1. 方法論と範囲

1.1. 調査方法

1.2. 調査目的と調査範囲

2. 定義と概要

3. エグゼクティブ・サマリー

3.1. タイプ別スニペット

3.2. 薬剤クラス別スニペット

3.3. 投与経路別スニペット

3.4. 流通チャネル別スニペット

3.5. 地域別スニペット

4. ダイナミクス

4.1. 影響要因

4.1.1. 推進要因

4.1.1.1. 炎症性腸疾患の有病率の上昇

4.1.2. 阻害要因

4.1.2.1. 疾患管理の複雑さ

4.1.3. 機会

4.1.4. 影響分析

5. 産業分析

5.1. ポーターのファイブフォース分析

5.2. サプライチェーン分析

5.3. 価格分析

5.4. 規制分析

5.5. 償還分析

5.6. 特許分析

5.7. SWOT分析

5.8. DMI意見

6. タイプ別

6.1. はじめに

6.1.1. 市場規模分析および前年比成長率分析(%), タイプ別

6.1.2. 市場魅力度指数(タイプ別

6.2. 回腸炎*市場

6.2.1. 序論

6.2.2. 市場規模分析と前年比成長率分析(%)

6.3. 概要

6.4. 胃十二指腸クローン病

6.5. 腸炎

7. 薬剤クラス別

7.1. はじめに

7.1.1. 薬効分類別市場規模分析および前年比成長率分析(%) 7.1.2.

7.1.2. 市場魅力度指数(薬効分類別

7.2. 抗炎症薬*市場

7.2.1. 序論

7.2.2. 市場規模分析と前年比成長率分析(%)

7.3. 免疫抑制剤

7.4. 生物製剤

7.5. 抗生物質

7.6. 鎮痛剤

7.7. その他

8. 投与経路別

8.1. はじめに

8.1.1. 市場規模分析および前年比成長率分析(%)、投与経路別

8.1.2. 市場魅力度指数(投与経路別

8.2. 注射剤

8.2.1. 序論

8.2.2. 市場規模分析と前年比成長率分析(%)

8.3. 経口

9. 流通チャネル別

9.1. はじめに

9.1.1. 市場規模分析および前年比成長率分析(%), 流通チャネル別

9.1.2. 市場魅力度指数(流通チャネル別

9.2. 病院薬局

9.2.1. 序論

9.2.2. 市場規模分析と前年比成長率分析(%)

9.3. 小売薬局

9.4. オンライン薬局

10. 地域別

10.1. はじめに

10.1.1. 地域別市場規模分析および前年比成長率分析(%)

