1 はじめに 24

1.1 調査目的 24

1.2 市場の定義 24

1.3 市場範囲 25

1.3.1 調査の対象範囲と対象外 25

1.3.2 考慮した年数 26

1.3.3 通貨 27

1.3.4 単位の検討 27

1.4 制限事項 27

1.5 利害関係者 27

1.6 変更点のまとめ 28

2 調査方法 29

2.1 調査データ 29

2.1.1 二次データ 30

2.1.1.1 二次資料からの主要データ 30

2.1.2 一次データ 31

2.1.2.1 一次資料からの主要データ 31

2.1.2.2 主要な一次参加者 31

2.1.2.3 一次インタビューの内訳 32

2.1.2.4 主要な業界インサイト 32

2.2 市場規模の推定 32

2.2.1 ボトムアップアプローチ 33

2.2.2 トップダウンアプローチ

2.3 基本数値の算出 34

2.3.1 アプローチ1:サプライサイド分析 34

2.3.2 アプローチ2:需要サイド分析 34

2.4 市場予測アプローチ 35

2.4.1 供給サイド 35

2.4.2 需要サイド

2.5 データの三角測量 36

2.6 要因分析 37

2.7 前提条件 37

2.8 制限とリスク 38

3 エグゼクティブ・サマリー 39

4 プレミアムインサイト 44

4.1 SIC繊維市場におけるプレーヤーにとっての魅力的な機会 44

4.2 SIC繊維市場:最終用途産業別、地域別(2023年) 45

4.3 SIC繊維の市場シェア、タイプ別、2023年 45

4.4 SIC繊維の市場シェア:形態別、2023年 46

4.5 Sic繊維の市場シェア:フェーズ別、2023年 46

4.6 Sic繊維の市場シェア:用途別、2023年 46

4.7 Sic繊維市場:国別 47

5 市場の概要 48

5.1 はじめに 48

5.2 市場ダイナミクス 48

5.2.1 推進要因 49

5.2.1.1 技術の進歩 49

5.2.1.2 LEAP エンジンの生産増加による生産能力拡大 49

5.2.1.3 低燃費航空機への需要の増加 49

5.2.1.4 陸上ガスタービンエンジン用SiC繊維ベースCMC製造への投資の増加 49

5.2.2 抑制要因 50

5.2.2.1 SiC 繊維の高コスト 50

5.2.2.2 代替品の入手可能性 50

5.2.3 機会 50

5.2.3.1 事故に強く軽量な原子炉製造のための研究開発の増加 50

5.2.3.2 SiC 繊維のコスト削減 50

5.2.3.3 中国勢の台頭 51

5.2.4 課題 51

5.2.4.1 低コストSiC繊維製造における技術的課題 51

5.2.4.2 流動性の逼迫 51

5.3 ポーターの5つの力分析 52

5.3.1 新規参入の脅威 52

5.3.2 代替品の脅威 53

5.3.3 供給者の交渉力 53

5.3.4 買い手の交渉力 53

5.3.5 競合の激しさ 53

5.4 主要ステークホルダーと購買基準 54

5.4.1 購買プロセスにおける主要ステークホルダー 54

5.4.2 購入基準

5.5 マクロ経済の見通し 55

5.5.1 導入 55

5.5.2 GDPの動向と予測 55

5.5.3 世界の航空宇宙・防衛産業の動向 57

5.5.4 エネルギー・電力産業の動向 58

5.5.5 世界の工業産業の動向 58

5.6 サプライチェーン分析 59

5.6.1 原材料分析 59

5.6.1.1 ポリカルボシラン 59

5.6.1.2 ポリチタンカルボシラン 59

5.6.2 タイプ分析 60

5.6.2.1 第一世代SiC繊維 60

5.6.2.2 第二世代SiC繊維 60

5.6.2.3 第3世代SiC繊維 60

5.6.3 相分析 60

5.6.4 最終製品分析 60

5.7 バリューチェーン分析 61

5.8 貿易分析 62

5.8.1 HSコード880330の輸入シナリオ 62

5.8.2 HSコード880330の輸出シナリオ 63

5.9 エコシステム 64

5.10 価格分析 66

5.10.1 主要プレーヤー別SIC材料の平均販売価格動向 66

5.10.2 SIC繊維のタイプ別平均販売価格動向 67

5.10.3 Sic繊維の平均販売価格動向(フェーズ別) 67

5.10.4 Sic繊維の形態別平均販売価格動向 68

5.10.5 Sic繊維の用途別平均販売価格動向 68

5.10.6 Sic繊維の平均販売価格動向(最終用途産業別) 69

5.10.7 Sic繊維の地域別平均販売価格動向 69

5.11 Sic繊維の地域別平均販売価格 70

5.12 技術分析 70

5.12.1 主要技術 70

5.12.1.1 化学気相成長法(CVD) 70

5.12.1.2 レーザー駆動型CVD(LCVD) 71

5.12.2 補足技術

5.12.2.1 連続インライン処理 71

5.13 特許分析 72

5.13.1 導入 72

5.13.2 方法論 72

5.13.3 文書タイプ 72

5.13.4 洞察 73

5.13.5 法的地位 74

5.13.6 管轄区域分析 74

5.13.7 上位出願人 75

5.13.8 過去5年間の特許権者トップ10(米国) 77

5.14 規制の状況 78

5.14.1 規制機関、政府機関、その他の組織 78

5.15 主要な会議とイベント 80

5.16 ケーススタディ分析 82

5.16.1 ケーススタディ1:寧波中興による第2世代SiC繊維の導入

寧波中興新材料有限公司による第2世代SIC繊維の導入。 82

5.16.2 ケーススタディ 2: Nasa’s Glenn Research Center による炭化ケイ素繊維トウの開発 83

5.16.3 ケーススタディ3:炭化ケイ素繊維の国内生産のための連続スケーラブル・プロセス 83

