1. 方法論と範囲

1.1. 調査方法

1.2. 調査目的と調査範囲

2. 定義と概要

3. エグゼクティブ・サマリー

3.1. タイプ別スニペット

3.2. 用途別スニペット

3.3. 流通チャネル別スニペット

3.4. 地域別スニペット

4. ダイナミクス

4.1. 影響要因

4.1.1. 推進要因

4.1.1.1. がん罹患率の増加

4.1.1.2. XX

4.1.2. 阻害要因

4.1.2.1. 高額な治療費

4.1.3. 機会

4.1.4. 影響分析

5. 産業分析

5.1. ポーターのファイブフォース分析

5.2. サプライチェーン分析

5.3. 価格分析

5.4. 規制分析

6. タイプ別

6.1. はじめに

6.1.1. タイプ別分析と前年比成長率分析(%)

6.1.2. 市場魅力度指数, タイプ別

6.2. PD-1阻害剤

6.2.1. 序論

6.2.2. 市場規模分析と前年比成長率分析(%)

6.2.3. ペムブロリズマブ

6.2.4. ニボルマブ

6.2.5. セミピリマブ

6.3. PD-L1阻害薬

6.3.1. アテゾリズマブ

6.3.2. アベルマブ

6.3.3. デュルバルマブ

6.4. CTLA-4阻害剤

6.4.1. イピリムマブ

6.4.2. トレメリムマブ

6.5. LAG-3阻害薬(レラトリマブ)

6.6. その他

7. 用途別

7.1. 導入

7.1.1. 市場規模分析および前年比成長率分析(%), アプリケーション別

7.1.2. 市場魅力度指数:用途別

7.2. 乳がん

7.2.1. はじめに

7.2.2. 市場規模分析と前年比成長率分析(%)

7.3. 膀胱がん

7.4. 子宮頸がん

7.5. 大腸がん

7.6. ホジキンリンパ腫

7.7. 肝臓がん

7.8. 肺がん

7.9. その他

8. 販売チャネル別

8.1. はじめに

8.1.1. 市場規模分析および前年比成長率分析(%), 流通チャネル別

8.1.2. 市場魅力度指数(流通チャネル別

8.2. 病院薬局

8.2.1. はじめに

8.2.2. 市場規模分析と前年比成長率分析(%)

8.3. 小売薬局

8.4. オンライン薬局

9. 地域別

9.1. はじめに

9.1.1. 地域別市場規模分析および前年比成長率分析(%)