10.1.2. 市場魅力度指数、地域別

10.2. 北米

10.2.1. 序論

10.2.2. 地域別主要市場

10.2.2.1. 市場規模分析および前年比成長率分析(%), タイプ別

10.2.2.2. 市場規模分析および前年比成長率分析(%)、薬効分類別

10.2.2.3. 市場規模分析および前年比成長率分析(%)、投与経路別

10.2.2.4. 市場規模分析および前年比成長率分析(%):流通チャネル別

10.2.3. 市場規模分析および前年比成長率分析(%), 国別

10.2.3.1. 米国

10.2.3.2. カナダ

10.2.3.3. メキシコ

10.3. ヨーロッパ

10.3.1. はじめに

10.3.2. 地域別主要市場

10.3.2.1. 市場規模分析および前年比成長率分析(%), タイプ別

10.3.2.2. 市場規模分析およびYoY成長率分析(%)、薬物クラス別

10.3.2.3. 市場規模分析および前年比成長率分析(%)、投与経路別

10.3.2.4. 市場規模分析および前年比成長率分析(%):流通チャネル別

10.3.3. 市場規模分析および前年比成長率分析(%), 国別

10.3.3.1. ドイツ

10.3.3.2. イギリス

10.3.3.3. フランス

10.3.3.4. イタリア

10.3.3.5. スペイン

10.3.3.6. その他のヨーロッパ

10.4. 南米

10.4.1. はじめに

10.4.2. 地域別主要市場

10.4.2.1. 市場規模分析および前年比成長率分析(%), タイプ別

10.4.2.2. 市場規模分析および前年比成長率分析(%)、薬効分類別

10.4.2.3. 市場規模分析および前年比成長率分析(%)、投与経路別

10.4.2.4. 市場規模分析および前年比成長率分析(%):流通チャネル別

10.4.3. 市場規模分析および前年比成長率分析(%), 国別

10.4.3.1. ブラジル

10.4.3.2. アルゼンチン

10.4.3.3. その他の南米諸国

10.5. アジア太平洋

10.5.1. 序論

10.5.2. 主な地域別ダイナミクス

10.5.2.1. 市場規模分析および前年比成長率分析(%), タイプ別

10.5.2.2. 市場規模分析および前年比成長率分析(%)、薬効分類別

10.5.2.3. 市場規模分析および前年比成長率分析(%)、投与経路別

10.5.2.4. 市場規模分析および前年比成長率分析(%):流通チャネル別

10.5.3. 市場規模分析および前年比成長率分析(%), 国別

10.5.3.1. 中国

10.5.3.2. インド

10.5.3.3. 日本

10.5.3.4. 韓国

10.5.3.5. その他のアジア太平洋地域

10.6. 中東・アフリカ

10.6.1. 序論

10.6.2. 地域別主要市場

10.6.2.1. 市場規模分析および前年比成長率分析(%), タイプ別

10.6.2.2. 市場規模分析およびYoY成長率分析(%)、薬物クラス別

10.6.2.3. 市場規模分析および前年比成長率分析(%)、投与経路別

10.6.2.4. 市場規模分析および前年比成長率分析(%)、流通チャネル別

11. 競合情勢

11.1. 競争シナリオ

11.2. 市場ポジショニング/シェア分析

11.3. M&A分析

12. 企業プロフィール

12.1. Biogen*

12.1.1. Company Overview

12.1.2. Product Portfolio and Description

12.1.3. Financial Overview

12.1.4. Key Developments

12.2. Merck & Co

12.3. Novartis AG

12.4. Janssen Biotech, Inc

12.5. Takeda Pharmaceuticals

12.6. UCB S.A

12.7. AbbVie

12.8. Prometheus Laboratories

リストは網羅的ではありません

13. 付録

13.1. 会社概要とサービス

13.2. お問い合わせ

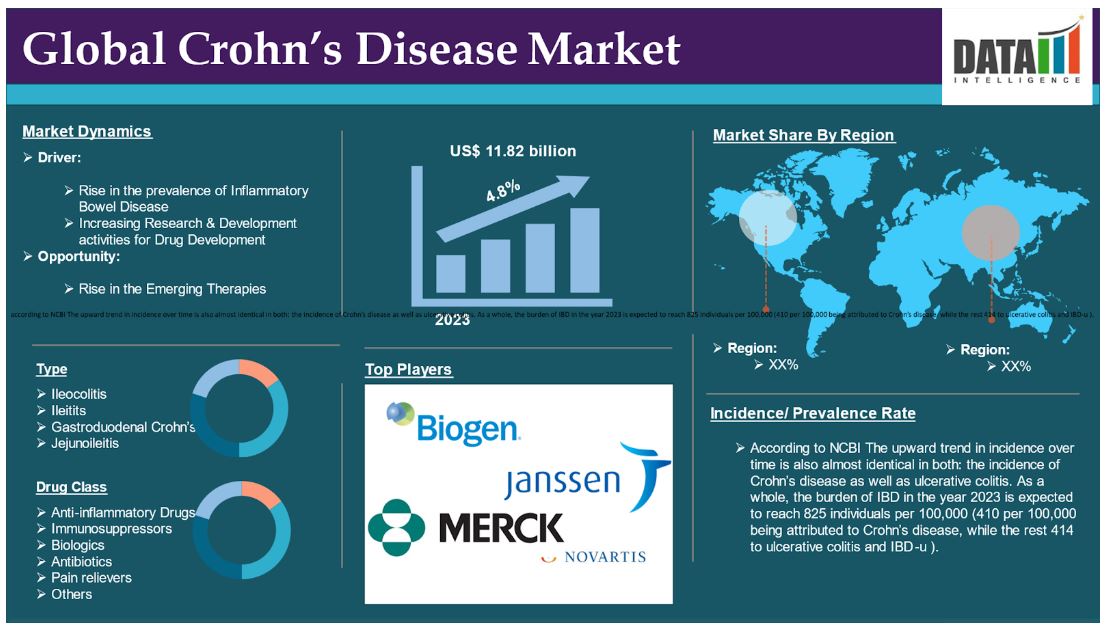

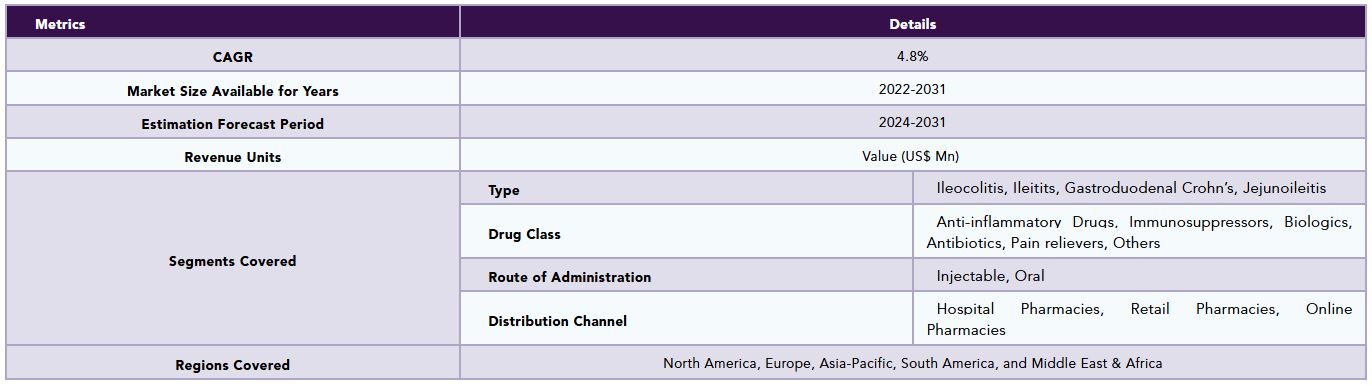

The global crohn's disease market reached US$ 11.82 billion in 2023 and is expected to reach US$ 17.15 billion by 2031, growing at a CAGR of 4.8% during the forecast period 2024-2031.

Crohn's disease is one of the inflammatory bowel diseases (IBD) which is marked by an illness in the intesines. It presents itself with symptoms like stomach ache, extreme bowel movement, tiredness, loss of appetite which leads to weight loss and malnourishment. There are the inflammation which is majorly in a part of the intestines that are also complicated by deeper layers of the bowel. This disease can be very painful, disabling, and sometimes, even deadly as it may attack different parts of the digestive system.