5.17 顧客ビジネスに影響を与えるトレンド/混乱 84

5.18 投資と資金調達のシナリオ 85

5.19 AIがシリコン繊維市場に与える影響 86

5.19.1 主要な使用事例と市場の可能性 86

5.19.2 SIC繊維市場におけるAIの導入事例 86

5.19.3 シック・ファイバー市場における顧客のAI導入準備 86

6 SIC繊維市場:タイプ別 87

6.1 導入 88

6.2 第1世代SIC繊維 90

6.2.1 低コストが採用を促進 90

6.3 第2世代Sic繊維 92

6.3.1 航空宇宙産業からの需要増加が市場を牽引 92

6.4 第3世代Sic繊維 94

6.4.1 第三世代Sic繊維の生産増加が市場を牽引 94

7 Sic繊維市場、フェーズ別 96

7.1 導入 97

7.2 非晶質 98

7.2.1 高温用途での使用が市場を牽引 98

7.3 結晶性 100

7.3.1 他の繊維よりも優れた性能が市場を牽引 100

8 シック繊維市場、形態別 103

8.1 導入 104

8.2 連続繊維 105

8.2.1 航空宇宙・防衛産業におけるSIC繊維の用途拡大が市場を牽引 105

8.3 織物 107

8.3.1 主要メーカーによる織物繊維の自社加工が市場を牽引 107

8.4 その他の形態 109

9 シック繊維市場:用途別 111

9.1 導入 112

9.2 複合材料 113

9.2.1 研究開発活動の活発化が市場を牽引 113

9.3 非コンポジット 116

9.3.1 非複合用途での使用の増加が市場を牽引 116

10 シック繊維市場:最終用途産業別 118

10.1 導入 119

10.2 航空宇宙・防衛 121

10.2.1 航空機エンジンメーカーからの高い需要が市場を牽引 121

10.3 エネルギー・電力 123

10.3.1 市場成長を支える研究開発投資の増加 123

10.4 産業用 125

10.4.1 シック・ファイバーの幅広い産業用途が市場を牽引 125

10.5 その他の最終用途産業 126

11 シック繊維市場(地域別) 128

11.1 はじめに 129

11.2 北米 132

11.2.1 米国 138

11.2.1.1 主要メーカーの存在が市場を牽引 138

11.2.2 カナダ 139

11.2.2.1 航空宇宙・防衛産業への投資拡大が市場を牽引 139

11.3 欧州 141

11.3.1 フランス 147

11.3.1.1 主要航空機メーカーの存在が市場を押し上げる 147

11.3.2 ドイツ 149

11.3.2.1 SiC繊維のエコシステムにおけるプレーヤー間の戦略的提携が市場を促進 149

11.3.3 イギリス 150

11.3.3.1 航空宇宙・防衛産業の研究開発投資の増加が市場を牽引 150

11.3.4 イタリア 152

11.3.4.1 航空機メーカーの需要増加が市場を牽引 152

11.3.5 スペイン 153

11.3.5.1 急速に拡大する航空宇宙・防衛産業が市場を牽引 153

11.3.6 その他のヨーロッパ 155

11.4 アジア太平洋地域 157

11.4.1 日本 163

11.4.1.1 主要企業間のパートナーシップ拡大が市場を牽引 163

11.4.2 中国 165

11.4.2.1 COMACのフットプリントの拡大が市場を牽引 165

11.4.3 韓国 166

11.4.3.1 成長する国防予算がSiC繊維の機会を創出 166

11.4.4 その他のアジア太平洋地域 168

11.5 ラテンアメリカ 170

11.5.1 ブラジル 175

11.5.1.1 LEAPエンジン向けSiC繊維の高い需要が市場を牽引 175

11.5.2 メキシコ 177

11.5.2.1 航空宇宙・防衛産業の成長が市場を牽引 177

11.5.3 その他のラテンアメリカ 178

11.6 中東・アフリカ 180

11.6.1 イスラエル 186

11.6.1.1 防衛予算の増加が市場を牽引 186

11.6.2 GCC諸国 188

11.6.2.1 アラブ首長国連邦 188

11.6.2.1.1 ボーイングへの先端複合材の供給が市場を牽引 188

11.6.2.2 サウジアラビア 189

11.6.2.2.1 航空宇宙用複合材料の製造に注力する動きが市場を牽引 189

11.6.2.3 その他のGCC諸国 191

11.6.3 その他の中東・アフリカ 193

12 競争環境 195

12.1 概要 195

12.2 主要プレーヤーの戦略/勝利への権利 195

12.3 収益分析 196

12.4 市場シェア分析 197

12.5 ブランド/製品の比較 199

12.5.1 ブランド/製品の比較(シックファイバー製品別) 199

12.6 企業評価マトリックス:主要企業(2023年) 201

12.6.1 スター企業 201

12.6.2 新興リーダー 201

12.6.3 浸透型プレーヤー 201

12.6.4 参加企業 201

12.6.5 企業フットプリント:主要プレーヤー、2023年 203

12.6.5.1 企業フットプリント 203

12.6.5.2 タイプ別フットプリント 204

12.6.5.3 フェーズ別フットプリント 205

12.6.5.4 形状フットプリント 205

12.6.5.5 用途フットプリント 206

12.6.5.6 最終用途産業フットプリント 207

12.6.5.7 地域別フットプリント 208

12.7 企業評価と財務指標 209

12.7.1 企業評価 209

12.7.2 財務指標 209

12.8 競争シナリオ 210

12.8.1 取引 210

12.8.2 拡張 210

13 会社プロファイル 211

13.1 主要プレーヤー 211

NGS Advanced Fibers Co.Ltd. (Japan)

