Japan Data Center Market Outlook (2025–2033): Digital Infrastructure at the Core of National Transformation

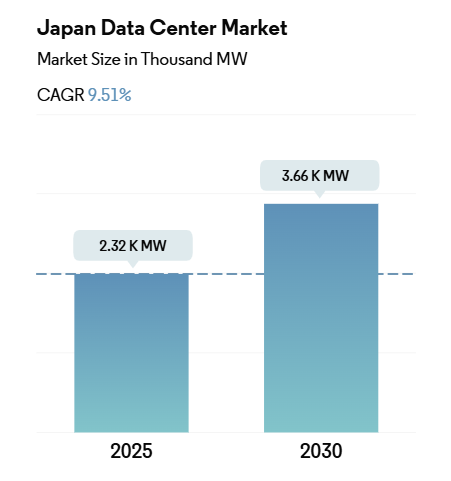

The Japan data center market is entering a new era of digital advancement and infrastructure expansion, driven by robust public and private sector investments, strategic policy initiatives, and a rapidly evolving digital economy. According to recent projections, the market’s total IT power capacity is expected to grow from 2.32 thousand MW in 2025 to 3.66 thousand MW by 2030, expanding at a CAGR of 9.51%. In parallel, colocation revenue is forecasted to double from USD 2.5 billion to nearly USD 5 billion, representing a CAGR of 14.68% during the forecast period.

This rapid market growth is underpinned by Japan’s commitment to creating a digitally integrated, decentralized, and sustainable society. The government’s Digital Garden City Nation initiative, backed by a JPY 5.7 trillion investment, is accelerating digital transformation across urban and rural regions, positioning data centers as a strategic cornerstone of Japan’s future economy.

Strategic Drivers of Market Growth

1. Government-Led Digital Transformation and Infrastructure Expansion

Japan’s forward-looking policies, including the Basic Act on Forming a Digital Society, reflect national ambitions to overhaul digital infrastructure. In 2023, the Ministry of Economy, Trade and Industry launched efforts to decentralize data centers, attracting interest from over 100 local governments to host new facilities. These initiatives are shaping a more regionally distributed data center ecosystem, with growing deployment in cooler areas to optimize energy usage via natural cooling.

2. Emphasis on Green and Sustainable Data Center Facilities

Sustainability is a central pillar of the market. Operators are increasingly investing in green data centers, with pioneers like NTT Corporation committing JPY 40 billion to renewable energy-powered facilities. Government tax incentives, such as the JPY 5 billion carbon neutrality subsidy, further stimulate green investments. These efforts align with Japan’s national goal of net-zero emissions by 2050, prompting data center operators to adopt energy-efficient cooling systems, renewable sourcing, and carbon-neutral operations.

3. Digitalization of Manufacturing and Enterprise Sectors

The manufacturing sector’s digital shift—marked by USD 890 million in digital infrastructure investments—is fueling demand for high-performance data center services. Applications such as private 5G networks, smart factory technologies, IoT deployments, and real-time analytics are amplifying the need for reliable, secure, and scalable data infrastructure.

4. Accelerated 5G Rollout and National Connectivity Goals

The expansion of 5G infrastructure, led by operators like NTT Docomo, KDDI, SoftBank, and Rakuten Mobile, is another significant growth catalyst. With an investment of over USD 14 billion in base stations and fiber optic networks, 5G is driving higher data consumption and distributed cloud computing, both of which are increasing data center capacity requirements. The Ministry of Internal Affairs and Communications is targeting 98% 5G coverage by 2024, further propelling data center demand in edge locations.

Emerging Market Trends and Dynamics

Rising Smartphone Usage and E-Commerce Integration

With 117 million smartphone users expected by 2029 and e-commerce becoming mainstream, Japan is witnessing a digital lifestyle boom. Businesses are rapidly adopting online platforms, mobile payments, and cloud-based services, generating massive data volumes and reinforcing the need for scalable storage and processing capabilities.

Growth of OTT Streaming and Digital Entertainment

The surge in streaming services, online gaming, and cloud-based content delivery is reshaping the data traffic landscape, compelling providers to develop high-capacity, low-latency data centers that can handle dynamic content loads while ensuring uninterrupted user experiences.

Subsea Cable Infrastructure and Decentralization Initiatives

Japan’s strategy to strengthen international bandwidth diversity involves extensive investments in subsea cable networks and data center decentralization, particularly off the western coastline. These moves aim to enhance data security, reduce latency, and stimulate regional economic revitalization by building over a dozen data centers in non-metropolitan zones by 2030.