Market Dynamics: Drivers & Restraints

Rise in the Prevalence of Inflammatory Bowel Disease

Globally, the increase in the number of chronic digestive illnesses like IBS and IBD has led to a surge for products which are good for the gut. It is worryingly prevalent due to inflammation and disturbance caused by the gut microbiome and it is an example of IBD.

For instance, according to NCBI The upward trend in incidence over time is also almost identical in both: the incidence of Crohn’s disease as well as ulcerative colitis. As a whole, the burden of IBD in the year 2023 is expected to reach 825 individuals per 100,000 (410 per 100,000 being attributed to Crohn’s disease, while the rest 414 to ulcerative colitis and IBD-u ).

In Canada, this amount equates to approximately 322,600 IBD cases in a population where the prevalence is 0.82%. It is posited that by 2035 the proportion will rise to 1.08% of the population or 470,000 Canadians will have IBD. The prevalence across the age strata was projected to show a much higher increase. The elderly had the highest AAPC where the incidence was 841 per 100,000 in the year 2014 and is expected to rise to 1534 per 100,000 in the year 2035.

Moreover, Research conducted by Crohn’s & Colitis UK in 2022 suggests 1 in every 123 people in the UK have either Crohn’s disease or ulcerative colitis. This amounts to a total of nearly half a Billion people in the UK living with IBD. Therefore, although IBD is not that common, it still impacts a significant amount of people in the UK.

Complexity of Disease Management

The global market for Crohn's disease faces challenges in disease management due to its complexities and the large continuum of patients with different symptoms and treatment responses. This makes it difficult for healthcare providers to implement tailored treatment protocols, often requiring combinations of drugs and surgery. The cost and complexity of care management also discourage patients from completing treatment, further restricting market growth.

Segment Analysis

The global crohn’s disease market is segmented based on type, drug class, route of administration, distribution channel and region.

Drug Class:

Anti-inflammatory Drugs segment is expected to dominate the market share

The anti-inflammatory drugs segment are expected to hold a significant portion of the market share. Medication therapy is very important in controlling symptoms of Crohn's disease, particularly in this case the anti-inflammatory medication which aims at reducing inflammation within the gastrointestinal tract so as to relieve the symptoms and also avert active disease more so flare-ups.