UBE Corporation (Japan)

COI Ceramics Inc. (US)

Specialty Materials Inc. (US)

MATECH (US)

Suzhou Saifei Group Ltd. (China)

Haydale Technologies Inc. (US)

GE Aerospace (US)

Ningbo Zhongxing New Materials Co.Ltd. (China)

and BJS Ceramics (Germany)

14 付録 240

14.1 ディスカッションガイド 240

14.2 Knowledgestore: マーケットサ ンドマーケッツの購読ポータル 243

14.3 カスタマイズオプション 245

14.4 関連レポート 245

14.5 著者の詳細 246

Third generation fiber's performance in ultra-high-temperature environments and their ability to withstand structural integrity over such long time intervals make them particularly useful for application in next-generation turbine engines including in LEAP engines and advanced power generation systems.

"In terms of value, continuous form of SiC fibers accounted for the largest share of the overall SiC fibers market."

In 2023, continuous SiC fibers in SiC fibers market have the largest market share due to their ability to be easily integrated into advanced composite structures making them the choice for next-generation engine systems. For example, in LEAP engines, they play a very visible role. Continuous SiC fibers are becoming increasingly in demand as industries work towards getting closer and closer to lighter, stronger, and fuel-efficient materials. Thus, as the end-use industries seek advanced materials there is an expected increase in demand for continuous SiC fibers.

"In terms of value, the crystalline SiC fibers are projected to be the fastest growing phase of SiC fibers."

Crystalline SiC fibers are projected to be the fastest-growing in phase segment in SiC fibers market, due to its advantages over other fibers. Oxide fibers, superalloys, and amorphous SiC fibers degrade very quickly at elevated temperatures. However, Sylramic SiC fibers which are a type of crystalline SiC fiber retain strength and stiffness to very high-temperature levels, above 1400°C (2252°F) due to the particular chemical composition, structure, and low oxygen content. It offers superior creep resistance along with thermal stability and is highly suitable for high-performance applications in aerospace, defense, and energy. Advances have been achieved in SiC fibers not only for breaking through functional barriers but also in response to increased demands for high-temperature-resistant materials in various sectors.

"In terms of value, the usage of SiC fibers in composites is projected to be the fastest in the forecast period."

The fastest-growing usage of SiC fibers in composites is based on tremendous progress in material properties and the ability to withstand extreme conditions. NASA's research, especially at Glenn Research Center, has played an important role in propelling increased demand for SiC fibers in ceramic matrix composites for high-temperature structural applications beyond 2700°F. High-strength SiC fibers patented as "Sylramic-iBN" and "Super Sylramic-iBN" are specially processed to provide high mechanical and environmental properties. Protective boron-nitride coatings and advanced CVI techniques have transformed the CMCs made of SiC/SiC from NASA into products that are much more resistant and quite highly resistant to extreme heat and stress, but still allow for customization under specific design and performance requirements. Thus, these developments have been very much driving the adoption of SiC composites for high-performance industries.

“During the forecast period, the SiC fiber market in aerospace & defense is projected to be the fastest growing end-use industry.”

During the forecast period from 2024 to 2029, the aerospace & defense industry is expected to be the fastest-growing end-use industry in the SiC fibers market. The SiC fibers are unmatched in their performances in high temperature as well as high-stress applications, such as advanced aircraft and space vehicle engines. These fibers can resist up to 2,732°F and thus are well suited for use in next-generation aerospace engines, such as the GE9X installed in the Boeing 777X, or advanced military engines such as the GE3000 for the US Army's ITEP program. Although the market faces disruptions in terms of reductions in aircraft delivery and more issues on the supply chain, high-performance material demand within both the components of the engine and aerospace technology development is a factor pushing the growth of SiC fiber usage in the aerospace & defense sector at a very rapid pace.

“During the forecast period, the SiC fibers market in North America region is projected to be the largest region.”

North America is the largest market for SiC fibers because of its strong aerospace, defense, and energy sectors, which are a driver for the demand for high-performance materials such as SiC fibers. The region is dominated by large aerospace manufacturers, Boeing, Lockheed Martin, and General Electric, which have comprehensive use of SiC fibers in critical engine components in commercial and military applications. It also continues to invest in space exploration and defense projects led by the NASA and U.S. Department of Defense; this investment promotes increased demand for SiC-based CMCs in rockets, space vehicles, and advanced military engine components. Second, North America has a strong research infrastructure led by institutions and private companies that develop SiC fiber technology, which creates innovation and potentially expands its market shares.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

• By Company Type- Tier 1- 55%, Tier 2- 25%, and Tier 3- 20%

• By Designation- C Level- 50%, Director Level- 30%, and Others- 20%

• By Region- North America- 15%, Europe- 15%, Asia Pacific- 65%, Middle East & Africa (MEA)-2%, Latin America- 3%.