9.1.2. 市場魅力度指数、地域別

9.2. 北米

9.2.1. 序論

9.2.2. 主な地域別ダイナミクス

9.2.3. 市場規模分析および前年比成長率分析(%), タイプ別

9.2.4. 市場規模分析とYoY成長率分析(%)、用途別

9.2.5. 市場規模分析および前年比成長率分析(%), 流通チャネル別

9.2.6. 市場規模分析および前年比成長率分析(%), 国別

9.2.6.1. 米国

9.2.6.2. カナダ

9.2.6.3. メキシコ

9.3. ヨーロッパ

9.3.1. はじめに

9.3.2. 主な地域別動向

9.3.3. 市場規模分析および前年比成長率分析(%), タイプ別

9.3.4. 市場規模分析とYoY成長率分析(%)、用途別

9.3.5. 市場規模分析および前年比成長率分析(%), 流通チャネル別

9.3.6. 市場規模分析および前年比成長率分析(%), 国別

9.3.6.1. ドイツ

9.3.6.2. イギリス

9.3.6.3. フランス

9.3.6.4. スペイン

9.3.6.5. イタリア

9.3.6.6. その他のヨーロッパ

9.4. 南米

9.4.1. はじめに

9.4.2. 地域別主要市場

9.4.3. 市場規模分析および前年比成長率分析(%), タイプ別

9.4.4. 市場規模分析とYoY成長率分析(%)、用途別

9.4.5. 市場規模分析および前年比成長率分析(%), 流通チャネル別

9.4.6. 市場規模分析および前年比成長率分析(%), 国別

9.4.6.1. ブラジル

9.4.6.2. アルゼンチン

9.4.6.3. その他の南米諸国

9.5. アジア太平洋

9.5.1. はじめに

9.5.2. 主な地域別ダイナミクス

9.5.3. 市場規模分析および前年比成長率分析(%), タイプ別

9.5.4. 市場規模分析および前年比成長率分析(%), アプリケーション別

9.5.5. 市場規模分析および前年比成長率分析(%), 流通チャネル別

9.5.6. 市場規模分析および前年比成長率分析(%), 国別

9.5.6.1. 中国

9.5.6.2. インド

9.5.6.3. 日本

9.5.6.4. 韓国

9.5.6.5. その他のアジア太平洋地域

9.6. 中東・アフリカ

9.6.1. 序論

9.6.2. 主な地域別ダイナミクス

9.6.3. 市場規模分析および前年比成長率分析(%), タイプ別

9.6.4. 市場規模分析とYoY成長率分析(%)、用途別

9.6.5. 市場規模分析および前年比成長率分析(%), 流通チャネル別

10. 競合情勢

10.1. 競争シナリオ

10.2. 市場ポジショニング/シェア分析

10.3. M&A分析

11. 企業プロフィール

11.1. Bristol-Myers Squibb Company. *

11.1.1. Company Overview

11.1.2. Product Portfolio and Description

11.1.3. Financial Overview

11.1.4. Key Developments

11.2. Merck & Co., Inc.

11.3. F. Hoffmann-La Roche Ltd

11.4. AstraZeneca

11.5. Regeneron Pharmaceuticals, Inc.

11.6. Eli Lilly and Company

11.7. BeiGene LTD.

11.8. GSK plc

11.9. Coherus BioSciences, Inc.

11.10. lncyte.