These drugs which include aminosalicylates (e.g., mesalamine) and corticosteroids (prednisone) are common at the initiation of the disease or in mild to moderate exacerbations. Aminosalicylates help reduce the inflammation at the mucosal layer of the intestines.

The use of corticosteroids also has a significant beneficial effect in inducing remission than placebo and other agents such as 5-aminosalicylic acids (5-ASA) , Treatment of most studies indicates that they can help reach remission rates almost twice those of placebo treatments1. More so, they are at their maximal efficiency when used for a long period (more than 15 weeks) and for most patients will resolve symptoms in a matter of days.

Aminosalicylates, a first-line treatment for UC, contain the ingredient 5-aminosalicylic acid (5-ASA). These drugs, including mesalamine, olsalazine, balsalazide, and sulfasalazine, help reduce inflammation in the intestine and are best for mild to moderate UC. The American Gastroenterological Association (AGA) recommends adults with mild to moderate UC take a standard dose of oral mesalamine, olsalazine, or balsalazide instead of low dose mesalamine or sulfasalazine or no treatment.

Biologics segment is the fastest-growing segment in the crohn’s disease market share

Biologics have significantly improved the global Crohn's disease treatment by offering targeted, effective options for managing moderate to severe cases. These therapies, including TNF inhibitors, integrin inhibitors, and IL blockers, modulate the immune system to reduce inflammation and prevent disease flare-ups. They are especially beneficial for patients who do not respond well to conventional treatments, as they maintain remission and reduce the need for corticosteroids. Their efficacy in minimizing gut damage, enhancing quality of life, and potentially reducing hospitalization rates has led to their increased adoption and development.

For instance, in October 2024, Johnson & Johnson released data showcasing TREMFYA (guselkumab), in Crohn’s disease (CD) and ulcerative colitis (UC) with high rates of endoscopic remission in both biologic-naive and biologic-refractory patients (including UC patients who are JAK-inhibitor refractory), meaning the intestinal mucosa appeared uninflammed.

Route of Administration:

Injectable segment is expected to dominate the crohn’s disease market share

Injectable route of administration are of utmost importance especially in cases where moderate to severe therapies are required. Injectable biologics, which include therapies such as adalimumab, a TNF inhibitor, are generally given via the subcutaneous or intravenous routes and help regulate inflammation. These treatment modalities are indicated for patients who experienced a poor response to standard oral therapies, since these intravenous drugs rapidly resolve symptoms and help to attain and sustain remission. The injectable form of the treatment ensures excellent bioavailability thereby making it possible to taper disease symptom and progression to the level where hospitalization would not be needed.

Oral segment is the fastest-growing segment in the crohn’s disease market share

Oral therapy is an important component in the treatment of Crohn's disease at both the initial and maintenance stages for mild to moderate cases. They include aminosalicylates, corticosteroids, and immunomodulators, which help reduce inflammation and prevent flares from occurring in patients with mild disease. Oral formulations have the advantage of a non-invasive mode of administration thereby promoting patient compliance as the drugs do not require clinical visits. With recent advancements, newer oral therapies, including small-molecule inhibitors, are emerging, which provide targeted action with fewer adverse reactions than conventional medications.

For instance, in May 2023, a new treatment option for moderate-to-severe Crohn's disease patients has been approved by the Food and Drug Administration. The once-daily oral medication, upadacitinib, suppresses intestinal inflammation and painful symptoms, helping patients achieve and maintain clinical and endoscopic remission. The study was published in The New England Journal of Medicine.

Geographical Analysis

North America is expected to hold a significant position in the Crohn’s Disease market share

North America is expected to hold a significant position in the global Crohn’s Disease market during the forecast period due to the novel drugs launches, FDA approvals, ongoing clinical trials, high prevalence of crohn’s disease cases in the region and other factors help the region to grow during the forecast period.

For instance, in June 2024, AbbVie declared that the Food and Drug Administration (FDA) in the United States has approved SKYRIZI (risankizumab-rzaa) for adults suffering from moderate to severe ulcerative colitis and moderate to severe Crohn's disease. It is anticipated that this launch strategy will assist the organization in diversifying its range of products.

Moreover, in October 2023, Eli Lilly and Company has announced that in VIVID-1, a Phase 3 study investigating the safety and efficacy of mirikizumab for adult patients with moderately to severely active Crohn’s disease, an investigational interleukin-23p19 antagonist protocolled as mirikizumab has succeeded in meeting the co-primary and all centrala secondary endpoints as compared to placebo. The double-blind, treat-through trial included mirikizumab, placebo and active control (ustekinumab) arms.