Segmental Analysis: Data Center Size and Tier Classification

By Size:

-

Mega Data Centers (Dominant Segment, ~37%)

Mega facilities are pivotal in supporting hyperscale and enterprise workloads, with major operators like Digital Realty, AirTrunk, and IDC Frontier expanding capacities in Tokyo, Osaka, and Kyoto. Tax benefits and land incentives in strategic zones bolster their growth. -

Small Data Centers (Fastest-Growing Segment)

Despite smaller footprints, these facilities are witnessing a 13% growth CAGR, fueled by demand for edge computing and decentralized processing. Operators like Digital Edge and Telehouse are actively developing smaller-scale, high-efficiency hubs. -

Other Categories (Massive, Large, Medium)

These segments serve diverse industry verticals, offering flexible infrastructure between hyperscale and SME needs, often meeting Tier 3 compliance standards and regional computing requirements.

By Tier Type:

-

Tier 3 (Majority Market Share, ~79%)

The backbone of Japan’s data infrastructure, Tier 3 centers offer high redundancy, 99.98% uptime, and cost-effectiveness, attracting widespread enterprise adoption. New projects by Equinix, Vantage Data Centers, and NTT will expand this segment substantially. -

Tier 4 (High-Growth Segment, ~23% CAGR)

As critical industries demand maximum uptime and fault tolerance, Tier 4 facilities are gaining momentum. Mega Tier 4 centers are being planned for Tokyo, powered by innovations in cooling systems, power management, and security. -

Tier 1 & 2 (Niche Market Share)

Used for specific low-risk applications or in cost-sensitive sectors, these segments remain relatively underdeveloped, primarily in Okinawa, Nagoya, and smaller locations.

Absorption and Utilization Dynamics

-

Utilized Capacity (~78% Market Share)

Japan’s efficient capacity management reflects strong demand, driven by cloud migration, SaaS/PaaS adoption, and corporate digital initiatives. The segment is growing steadily, positioning Japan as a key North Asian data center hub. -

Non-Utilized Capacity

Though smaller in market share, this segment plays a strategic role in allowing operators to scale operations flexibly and accommodate sudden demand spikes. It also provides growth opportunities without immediate infrastructure outlays.

Competitive Landscape and Market Leaders

The Japan data center market is marked by a blend of global powerhouses and domestic giants, forming a synergistic and competitive ecosystem. Operators are investing in carrier-neutral, high-density, and energy-efficient infrastructure, focusing on compliance, automation, and sustainability.

Key Players:

-

Digital Realty Trust Inc.

-

Equinix Inc.

-

IDC Frontier Inc. (SoftBank Group)

-

NEC Corporation

-

NTT Ltd

These companies lead innovation in facility design, interconnect ecosystems, and value-added services, while forming strategic alliances to expand geographic footprints and enhance service offerings across segments (retail, wholesale, edge, hybrid cloud).

Future Growth Outlook and Strategic Recommendations

To succeed in this evolving market, operators must:

-

Accelerate green infrastructure investments

-

Expand edge and hyperscale capacity

-

Integrate AI, automation, and predictive analytics

-

Build robust interconnection platforms

-

Ensure compliance with cybersecurity, data sovereignty, and ESG standards

The next decade will be defined by flexibility, scalability, and sustainability. Companies capable of offering hybrid cloud, edge computing, and digital integration services will lead the future of Japan’s digital economy.

Table of Contents

-

Executive Summary & Key Findings

-

High-level insights and key data-driven takeaways.

-

-

Report Offers

-

Overview of data points, analysis scope, and deliverables.

-

-

Introduction

-

3.1 Study Assumptions & Market Definition

-

3.2 Scope of Study

-

3.3 Research Methodology

-

-

Market Outlook

-

Analysis of key metrics:

-

IT Load Capacity

-

Raised Floor Space

-

Colocation Revenue

-

Installed Racks

-

Rack Space Utilization

-

Submarine Cable Infrastructure

-

-

-

Key Industry Trends

-

Trends shaping the market:

-

Smartphone users & data traffic growth

-

Internet and mobile data speeds

-

Fiber connectivity expansion

-

Regulatory landscape

-

Value chain & distribution channel insights

-

-

-

Market Segmentation (Volume & Forecast to 2030)

-

By Location (Hotspot): Tokyo, Osaka, Rest of Japan

-

By Data Center Size: Small, Medium, Large, Massive, Mega

-

By Tier Type: Tier 1–2, Tier 3, Tier 4

-

By Absorption:

-

Utilized vs Non-utilized Capacity

-

By Colocation Type: Hyperscale, Retail, Wholesale

-

By End Users: BFSI, Cloud, E-Commerce, Government, Manufacturing, Media & Entertainment, Telecom, Others

-

-

-

Competitive Landscape

-

7.1 Market Share Overview

-

7.2 Company Landscape

-

7.3 Company Profiles (Detailed analysis of major players such as Equinix, Digital Realty, NTT, NEC, SoftBank IDC Frontier, etc.)

-

7.4 Full List of Companies Studied

-

-

Key Strategic Questions for Data Center CEOs

-

Critical business and investment questions for decision-makers.

-

-

Appendix

-

Global industry context:

-

Global Overview

-

Porter’s Five Forces Analysis

-

Value Chain Mapping

-

Market Drivers, Restraints, and Opportunities (DROs)

-

Sources, Tables, Figures, Glossary, and Data Pack

-

-