リストは網羅的ではありません

12. 付録

12.1. 会社概要とサービス

12.2. お問い合わせ

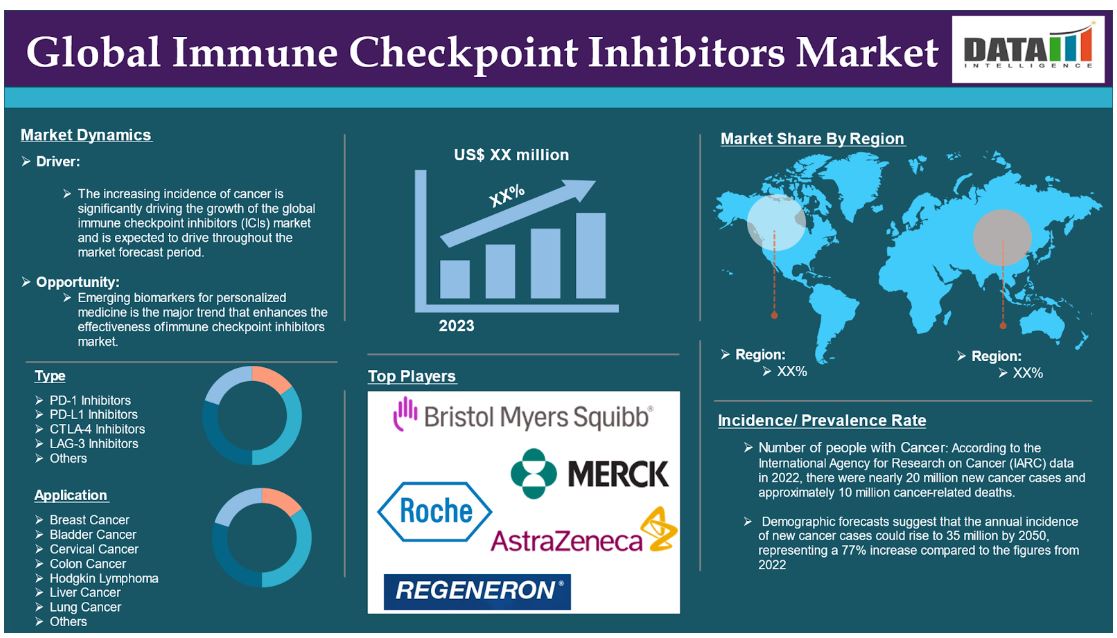

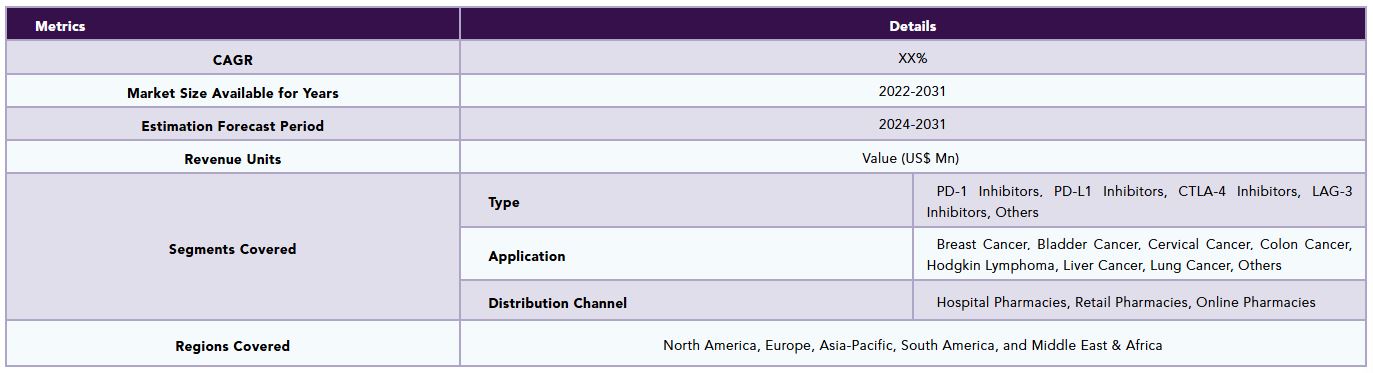

The global Immune Checkpoint Inhibitors market reached US$ 40.1 billion in 2023 and is expected to reach US$ 156.6 billion by 2031, growing at a CAGR of 16.5% during the forecast period 2024-2031.

Immune checkpoints are integral components of the immune system, designed to prevent an overly aggressive immune response that could harm healthy cells. These checkpoints come into play when proteins on T cells, a type of immune cell, recognize and bind to corresponding proteins on other cells, including some tumor cells. These partner proteins are known as immune checkpoint proteins. When the checkpoint proteins and their partners bind, they send an "off" signal to the T cells, which can inhibit the immune system's ability to attack cancer demands for the Immune checkpoint inhibitors (ICIs).

Immune checkpoint inhibitors (ICIs) are a class of immunotherapy drugs that function by blocking these checkpoint proteins from interacting with their partners. This blockade prevents the "off" signal from being transmitted, thereby enabling T cells to effectively target and eliminate cancer cells. These factors have driven the global immune checkpoint inhibitors (ICIs) market expansion.

Market Dynamics: Drivers & Restraints

Increasing incidence of cancer

The increasing incidence of cancer is significantly driving the growth of the global immune checkpoint inhibitors (ICIs) market and is expected to drive throughout the market forecast period.

Cancer is a rapidly advancing disease with a high mortality rate. In recent years, new therapeutic approaches, including targeted therapies and immunotherapies, have emerged as important complements to traditional treatments like surgery and radiation. The introduction of immunotherapy has significantly transformed cancer management. The development of immune checkpoint inhibitors (ICIs) has notably improved treatment outcomes for tumors.