Asia-Pacific is growing at the fastest pace in the crohn’s disease market

Asia-Pacific holds the fastest pace in the crohn’s disease market and is expected to hold most of the market share due to increasing prevalence of inflammatory bowel diseases and increased awareness. Moreover, partnership, agreements, westernized lifestyles, high in processed foods and lower in fiber, have led to a rise in gastrointestinal disorders, including Crohn's disease. Improved healthcare infrastructure and access to advanced diagnostic tools have led to earlier diagnoses and increased demand for effective treatments.

For instance, in August 2024, Biocon Biologics has signed a settlement and license agreement with Janssen Biotech Inc., Janssen Sciences Ireland, and Johnson & Johnson to resolve patent disputes and commercialize its biosimilar, Bmab 1200, in Europe, the UK, Canada, and Japan. The settlement secures market entry dates in these regions, and Biocon's regulatory filings are currently under review. Bmab 1200 is a proposed biosimilar to Janssen's Stelara, used for treating conditions like psoriasis, Crohn's disease, and psoriatic arthritis.

Market Segmentation

By Type

• Ileocolitis

• Ileitits

• Gastroduodenal Crohn’s

• Jejunoileitis

By Drug Class

• Anti-inflammatory Drugs

o Corticosteroids

o Oral 5-aminosalicylates

• Immunosuppressors

o Azathioprine

o Methotrexate

• Biologics

o Vedolizumab

o Infliximab

o Ustekinumab

o Others

• Antibiotics

• Pain relievers

• Others

By Route of Administration

• Injectable

• Oral

By Distribution Channel

• Hospital Pharmacies

• Retail Pharmacies

• Online Pharmacies

By Region

• North America

o The U.S.

o Canada

o Mexico

• Europe

o Germany

o UK

o France

o Italy

o Spain

o Rest of Europe

• South America

o Brazil

o Argentina

o Rest of South America

• Asia-Pacific

o China

o India

o Japan

o South Korea

o Rest of Asia-Pacific

• Middle East and Africa

Competitive Landscape

The major global players in the market include Biogen , Merck & Co, Novartis AG, Janssen Biotech, Inc, Takeda Pharmaceuticals , UCB S.A, AbbVie, Prometheus Laboratories among others.

Key Developments

• In July 2024, Teva Pharmaceuticals and Sanofi have adjusted the timing for the anti-TL1A, duvakitug program, which aims to treat moderate-to-severe IBD. The RELIEVE UCCD Phase 2b trial has completed early due to patient recruitment, and topline results for both ulcerative colitis and crohn's disease are expected in Q4 2024. The study replaces the previously planned interim analysis for the second half of 2024. Teva and Sanofi are collaborating to co-develop and co-commercialize duvakitug for moderate-to-severe UC and CD patients.

Why Purchase the Report?

• To visualize the global crohn’s disease market segmentation based on type, drug class, route of administration, distribution channel, and region as well as understand key commercial assets and players.

• Identify commercial opportunities by analyzing trends and co-development.

• Excel data sheet with numerous data points of crohn’s disease market-level with all segments.

• PDF report consists of a comprehensive analysis after exhaustive qualitative interviews and an in-depth study.

• Product mapping available as Excel consisting of key products of all the major players.

The global crohn’s disease market report would provide approximately 70 tables, 69 figures, and 202 pages.