The report provides a comprehensive analysis of company profiles:

Prominent companies NGS Advanced Fibers Co., Ltd. (Japan), UBE Corporation (Japan), COI Ceramics, Inc. (US), Specialty Materials, Inc. (US), MATECH (US), Suzhou Saifei Group Ltd. (China), Haydale Technologies Inc. (US), GE Aerospace (US), Ningbo Zhongxing New Materials Co., Ltd. (China), and BJS Ceramics (Germany).

Research Coverage

This research report categorizes the SiC Fibers market By Type (First Generation, Second Generation, Third Generation), By Form (Continuous, Woven, Others), By Phase (Amorphous, Crystalline), By Usage ( Composites, Non-composites), End-Use Industry (Aerospace & Defense, Energy & Power, Industrial, and Other End-Use Industries), Region (North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America). The scope of the report includes detailed information about the major factors influencing the growth of the SiC Fibers market, such as drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted in order to provide insights into their business overview, solutions, and services, key strategies, contracts, partnerships, and agreements. Product launches, mergers and acquisitions, and recent developments in the SiC Fibers market are all covered. This report includes a competitive analysis of upcoming startups in the SiC Fibers market ecosystem.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall SiC Fibers market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

• Analysis of key drivers (Rising demand from LEAP engines), restraints (High cost of SiC fibers, availability of substitutes), opportunities (Reduction in SiC fibers cost, Emergence of Chinese players), and challenges (Liquidity crunch, technological challenges in manufacturing of low-cost SiC fibers) influencing the growth of the SiC Fibers market

• Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and service launches in the SiC Fibers market.

• Market Development: Comprehensive information about lucrative markets – the report analyses the SiC Fibers market across varied regions.

• Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the SiC Fibers market

• Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like NGS Advanced Fibers Co., Ltd. (Japan), UBE Corporation (Japan), COI Ceramics, Inc. (US), Specialty Materials, Inc. (US), MATECH (US), Suzhou Saifei Group Ltd. (China), Haydale Technologies Inc. (US), GE Aerospace (US), Ningbo Zhongxing New Materials Co., Ltd. (China), BJS Ceramics (Germany), Nanoshel LLC (US), Skyspring Nanomaterials, Inc. (US), TISICS LTD. (UK), National Aeronautics and Space Administration (US), the Institute of Energy Science & Technology (Japan), National University of Defense Technology (China), Free Form Fibers (US), among others in the SiC Fibers market.