Ongoing research in cancer immunology is focused on discovering innovative agents that can effectively stimulate immune responses against cancer. According to the International Agency for Research on Cancer (IARC) data in 2022, there were nearly 20 million new cancer cases and approximately 10 million cancer-related deaths. Demographic forecasts suggest that the annual incidence of new cancer cases could rise to 35 million by 2050, representing a 77% increase compared to the figures from 2022. This significant rise in the cancer burden is directly linked to the growing need for effective treatment options, such as immune checkpoint inhibitors (ICIs).

Furthermore, key players in the industry research studies and key developments that would propel this global immune checkpoint inhibitors (ICIs) market growth. For instance, according to the NCBI research study in February 2022, recent research has emphasized the importance of several factors in optimizing the immune response against tumors. These include the priming and activation of tumor-specific T cells in the draining lymph nodes, their subsequent migration to the tumor site, and the formation of tertiary lymphoid structures within the tumor environment. All these factors demand the global immune checkpoint inhibitors (ICIs) market.

Moreover, the rising demand for advancements in immunotherapy contributes to the global immune checkpoint inhibitors (ICIs) market expansion.

High cost of treatments

The high cost of treatments will hinder the growth of global immune checkpoint inhibitors (ICIs). The expenses associated with these therapies can significantly restrict patient access and impose a substantial financial burden on healthcare systems.

As per an NCBI research study in April 2023, overall spending and utilization of immune checkpoint inhibitors (ICIs) have surged dramatically over the past decade. From 2011 to 2021, expenditures rose from $2.8 million to $4.1 billion. During the same period, the number of prescriptions increased significantly, from just 94 to 462,049 in 2021, encompassing six different ICIs. The average spending per prescription indicative of the average drug price decreased by 70%, dropping from approximately $29,795.88 in 2011 to about $8,914.69 in 2021.

In addition, the overall cost of managing treatment-related toxicities further complicates the financial landscape. For instance, managing immune-related adverse events can add thousands of dollars to the total treatment cost, affecting the value-to-cost ratio of these therapies. As a result, the high costs associated with immune checkpoint inhibitors (ICIs) pose a significant barrier to their adoption and utilization in clinical practice. Thus, the above factors could be limiting the global immune checkpoint inhibitors (ICIs) market's potential growth.

Segment Analysis

The global immune checkpoint inhibitors (ICIs) market is segmented based on type, application, distribution channel, and region.

Type:

PD-1 inhibitors segment is expected to dominate the global immune checkpoint inhibitors (ICIs) market share

The PD-1 inhibitors segment holds a major portion of the global immune checkpoint inhibitors (ICIs) market share and is expected to continue to hold a significant portion of the global immune checkpoint inhibitors (ICIs) market share during the forecast period.

PD-1 is a checkpoint protein found in immune cells known as T cells. It functions as an "off switch" that helps prevent T cells from attacking other cells in the body. This occurs when PD-1 binds to PD-L1, a protein present in some normal and cancer cells. When PD-1 attaches to PD-L1, it signals the T cell to leave the other cell unharmed. Many cancer cells produce high levels of PD-L1, which allows them to evade detection by the immune system.

Furthermore, key players in the industry research studies and drug approvals that would drive this segment growth in the global immune checkpoint inhibitors (ICIs) market. For instance, according to the NCBI research study in February 2022, the primary limitation of currently available immune checkpoint inhibitors (ICIs), including PD-1 inhibitors, is that only about 10% to 20% of patients experience significant clinical benefits from these treatments. This low response rate highlights the need for improved strategies to enhance the effectiveness of immunotherapy. One promising approach is to combine different ICIs that have non-overlapping mechanisms of action, which may lead to increased clinical efficacy.

Also, in October 2024, the European Commission approved KEYTRUDA (pembrolizumab) in combination with chemotherapy for two new indications in gynecologic cancers, marking the 30th approval for this anti-PD-1 therapy. This includes the first approval in the European Union (EU) for an anti-PD-1 therapy combined with chemotherapy specifically for patients with primary advanced or recurrent endometrial carcinoma, regardless of their mismatch repair (MMR) status.