Target Audience 2023

• Manufacturers/ Buyers

• Industry Investors/Investment Bankers

• Research Professionals

• Emerging Companies

1. Methodology and Scope

1.1. Research Methodology

1.2. Research Objective and Scope of the Report

2. Definition and Overview

3. Executive Summary

3.1. Snippet by Type

3.2. Snippet by Drug Class

3.3. Snippet by Route of Administration

3.4. Snippet by Distribution Channel

3.5. Snippet by Region

4. Dynamics

4.1. Impacting Factors

4.1.1. Drivers

4.1.1.1. Rise in the prevalence of Inflammatory Bowel Disease

4.1.2. Restraints

4.1.2.1. Complexity of Disease Management

4.1.3. Opportunity

4.1.4. Impact Analysis

5. Industry Analysis

5.1. Porter's Five Force Analysis

5.2. Supply Chain Analysis

5.3. Pricing Analysis

5.4. Regulatory Analysis

5.5. Reimbursement Analysis

5.6. Patent Analysis

5.7. SWOT Analysis

5.8. DMI Opinion

6. By Type

6.1. Introduction

6.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

6.1.2. Market Attractiveness Index, By Type

6.2. Ileocolitis*

6.2.1. Introduction

6.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

6.3. Ileitits

6.4. Gastroduodenal Crohn’s

6.5. Jejunoileitis

7. By Drug Class

7.1. Introduction

7.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Drug Class

7.1.2. Market Attractiveness Index, By Drug Class

7.2. Anti-inflammatory Drugs*

7.2.1. Introduction

7.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

7.3. Immunosuppressors

7.4. Biologics

7.5. Antibiotics

7.6. Pain relievers

7.7. Others

8. By Route of Administration

8.1. Introduction

8.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Route of Administration

8.1.2. Market Attractiveness Index, By Route of Administration

8.2. Injectable*

8.2.1. Introduction

8.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

8.3. Oral

9. By Distribution Channel

9.1. Introduction

9.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Distribution Channel

9.1.2. Market Attractiveness Index, By Distribution Channel

9.2. Hospital Pharmacies*

9.2.1. Introduction

9.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

9.3. Retail Pharmacies

9.4. Online Pharmacies

10. By Region

10.1. Introduction

10.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Region

10.1.2. Market Attractiveness Index, By Region

10.2. North America

10.2.1. Introduction

10.2.2. Key Region-Specific Dynamics

10.2.2.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

10.2.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%), By Drug Class

10.2.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Route of Administration

10.2.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Distribution Channel

10.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.2.3.1. The U.S.

10.2.3.2. Canada

10.2.3.3. Mexico

10.3. Europe

10.3.1. Introduction

10.3.2. Key Region-Specific Dynamics

10.3.2.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

10.3.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%), By Drug Class

10.3.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Route of Administration

10.3.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Distribution Channel

10.3.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.3.3.1. Germany

10.3.3.2. UK

10.3.3.3. France

10.3.3.4. Italy

10.3.3.5. Spain

10.3.3.6. Rest of Europe

10.4. South America

10.4.1. Introduction

10.4.2. Key Region-Specific Dynamics

10.4.2.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

10.4.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%), By Drug Class

10.4.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Route of Administration

10.4.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Distribution Channel

10.4.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.4.3.1. Brazil

10.4.3.2. Argentina

10.4.3.3. Rest of South America

10.5. Asia-Pacific

10.5.1. Introduction

10.5.2. Key Region-Specific Dynamics

10.5.2.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

10.5.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%), By Drug Class

10.5.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Route of Administration

10.5.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Distribution Channel

10.5.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.5.3.1. China

10.5.3.2. India

10.5.3.3. Japan

10.5.3.4. South Korea

10.5.3.5. Rest of Asia-Pacific

10.6. Middle East and Africa

10.6.1. Introduction

10.6.2. Key Region-Specific Dynamics

10.6.2.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

10.6.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%), By Drug Class

10.6.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Route of Administration

10.6.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Distribution Channel

11. Competitive Landscape

11.1. Competitive Scenario

11.2. Market Positioning/Share Analysis

11.3. Mergers and Acquisitions Analysis

12. Company Profiles

12.1. Biogen*

12.1.1. Company Overview

12.1.2. Product Portfolio and Description

12.1.3. Financial Overview

12.1.4. Key Developments

12.2. Merck & Co

12.3. Novartis AG

12.4. Janssen Biotech, Inc

12.5. Takeda Pharmaceuticals

12.6. UCB S.A

12.7. AbbVie

12.8. Prometheus Laboratories

LIST NOT EXHAUSTIVE

13. Appendix

13.1. About Us and Services

13.2. Contact Us

❖ 世界のクローン病市場に関するよくある質問(FAQ) ❖

・クローン病の世界市場規模は?

→DataM Intelligence社は2023年のクローン病の世界市場規模を118.2億米ドルと推定しています。

・クローン病の世界市場予測は?

→DataM Intelligence社は2031年のクローン病の世界市場規模を171.5億米ドルと予測しています。

・クローン病市場の成長率は?

→DataM Intelligence社はクローン病の世界市場が2024年~2031年に年平均4.8%成長すると予測しています。

・世界のクローン病市場における主要企業は?

→DataM Intelligence社は「Biogen , Merck & Co, Novartis AG, Janssen Biotech, Inc, Takeda Pharmaceuticals , UCB S.A, AbbVie, Prometheus Laboratoriesなど ...」をグローバルクローン病市場の主要企業として認識しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、納品レポートの情報と少し異なる場合があります。