1 INTRODUCTION 24

1.1 STUDY OBJECTIVES 24

1.2 MARKET DEFINITION 24

1.3 MARKET SCOPE 25

1.3.1 INCLUSIONS & EXCLUSIONS OF STUDY 25

1.3.2 YEARS CONSIDERED 26

1.3.3 CURRENCY 27

1.3.4 UNIT CONSIDERED 27

1.4 LIMITATIONS 27

1.5 STAKEHOLDERS 27

1.6 SUMMARY OF CHANGES 28

2 RESEARCH METHODOLOGY 29

2.1 RESEARCH DATA 29

2.1.1 SECONDARY DATA 30

2.1.1.1 Key data from secondary sources 30

2.1.2 PRIMARY DATA 31

2.1.2.1 Key data from primary sources 31

2.1.2.2 Key primary participants 31

2.1.2.3 Breakdown of primary interviews 32

2.1.2.4 Key industry insights 32

2.2 MARKET SIZE ESTIMATION 32

2.2.1 BOTTOM-UP APPROACH 33

2.2.2 TOP-DOWN APPROACH 33

2.3 BASE NUMBER CALCULATION 34

2.3.1 APPROACH 1: SUPPLY-SIDE ANALYSIS 34

2.3.2 APPROACH 2: DEMAND-SIDE ANALYSIS 34

2.4 MARKET FORECAST APPROACH 35

2.4.1 SUPPLY SIDE 35

2.4.2 DEMAND SIDE 35

2.5 DATA TRIANGULATION 36

2.6 FACTOR ANALYSIS 37

2.7 ASSUMPTIONS 37

2.8 LIMITATIONS & RISKS 38

3 EXECUTIVE SUMMARY 39

4 PREMIUM INSIGHTS 44

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SIC FIBERS MARKET 44

4.2 SIC FIBERS MARKET, BY END-USE INDUSTRY AND REGION, 2023 45

4.3 SIC FIBERS MARKET SHARE, BY TYPE, 2023 45

4.4 SIC FIBERS MARKET SHARE, BY FORM, 2023 46

4.5 SIC FIBERS MARKET SHARE, BY PHASE, 2023 46

4.6 SIC FIBERS MARKET SHARE, BY USAGE, 2023 46

4.7 SIC FIBERS MARKET, BY COUNTRY 47

5 MARKET OVERVIEW 48

5.1 INTRODUCTION 48

5.2 MARKET DYNAMICS 48

5.2.1 DRIVERS 49

5.2.1.1 Technological advancements 49

5.2.1.2 Capacity expansion due to rising production of LEAP engines 49

5.2.1.3 Increasing demand for fuel-efficient aircraft 49

5.2.1.4 Increased investments in manufacturing SiC fiber-based CMCs for land-based gas turbine engines 49

5.2.2 RESTRAINTS 50

5.2.2.1 High cost of SiC fibers 50

5.2.2.2 Availability of substitutes 50

5.2.3 OPPORTUNITIES 50

5.2.3.1 Increasing R&D for manufacturing accident-tolerant and lightweight nuclear reactors 50

5.2.3.2 Reduction in SiC fiber costs 50

5.2.3.3 Emergence of Chinese players 51

5.2.4 CHALLENGES 51

5.2.4.1 Technological challenges in manufacturing low-cost SiC fibers 51

5.2.4.2 Liquidity crunch 51

5.3 PORTER’S FIVE FORCES ANALYSIS 52

5.3.1 THREAT OF NEW ENTRANTS 52

5.3.2 THREAT OF SUBSTITUTES 53

5.3.3 BARGAINING POWER OF SUPPLIERS 53

5.3.4 BARGAINING POWER OF BUYERS 53

5.3.5 INTENSITY OF COMPETITIVE RIVALRY 53

5.4 KEY STAKEHOLDERS AND BUYING CRITERIA 54

5.4.1 KEY STAKEHOLDERS IN BUYING PROCESS 54

5.4.2 BUYING CRITERIA 55

5.5 MACROECONOMIC OUTLOOK 55

5.5.1 INTRODUCTION 55

5.5.2 GDP TRENDS AND FORECAST 55

5.5.3 TRENDS IN GLOBAL AEROSPACE & DEFENSE INDUSTRY 57

5.5.4 TRENDS IN ENERGY & POWER INDUSTRY 58

5.5.5 TRENDS IN GLOBAL INDUSTRIAL INDUSTRY 58

5.6 SUPPLY CHAIN ANALYSIS 59

5.6.1 RAW MATERIAL ANALYSIS 59

5.6.1.1 Polycarbosilane 59

5.6.1.2 Polytitaniumcarbosilane 59

5.6.2 TYPE ANALYSIS 60

5.6.2.1 First-generation SiC fibers 60

5.6.2.2 Second-generation SiC fibers 60

5.6.2.3 Third-generation SiC fibers 60

5.6.3 PHASE ANALYSIS 60

5.6.4 FINAL PRODUCT ANALYSIS 60

5.7 VALUE CHAIN ANALYSIS 61

5.8 TRADE ANALYSIS 62

5.8.1 IMPORT SCENARIO FOR HS CODE 880330 62

5.8.2 EXPORT SCENARIO FOR HS CODE 880330 63

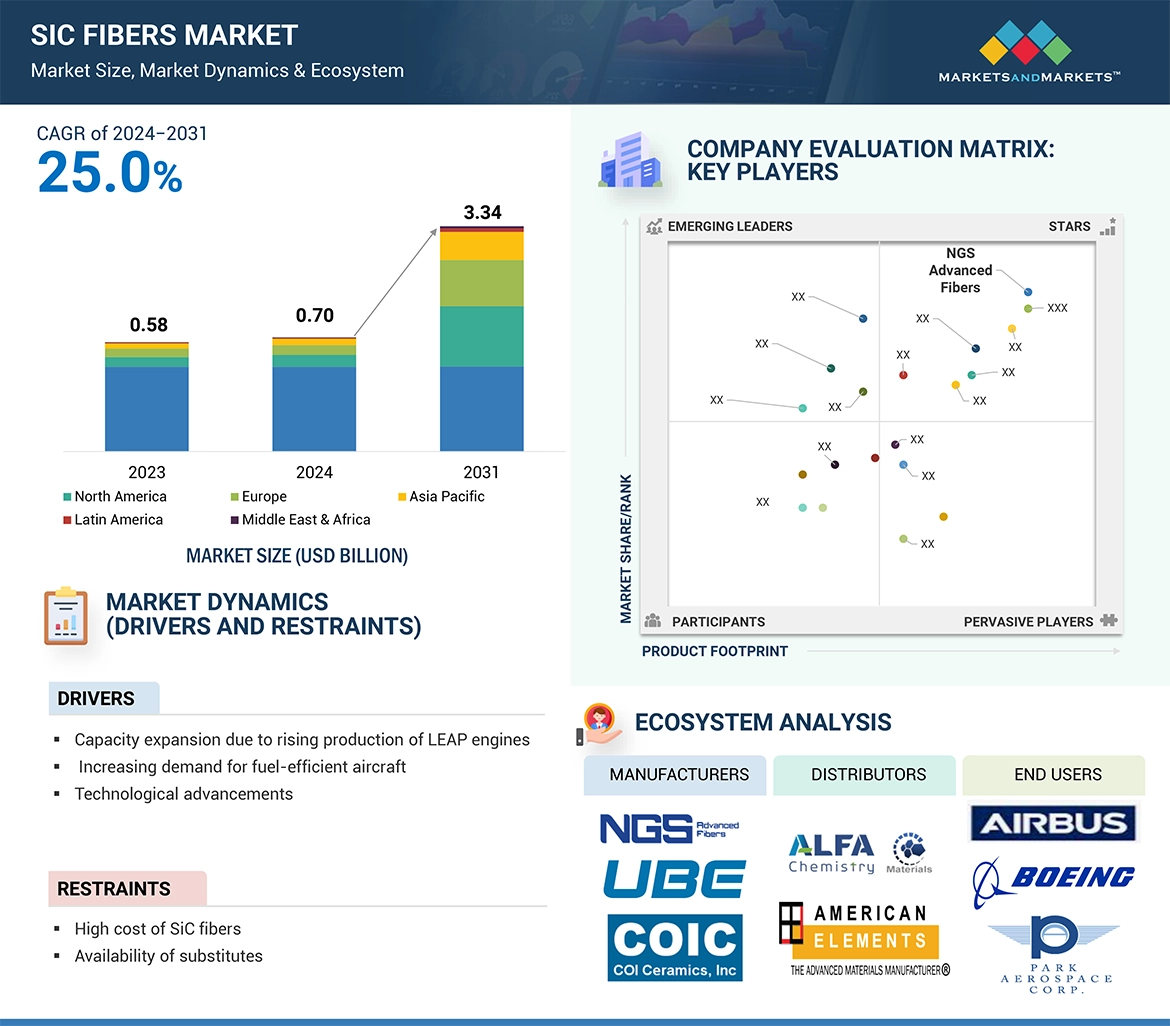

5.9 ECOSYSTEM 64

5.10 PRICING ANALYSIS 66

5.10.1 AVERAGE SELLING PRICE TREND OF SIC MATERIALS, BY KEY PLAYER 66