The European Commission's approval of KEYTRUDA in combination with chemotherapy for advanced or recurrent endometrial carcinoma underscores the growing role of immune checkpoint inhibitors (ICIs) in oncology. These factors have solidified the segment's position in the global immune checkpoint inhibitors (ICIs) market.

PD-L1 inhibitors segment is the fastest-growing segment in the global immune checkpoint inhibitors (ICIs) market share

The PD-L1 inhibitors segment is the fastest-growing segment in the global immune checkpoint inhibitors (ICIs) market share and is expected to hold the market share over the forecast period.

PD-L1 is a protein that functions as a type of "brake" to regulate the body's immune responses. It is present in some normal cells and is found in elevated levels in certain cancer cells. When PD-L1 binds to PD-1, a protein located in T cells, it signals the T cells to refrain from attacking the PD-L1-expressing cells, including cancer cells. Immune checkpoint inhibitors are anticancer drugs that target PD-L1, blocking its interaction with PD-1. This action effectively releases the "brakes" on the immune system, allowing T cells to recognize and destroy cancer cells.

Monoclonal antibodies that target either PD-1 or PD-L1 can block this interaction, thereby enhancing the immune response against cancer cells. By inhibiting the binding of PD-1 to PD-L1, these therapies reactivate T cells, enabling them to recognize and attack tumors more effectively. These factors have solidified the segment's position in the global immune checkpoint inhibitors (ICIs) market.

Application :

Lung cancer segment is expected to dominate the global immune checkpoint inhibitors (ICIs) market share

The lung cancer segment holds a major portion of the global immune checkpoint inhibitors (ICIs) market share and is expected to continue to hold a significant portion of the global immune checkpoint inhibitors (ICIs) market share during the forecast period.

The incidence of lung cancer needs a substantial demand for effective treatment options, including immune checkpoint inhibitors (ICIs). Lung cancer is a leading cause of mortality, there is an urgent need for therapies that can improve survival rates and quality of life for affected patients.

A recent collaborative report from researchers at the International Agency for Research on Cancer (IARC) and the American Cancer Society (ACS) presents the global cancer statistics for 2022. The report indicates that lung cancer was the most frequently diagnosed cancer globally in 2022, accounting for nearly 2.5 million new cases, which represents about 12.4% of all cancers worldwide. Following lung cancer, breast cancer and colorectal cancer were the next most common, with incidences of 11.6% and 9.6%, respectively. Additionally, lung cancer was the leading cause of cancer-related deaths, responsible for an estimated 1.8 million deaths (approximately 18.7% of total cancer deaths), followed by colorectal cancer (9.3%) and liver cancer (7.8%).

Immune checkpoint inhibitors (ICIs) such as pembrolizumab (Keytruda) and nivolumab (Opdivo) have been approved for the treatment of non-small cell lung cancer (NSCLC), demonstrating improved outcomes compared to traditional therapies. The effectiveness of these drugs in treating lung cancer reinforces their importance in the oncology market and drives investment in further research and development. These factors have solidified the segment's position in the global immune checkpoint inhibitors (ICIs) market.

Bladder cancer segment is the fastest-growing segment in the global immune checkpoint inhibitors (ICIs) market share

The bladder cancer segment is the fastest-growing segment in the global immune checkpoint inhibitors (ICIs) market share and is expected to hold the market share over the forecast period.

Bladder cancer is a major public health issue and is the leading cause of cancer-related deaths worldwide. It ranks as the ninth most common cancer globally and is the second most prevalent urinary tract malignancy, with approximately 549,000 new cases and around 200,000 deaths each year. The incidence and mortality rates for bladder cancer vary significantly across different regions, with the highest rates observed in Western countries, particularly in North America and Europe.

