1 はじめに 29

1.1 調査目的 29

1.1.1 市場の定義 29

1.2 市場スコープ 30

1.2.1 市場セグメンテーション 30

1.2.2 含まれるものと除外されるもの 31

1.3 考慮した年数 31

1.4 考慮した単位 32

1.4.1 通貨/価値単位 32

1.4.2 数量の考慮 33

1.5 利害関係者 33

1.6 変更点のまとめ 34

2 調査方法 35

2.1 調査データ 35

2.1.1 二次データ 36

2.1.1.1 二次資料からの主要データ 36

2.1.2 一次データ 37

2.1.2.1 一次ソースからの主要データ 37

2.1.2.2 主要な業界インサイト 38

2.1.2.3 一次データの内訳 38

2.2 市場規模の推定 39

2.2.1 ボトムアップアプローチ 39

2.2.2 トップダウンアプローチ 40

2.2.2.1 トップダウン分析による市場規模推定のアプローチ 41

2.3 データの三角測量 43

2.4 リサーチの前提 44

2.5 調査の限界 44

3 エグゼクティブサマリー 45

4 プレミアムインサイト 51

4.1 ベクターコントロール市場における魅力的な市場機会 51

4.2 北米:ベクターコントロール市場:最終用途分野別、国別 52

4.3 ベクターコントロール市場:主要地域サブマーケットのシェア 52

4.4 ベクターコントロール市場:技術別、地域別 53

4.5 ベクターコントロール市場:コントロール方法別・地域 54

4.6 ベクターコントロール市場:ベクタータイプ別・地域別 55

4.7 ベクターコントロール市場:最終用途分野別・地域別 56

4.8 ベクターコントロール市場:用途モード別・地域別 57

5 市場の概要 58

5.1 はじめに 58

5.2 マクロ経済見通し 58

5.2.1 人口増加と都市化 58

5.2.2 媒介虫疾患の増加をもたらす気候変動 59

5.3 市場ダイナミクス 60

5.3.1 推進要因 60

5.3.1.1 市場成長を促進する技術革新 60

5.3.1.2 政府のイニシアティブと資金提供 61

5.3.2 阻害要因

5.3.2.1 媒介虫駆除のための高い経済コスト 61

5.3.2.2 媒介生物駆除製品の厳しい規制承認プロセス 61

5.3.3 機会 62

5.3.3.1 総合的媒介蚊管理戦略の採用 62

5.3.3.2 生物学的防除ソリューションに対する需要の高まり 62

5.3.4 課題 63

5.3.4.1 媒介虫における耐性菌の発生 63

5.3.4.2 媒介生物防除製品の環境および非標的への影響 63

5.4 媒介生物防除市場における AI/GEN AIの影響 64

5.4.1 導入 64

5.4.2 媒介生物防除における遺伝子AIの使用 65

5.4.3 ケーススタディ分析 66

5.4.3.1 VECTRACK プロジェクト – 蚊媒介性疾患対策のためのベクターサーベイランスの推進 66

5.4.3.2 IoT とクラウド統合で害虫駆除を変革するアンティシメックス 66

6 業界動向 68

6.1 はじめに 68

6.2 バリューチェーン分析 68

6.2.1 研究開発 69

6.2.2 原材料調達 69

6.2.3 製造 69

6.2.4 流通・物流 69

6.2.5 マーケティング&販売 70

6.2.6 最終用途への応用 70

6.3 貿易分析 70

6.3.1 HSコード3808の輸出シナリオ 70

6.3.2 HSコード3808の輸入シナリオ 72

6.4 技術分析 73

6.4.1 主要技術 73

6.4.1.1 殺虫剤処理ネット(ITN) 73

6.4.2 補足技術 73

6.4.2.1 屋内残留散布(IRS) 73

6.4.3 隣接技術 74

6.4.3.1 殺虫技術(SIT) 74

6.5 価格分析 74

6.5.1 主要企業の平均販売価格動向(適用形態別) 74

6.5.2 スプレーの平均販売価格動向(地域別) 74

6.5.3 ペレットの地域別平均販売価格動向 78

6.5.4 パウダーの地域別平均販売価格動向 79

6.6 エコシステム分析 79

6.6.1 需要サイド 79

6.6.2 供給サイド 79

6.7 顧客のビジネスに影響を与えるトレンド/混乱 81

6.8 特許分析 82

6.9 主要会議・イベント(2024-2025年) 86

6.10 規制の状況 87

6.10.1 規制機関、政府機関、その他の組織 87

6.10.2 米国 90

6.10.3 カナダ 93

6.10.4 欧州 93

6.10.4.1 欧州有害生物管理連合(CEPA) 95

6.10.4.2 欧州食品安全機関(EFSA) 95

6.10.4.3 欧州標準化委員会(CEN) 95

6.10.4.4 殺生物性製品規則(BPR) 95

6.10.4.5 欧州委員会施行規則(EU)2017/1376 95

6.10.5 アジア太平洋 95

6.10.5.1 インド 96