5.10.2 AVERAGE SELLING PRICE TREND OF SIC FIBERS, BY TYPE 67

5.10.3 AVERAGE SELLING PRICE TREND OF SIC FIBERS, BY PHASE 67

5.10.4 AVERAGE SELLING PRICE TREND OF SIC FIBERS, BY FORM 68

5.10.5 AVERAGE SELLING PRICE TREND OF SIC FIBERS, BY USAGE 68

5.10.6 AVERAGE SELLING PRICE TREND OF SIC FIBERS, BY END-USE INDUSTRY 69

5.10.7 AVERAGE SELLING PRICE TREND OF SIC FIBERS, BY REGION 69

5.11 AVERAGE SELLING PRICE OF SIC FIBERS, BY REGION 70

5.12 TECHNOLOGY ANALYSIS 70

5.12.1 KEY TECHNOLOGIES 70

5.12.1.1 Chemical Vapor Deposition (CVD) 70

5.12.1.2 Laser-driven CVD (LCVD) 71

5.12.2 COMPLEMENTARY TECHNOLOGIES 71

5.12.2.1 Continuous In-line Processing 71

5.13 PATENT ANALYSIS 72

5.13.1 INTRODUCTION 72

5.13.2 METHODOLOGY 72

5.13.3 DOCUMENT TYPES 72

5.13.4 INSIGHTS 73

5.13.5 LEGAL STATUS 74

5.13.6 JURISDICTION ANALYSIS 74

5.13.7 TOP APPLICANTS 75

5.13.8 TOP 10 PATENT OWNERS (US) IN LAST 5 YEARS 77

5.14 REGULATORY LANDSCAPE 78

5.14.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS 78

5.15 KEY CONFERENCES & EVENTS 80

5.16 CASE STUDY ANALYSIS 82

5.16.1 CASE STUDY 1: INTRODUCTION OF SECOND-GENERATION SIC FIBER

BY NINGBO ZHONGXING NEW MATERIALS CO., LTD. 82

5.16.2 CASE STUDY 2: DEVELOPMENT OF SILICON CARBIDE FIBER TOWS BY NASA’S GLENN RESEARCH CENTER 83

5.16.3 CASE STUDY 3: CONTINUOUS SCALABLE PROCESS FOR DOMESTIC PRODUCTION OF SILICON CARBIDE FIBERS 83

5.17 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS 84

5.18 INVESTMENT AND FUNDING SCENARIO 85

5.19 IMPACT OF AI ON SIC FIBERS MARKET 86

5.19.1 TOP USE CASES AND MARKET POTENTIAL 86

5.19.2 CASE STUDIES OF AI IMPLEMENTATION IN SIC FIBERS MARKET 86

5.19.3 CLIENTS' READINESS TO ADOPT AI IN SIC FIBERS MARKET 86

6 SIC FIBERS MARKET, BY TYPE 87

6.1 INTRODUCTION 88

6.2 FIRST-GENERATION SIC FIBERS 90

6.2.1 LOW COST TO DRIVE ADOPTION 90

6.3 SECOND-GENERATION SIC FIBERS 92

6.3.1 GROWING DEMAND FROM AEROSPACE INDUSTRY TO DRIVE MARKET 92

6.4 THIRD-GENERATION SIC FIBERS 94

6.4.1 GROWING PRODUCTION OF THIRD-GENERATION SIC FIBERS TO DRIVE MARKET 94

7 SIC FIBERS MARKET, BY PHASE 96

7.1 INTRODUCTION 97

7.2 AMORPHOUS 98

7.2.1 USE IN HIGH-TEMPERATURE APPLICATIONS TO DRIVE MARKET 98

7.3 CRYSTALLINE 100

7.3.1 SUPERIOR PERFORMANCE OVER OTHER FIBERS TO DRIVE MARKET 100

8 SIC FIBERS MARKET, BY FORM 103

8.1 INTRODUCTION 104

8.2 CONTINUOUS 105

8.2.1 INCREASED APPLICATION OF SIC FIBERS IN AEROSPACE & DEFENSE INDUSTRY TO DRIVE MARKET 105

8.3 WOVEN 107

8.3.1 IN-HOUSE WOVEN FIBER PROCESSING BY MAJOR MANUFACTURERS TO DRIVE MARKET 107

8.4 OTHER FORMS 109

9 SIC FIBERS MARKET, BY USAGE 111

9.1 INTRODUCTION 112

9.2 COMPOSITE 113

9.2.1 INCREASED R&D ACTIVITIES TO PROPEL MARKET 113

9.3 NON-COMPOSITE 116

9.3.1 INCREASED USE IN NON-COMPOSITE APPLICATIONS TO DRIVE MARKET 116

10 SIC FIBERS MARKET, BY END-USE INDUSTRY 118

10.1 INTRODUCTION 119

10.2 AEROSPACE & DEFENSE 121

10.2.1 HIGH DEMAND FROM AIRCRAFT ENGINE MANUFACTURERS TO DRIVE MARKET 121

10.3 ENERGY & POWER 123

10.3.1 GROWING INVESTMENTS IN R&D TO SUPPORT MARKET GROWTH 123

10.4 INDUSTRIAL 125

10.4.1 WIDE INDUSTRIAL APPLICATION OF SIC FIBERS TO DRIVE MARKET 125

10.5 OTHER END-USE INDUSTRIES 126

11 SIC FIBERS MARKET, BY REGION 128

11.1 INTRODUCTION 129

11.2 NORTH AMERICA 132

11.2.1 US 138

11.2.1.1 Presence of key manufacturers to drive market 138

11.2.2 CANADA 139