In the United States, bladder cancer is the sixth most frequently diagnosed cancer, accounting for about 3% of all cancers reported globally. In 2023, it is estimated that there will be over 80,000 new cases and more than 16,000 deaths attributed to this disease. The five-year survival rates for bladder cancer are approximately 70% for localized cases, 39.2% for regional cases, and less than 10% for those with distant metastases. Thus, all these factors demand for immune checkpoint inhibitors (ICIs).

According to an NCBI research publication in June 2023, bladder cancer is a prevalent condition with limited treatment options for advanced stages. However, immune checkpoint inhibitors (ICIs) targeting proteins like cytotoxic T-lymphocyte-associated antigen-4 (CTLA-4) and programmed cell death-1 (PD-1) have shown significant promise in managing this disease. These drugs function by blocking the interactions between receptors and ligands, disrupting the signaling pathways that typically inhibit T cell activity, thus allowing T cells to identify and attack cancer cells more effectively. These factors have solidified the segment's global position in the immune checkpoint inhibitors (ICIs) market.

Geographical Analysis

North America is expected to hold a significant position in the global immune checkpoint inhibitors (ICIs) market share

North America holds a substantial position in the global immune checkpoint inhibitors (ICIs) market and is expected to hold most of the market share.

The rise in cancer cases demands a significant and growing patient population that requires effective treatment options. The increasing burden of cancer directly correlates with the rising demand for immune checkpoint inhibitors (ICIs), which have shown promise in improving patient outcomes across multiple cancer types.

According to National Cancer Institute data in the United States, it is projected that 2,001,140 new cases of cancer will be diagnosed in 2024, alongside an estimated 611,720 deaths from the disease. This high incidence rate underscores the urgent need for innovative therapies, particularly immune checkpoint inhibitors (ICIs), which have demonstrated effectiveness in treating a variety of cancers.

Furthermore, in this region, a major number of key players' presence, well-advanced healthcare infrastructure, government initiatives & regulatory support, technological advancements, & investment in immunotherapy centers, and product launches & approvals would propel this immune checkpoint inhibitor (ICIs) market growth.

For instance, in August 2024, the U.S. Food and Drug Administration (FDA) approved the Immune checkpoint inhibitors (ICIs) drug dostarlimab-gxly (brand name Jemperli) in combination with carboplatin and paclitaxel for the treatment of adult patients with primary advanced or recurrent endometrial cancer (EC).

This approval is particularly significant as it expands the use of dostarlimab-gxly beyond its previous indication, which was limited to patients with mismatch repair deficient (dMMR) or microsatellite instability-high (MSI-H) tumors. The expansion of dostarlimab-gxly’s indications reflects a growing trend in the immune checkpoint inhibitors (ICIs) market towards broader applications of existing therapies. Thus, the above factors are consolidating the region's position as a dominant force in the global immune checkpoint inhibitors (ICIs) market.

Asia Pacific is growing at the fastest pace in the global immune checkpoint inhibitors (ICIs) market

Asia Pacific holds the fastest pace in the global immune checkpoint inhibitors (ICIs) market and is expected to hold most of the market share.

In the Asia-Pacific region, the immune checkpoint inhibitors (ICIs) market is driven by factors such as the increasing prevalence of cancer, growing investments in research and developments related to cancer, increasing innovative and targeted treatment options, and advancements in antibody technologies.

Japan holds a major portion of the market share owing to the rising prevalence of cancer Japan is a significant driver for immune checkpoint inhibitors (ICIs), as these therapies offer targeted treatment options that can be more effective and less toxic than traditional chemotherapies.

This high incidence of cancer cases demands effective treatment options, including immune checkpoint inhibitors, which have shown significant efficacy in treating various cancers. As per Australian Institute of Health and Welfare reported that by 2024, it is projected that approximately 169,500 new cases of cancer will be diagnosed in Australia. This represents an increase of about 93% over the past 24 years, primarily driven by population growth and a rising number of individuals reaching older age groups, which are associated with higher cancer rates. Thus, the above factors are consolidating the region's position as the fastest-growing force in the global immune checkpoint inhibitors (ICIs) market.

