なテキスタイル繊維の世界市場予測は?

→DataM Intelligence社は2031年の持続可能なテキスタイル繊維の世界市場規模を716億5,000万米ドルと予測しています。

・持続可能なテキスタイル繊維市場の成長率は?

→DataM Intelligence社は持続可能なテキスタイル繊維の世界市場が2024年~2031年に年平均5.1%成長すると予測しています。

・世界の持続可能なテキスタイル繊維市場における主要企業は?

→DataM Intelligence社は「Lenzing AG, US Fibers, Grasim Industries Ltd., Shanghai Tenbro Bamboo Textile Co. Ltd., China Bambro Textile (Group) Co., Ltd., Pilipinas Ecofiber Corporation, Teijin Limited, Foss Performance Materials, BASF and Södra.など ...」をグローバル持続可能なテキスタイル繊維市場の主要企業として認識しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、納品レポートの情報と少し異なる場合があります。