11.2.2.1 Growing investments in aerospace & defense industry to propel market 139

11.3 EUROPE 141

11.3.1 FRANCE 147

11.3.1.1 Presence of key aircraft manufacturers to boost market 147

11.3.2 GERMANY 149

11.3.2.1 Strategic partnerships between players in SiC fiber ecosystem to propel market 149

11.3.3 UK 150

11.3.3.1 Increased investments in R&D of aerospace & defense industry to drive market 150

11.3.4 ITALY 152

11.3.4.1 Growing demand from aircraft manufacturers to drive market 152

11.3.5 SPAIN 153

11.3.5.1 Rapidly expanding aerospace & defense industries to drive market 153

11.3.6 REST OF EUROPE 155

11.4 ASIA PACIFIC 157

11.4.1 JAPAN 163

11.4.1.1 Growing partnerships among key players to drive market 163

11.4.2 CHINA 165

11.4.2.1 Growing footprint of COMAC to drive market 165

11.4.3 SOUTH KOREA 166

11.4.3.1 Growing defense budget to create opportunities for SiC fibers 166

11.4.4 REST OF ASIA PACIFIC 168

11.5 LATIN AMERICA 170

11.5.1 BRAZIL 175

11.5.1.1 High demand for SiC fibers for LEAP engines to drive market 175

11.5.2 MEXICO 177

11.5.2.1 Growing aerospace & defense industry to drive market 177

11.5.3 REST OF LATIN AMERICA 178

11.6 MIDDLE EAST & AFRICA 180

11.6.1 ISRAEL 186

11.6.1.1 Growing defense budget to drive market 186

11.6.2 GCC COUNTRIES 188

11.6.2.1 UAE 188

11.6.2.1.1 Supply of advanced composites to Boeing to drive market 188

11.6.2.2 Saudi Arabia 189

11.6.2.2.1 Growing focus on manufacturing aerospace composites to drive market 189

11.6.2.3 Rest of GCC Countries 191

11.6.3 REST OF MIDDLE EAST & AFRICA 193

12 COMPETITIVE LANDSCAPE 195

12.1 OVERVIEW 195

12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN 195

12.3 REVENUE ANALYSIS 196

12.4 MARKET SHARE ANALYSIS 197

12.5 BRAND/PRODUCT COMPARISON 199

12.5.1 BRAND/PRODUCT COMPARISON, BY SIC FIBER PRODUCT 199

12.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023 201

12.6.1 STARS 201

12.6.2 EMERGING LEADERS 201

12.6.3 PERVASIVE PLAYERS 201

12.6.4 PARTICIPANTS 201

12.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023 203

12.6.5.1 Company footprint 203

12.6.5.2 Type footprint 204

12.6.5.3 Phase footprint 205

12.6.5.4 Form footprint 205

12.6.5.5 Usage footprint 206

12.6.5.6 End-use industry footprint 207

12.6.5.7 Region footprint 208

12.7 COMPANY VALUATION AND FINANCIAL METRICS 209

12.7.1 COMPANY VALUATION 209

12.7.2 FINANCIAL METRICS 209

12.8 COMPETITIVE SCENARIO 210

12.8.1 DEALS 210

12.8.2 EXPANSIONS 210

13 COMPANY PROFILES 211

13.1 KEY PLAYERS 211

13.1.1 NGS ADVANCED FIBERS CO., LTD. 211

13.1.1.1 Business overview 211

13.1.1.2 Products offered 211

13.1.1.3 MnM view 211

13.1.1.3.1 Key strengths 211

13.1.1.3.2 Strategic choices 212

13.1.1.3.3 Weaknesses and competitive threats 212

13.1.2 UBE CORPORATION 213

13.1.2.1 Business overview 213

13.1.2.2 Products offered 214

13.1.2.3 MnM view 215

13.1.2.3.1 Key strengths 215

13.1.2.3.2 Strategic choices 215

13.1.2.3.3 Weaknesses and competitive threats 215

13.1.3 COI CERAMICS, INC. 216

13.1.3.1 Business overview 216

13.1.3.2 Products offered 216

13.1.3.3 Recent developments 217

13.1.3.3.1 Deals 217

13.1.3.4 MnM view 217

13.1.3.4.1 Key strengths 217

13.1.3.4.2 Strategic choices 217

13.1.3.4.3 Weaknesses and competitive threats 217

13.1.4 GE AEROSPACE 218

13.1.4.1 Business overview 218

13.1.4.2 Products offered 219