Competitive Landscape

The major global players in the immune checkpoint inhibitors (ICIs) market include Bristol-Myers Squibb Company., Merck & Co., Inc., F. Hoffmann-La Roche Ltd, AstraZeneca, Regeneron Pharmaceuticals, Inc., Eli Lilly and Company, BeiGene LTD., GSK plc, Coherus BioSciences, Inc., and lncyte. among others.

Emerging Players

The emerging players in the global immune checkpoint inhibitors (ICIs) market include Immutep Limited, OncoC4., iTeos Therapeutics., and CureVac SE among others.

Key Developments

• In June 2024, the U.S. Food and Drug Administration (FDA) approved the Immune checkpoint inhibitors (ICIs) drug durvalumab (brand name Imfinzi) in combination with carboplatin and paclitaxel, followed by single-agent durvalumab, for the treatment of adult patients with primary advanced or recurrent endometrial cancer that is mismatch repair deficient (dMMR). The FDA's approval of durvalumab in combination with chemotherapy for dMMR advanced or recurrent endometrial cancer underscores the growing role of immune checkpoint inhibitors (ICIs) in oncology.

Why Purchase the Report?

• To visualize the global immune checkpoint inhibitors (ICIs) market segmentation based on type, application, distribution channel, and region and understand key commercial assets and players.

• Identify commercial opportunities by analyzing trends and co-development.

• Excel data sheet with numerous data points of the immune checkpoint inhibitors (ICIs) market with all segments.

• PDF report consists of a comprehensive analysis after exhaustive qualitative interviews and an in-depth study.

• Product mapping is available in excel consisting of key products of all the major players.

The global immune checkpoint inhibitors (ICIs) market report would provide approximately 62 tables, 59 figures, and 184 pages.

Target Audience 2023

• Manufacturers/ Buyers

• Industry Investors/Investment Bankers

• Research Professionals

• Emerging Companies

1. Methodology and Scope

1.1. Research Methodology

1.2. Research Objective and Scope of the Report

2. Definition and Overview

3. Executive Summary

3.1. Snippet by Type

3.2. Snippet by Application

3.3. Snippet by Distribution Channel

3.4. Snippet by Region

4. Dynamics

4.1. Impacting Factors

4.1.1. Drivers

4.1.1.1. Increasing Incidence of Cancer

4.1.1.2. XX

4.1.2. Restraints

4.1.2.1. High Cost of Treatments

4.1.3. Opportunity

4.1.4. Impact Analysis

5. Industry Analysis

5.1. Porter’s Five Force Analysis

5.2. Supply Chain Analysis

5.3. Pricing Analysis

5.4. Regulatory Analysis

6. By Type

6.1. Introduction

6.1.1. Analysis and Y-o-Y Growth Analysis (%), By Type

6.1.2. Market Attractiveness Index, By Type

6.2. PD-1 Inhibitors *

6.2.1. Introduction

6.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

6.2.3. Pembrolizumab

6.2.4. Nivolumab

6.2.5. Cemiplimab

6.3. PD-L1 Inhibitors

6.3.1. Atezolizumab

6.3.2. Avelumab

6.3.3. Durvalumab

6.4. CTLA-4 Inhibitors

6.4.1. Ipilimumab

6.4.2. Tremelimumab

6.5. LAG-3 Inhibitors (Relatlimab)

6.6. Others

7. By Application

7.1. Introduction

7.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

7.1.2. Market Attractiveness Index, By Application

7.2. Breast Cancer *

7.2.1. Introduction

7.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

7.3. Bladder Cancer

7.4. Cervical Cancer

7.5. Colon Cancer

7.6. Hodgkin Lymphoma

7.7. Liver Cancer

7.8. Lung Cancer

7.9. Others

8. By Distribution Channel

8.1. Introduction

8.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Distribution Channel

8.1.2. Market Attractiveness Index, By Distribution Channel

8.2. Hospital Pharmacies *

8.2.1. Introduction

8.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

8.3. Retail Pharmacies

8.4. Online Pharmacies

9. By Region

9.1. Introduction

9.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Region

9.1.2. Market Attractiveness Index, By Region

9.2. North America

9.2.1. Introduction

9.2.2. Key Region-Specific Dynamics

9.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

9.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.2.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Distribution Channel