13.1.4.3 Recent developments 220

13.1.4.3.1 Deals 220

13.1.4.4 MnM view 220

13.1.4.4.1 Key strengths 220

13.1.4.4.2 Strategic choices 220

13.1.4.4.3 Weaknesses and competitive threats 220

13.1.5 SPECIALTY MATERIALS, INC. 221

13.1.5.1 Business overview 221

13.1.5.2 Products offered 221

13.1.5.3 Recent developments 221

13.1.5.3.1 Deals 221

13.1.5.4 MnM view 222

13.1.5.4.1 Key strengths 222

13.1.5.4.2 Strategic choices 222

13.1.5.4.3 Weaknesses and competitive threats 222

13.1.6 HAYDALE GRAPHENE INDUSTRIES PLC 223

13.1.6.1 Business overview 223

13.1.6.2 Products offered 224

13.1.6.3 MnM view 224

13.1.6.3.1 Key strengths 224

13.1.6.3.2 Strategic choices 224

13.1.6.3.3 Weaknesses and competitive threats 224

13.1.7 MATECH 225

13.1.7.1 Business overview 225

13.1.7.2 Products offered 225

13.1.7.3 MnM view 226

13.1.7.3.1 Key strengths 226

13.1.7.3.2 Strategic choices 226

13.1.7.3.3 Weaknesses and competitive threats 226

13.1.8 SUZHOU SAIFEI GROUP LTD. 227

13.1.8.1 Business overview 227

13.1.8.2 Products offered 227

13.1.8.3 MnM view 227

13.1.8.3.1 Key strengths 227

13.1.8.3.2 Strategic choices 227

13.1.8.3.3 Weaknesses and competitive threats 228

13.1.9 BJS CERAMICS 229

13.1.9.1 Business overview 229

13.1.9.2 Products offered 229

13.1.9.3 Recent developments 229

13.1.9.3.1 Expansions 229

13.1.9.4 MnM view 230

13.1.9.4.1 Key strengths 230

13.1.9.4.2 Strategic choices 230

13.1.9.4.3 Weaknesses and competitive threats 230

13.1.10 NINGBO ZHONGXING NEW MATERIALS CO., LTD. 231

13.1.10.1 Business overview 231

13.1.10.2 Products offered 231

13.1.10.3 MnM view 231

13.1.10.3.1 Key strengths 231

13.1.10.3.2 Strategic choices 231

13.1.10.3.3 Weaknesses and competitive threats 232

13.1.11 NANOSHEL LLC 233

13.1.11.1 Business overview 233

13.1.11.2 Products offered 233

13.1.11.3 MnM view 233

13.1.11.3.1 Key strengths 233

13.1.11.3.2 Strategic choices 234

13.1.11.3.3 Weaknesses and competitive threats 234

13.1.12 SKYSPRING NANOMATERIALS, INC. 235

13.1.12.1 Business overview 235

13.1.12.2 Products offered 235

13.1.12.3 MnM view 235

13.1.12.3.1 Key strengths 235

13.1.12.3.2 Strategic choices 235

13.1.12.3.3 Weaknesses and competitive threats 236

13.2 OTHER PLAYERS 237

13.2.1 NATIONAL AERONAUTICS AND SPACE ADMINISTRATION 237

13.2.2 TISICS LTD. 237

13.2.3 INSTITUTE OF ENERGY SCIENCE AND TECHNOLOGY 238

13.2.4 NATIONAL UNIVERSITY OF DEFENSE TECHNOLOGY 238

13.2.5 FREE FORM FIBERS 239

14 APPENDIX 240

14.1 DISCUSSION GUIDE 240

14.2 KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL 243

14.3 CUSTOMIZATION OPTIONS 245

14.4 RELATED REPORTS 245

14.5 AUTHOR DETAILS 246

❖ 世界のSiC繊維市場に関するよくある質問(FAQ) ❖

・SiC繊維の世界市場規模は?

→MarketsandMarkets社は2024年のSiC繊維の世界市場規模を0.7億米ドルと推定しています。

・SiC繊維の世界市場予測は?

→MarketsandMarkets社は2031年のSiC繊維の世界市場規模を33.4億米ドルと予測しています。

・SiC繊維市場の成長率は?

→MarketsandMarkets社はSiC繊維の世界市場が2024年~2031年に年平均25.0%成長すると予測しています。

・世界のSiC繊維市場における主要企業は?

→MarketsandMarkets社は「NGS Advanced Fibers Co., Ltd. (Japan), UBE Corporation (Japan), COI Ceramics, Inc. (US), Specialty Materials, Inc. (US), MATECH (US), Suzhou Saifei Group Ltd. (China), Haydale Technologies Inc. (US), GE Aerospace (US), Ningbo Zhongxing New Materials Co., Ltd. (China), and BJS Ceramics (Germany)など ...」をグローバルSiC繊維市場の主要企業として認識しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、納品レポートの情報と少し異なる場合があります。