9.2.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

9.2.6.1. U.S.

9.2.6.2. Canada

9.2.6.3. Mexico

9.3. Europe

9.3.1. Introduction

9.3.2. Key Region-Specific Dynamics

9.3.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

9.3.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.3.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Distribution Channel

9.3.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

9.3.6.1. Germany

9.3.6.2. U.K.

9.3.6.3. France

9.3.6.4. Spain

9.3.6.5. Italy

9.3.6.6. Rest of Europe

9.4. South America

9.4.1. Introduction

9.4.2. Key Region-Specific Dynamics

9.4.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

9.4.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.4.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Distribution Channel

9.4.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

9.4.6.1. Brazil

9.4.6.2. Argentina

9.4.6.3. Rest of South America

9.5. Asia-Pacific

9.5.1. Introduction

9.5.2. Key Region-Specific Dynamics

9.5.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

9.5.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.5.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Distribution Channel

9.5.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

9.5.6.1. China

9.5.6.2. India

9.5.6.3. Japan

9.5.6.4. South Korea

9.5.6.5. Rest of Asia-Pacific

9.6. Middle East and Africa

9.6.1. Introduction

9.6.2. Key Region-Specific Dynamics

9.6.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

9.6.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.6.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Distribution Channel

10. Competitive Landscape

10.1. Competitive Scenario

10.2. Market Positioning/Share Analysis

10.3. Mergers and Acquisitions Analysis

11. Company Profiles

11.1. Bristol-Myers Squibb Company. *

11.1.1. Company Overview

11.1.2. Product Portfolio and Description

11.1.3. Financial Overview

11.1.4. Key Developments

11.2. Merck & Co., Inc.

11.3. F. Hoffmann-La Roche Ltd

11.4. AstraZeneca

11.5. Regeneron Pharmaceuticals, Inc.

11.6. Eli Lilly and Company

11.7. BeiGene LTD.

11.8. GSK plc

11.9. Coherus BioSciences, Inc.

11.10. lncyte.

LIST NOT EXHAUSTIVE

12. Appendix

12.1. About Us and Services

12.2. Contact Us

❖ 世界の免疫チェックポイント阻害薬(ICI)市場に関するよくある質問(FAQ) ❖

・免疫チェックポイント阻害薬(ICI)の世界市場規模は?

→DataM Intelligence社は2023年の免疫チェックポイント阻害薬(ICI)の世界市場規模を401億米ドルと推定しています。

・免疫チェックポイント阻害薬(ICI)の世界市場予測は?

→DataM Intelligence社は2031年の免疫チェックポイント阻害薬(ICI)の世界市場規模を1,566億米ドルと予測しています。

・免疫チェックポイント阻害薬(ICI)市場の成長率は?

→DataM Intelligence社は免疫チェックポイント阻害薬(ICI)の世界市場が2024年~2031年に年平均16.5%成長すると予測しています。

・世界の免疫チェックポイント阻害薬(ICI)市場における主要企業は?

→DataM Intelligence社は「Bristol-Myers Squibb Company., Merck & Co., Inc., F. Hoffmann-La Roche Ltd, AstraZeneca, Regeneron Pharmaceuticals, Inc., Eli Lilly and Company, BeiGene LTD., GSK plc, Coherus BioSciences, Inc., and lncyte.など ...」をグローバル免疫チェックポイント阻害薬(ICI)市場の主要企業として認識しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、納品レポートの情報と少し異なる場合があります。