6.10.5.1.1 殺虫剤法 96

6.10.5.1.2 中央殺虫剤委員会(CIB) 96

6.10.5.1.3 殺虫剤規則 96

6.10.5.1.4 農薬管理法案 97

6.10.5.2 中国 97

6.10.5.2.1 中国における新規化学物質の届出 98

6.10.5.2.2 中国標準化管理局(SAC) 98

6.10.5.2.3 規制農薬管理(RPA) 98

6.10.5.3 オーストラリア 98

6.10.6 南アメリカ 99

6.10.6.1 ブラジル 99

6.10.6.2 アルゼンチン 99

6.10.7 その他の地域 99

6.10.7.1 南アフリカ 99

6.10.7.2 アラブ首長国連邦 99

6.11 ポーターのファイブフォース分析 100

6.11.1 競争相手の強さ 101

6.11.2 サプライヤーの交渉力 101

6.11.3 買い手の交渉力 101

6.11.4 代替品の脅威 102

6.11.5 新規参入の脅威 102

6.12 主要ステークホルダーと購買基準 102

6.12.1 購入プロセスにおける主要ステークホルダー 102

6.12.2 購入基準 103

6.13 ケーススタディ分析 105

6.13.1 アンチシメックスのiot ソリューションがデジタル連結トラップの構築に貢献 105

6.13.2 レントキルは顧客基盤の拡大と顧客維持率の向上に iot ソリューションを活用 105

6.13.3 ネオジェン・コーポレーションの Surekill gel bait pro applicator の発売 106

6.14 投資と資金調達のシナリオ 106

7 媒介虫駆除市場、駆除方法別 107

7.1 導入 108

7.2 包括的防除 109

7.2.1 包括的防除は迅速かつ大規模な効果をもたらすため、マラリアやデング熱のホットスポットのような、 ベクターが媒介する緊急の健康脅威に直面している地域に最適 109

7.3 標的型 110

7.3.1 的を絞った防除法の精度と汎用性が需要を喚起する可能性 110

7.4 総合的媒介蚊管理(IVM) 111

7.4.1 産業用・商業用の最終用途産業でより幅広い適応を可能にする政府組織からの規制支援 111

8 ベクターコントロール市場、最終用途分野別 112

8.1 導入 113

8.2 住宅 114

8.2.1 シロアリや害虫による構造的被害が防疫市場に有利な環境を創出 114

8.3 商業 115

8.3.1 商業環境における多様な規制要件やコンプライアンス要件を満たす必要性が、 媒介虫防除ソリューションの需要を促進 115

8.4 産業用 117

8.4.1 品質保証とともに従業員の健康と安全に対する関心の高まりが、より厳格な有害生物防除プロトコルの採用を促す 117

9 媒介虫防除市場、用途モード別 119

9.1 導入 120

9.2 ペレット 121

9.2.1 特に水域での幼虫駆除用途における標的効果によって強く牽引されるペレット製品の需要 121

9.3 スプレー 123

9.3.1 急速な都市化により、効率的なスプレーベースの媒介蚊防除ソリューションへの需要が高 まっている 123

9.4 粉剤 125

9.4.1 雨のような要素に対しても表面に付着する粉剤の耐久性により、屋外環境での再塗布の必要性を最小限に抑えることができるため、好んで使用されている 125

10 ベクターコントロール市場:技術別 127

10.1 導入 128

10.2 化学物質 129

10.2.1 昆虫による構造的被害がベクターコントロール市場に有利な環境を創出 129

10.2.2 昆虫とその他の媒介生物 130

10.2.2.1 ピレスロイド 131

10.2.2.2 フィプロニル 131

10.2.2.3 有機リン剤 131

10.2.2.4 幼虫駆除剤 131

10.2.2.5 その他の化学物質 131

10.2.3 げっ歯類 132

10.2.3.1 抗凝固剤 132

10.2.3.1.1 第一世代抗凝固剤 133

10.2.3.1.2 第二世代抗凝固薬 133

10.2.3.2 非抗凝固薬 133

10.2.3.2.1 ブロメタリン 134

10.2.3.2.2 コレカルシフェロール 135

10.2.3.2.3 ストリキニーネ 135

10.2.3.2.4 リン化亜鉛 135

10.3 物理的・機械的 135

10.3.1 特に化学農薬の使用規制が厳しい地域で、持続可能な害虫管理に対する規制支援がこの分野の成長を牽引 135

10.3.2 トラップ&ベイト剤 137

10.3.3 紫外線デバイス 137

10.3.4 その他の物理的・機械的方法 137

10.4 生物学的方法 138

10.4.1 環境の持続可能性と化学農薬への依存度の低減が生物学的製品の需要を牽引 138

10.4.2 微生物 139

10.4.2.1 細菌 140

10.4.2.2 真菌 140

10.4.2.3 その他 140

10.4.3 植物性 140

10.4.3.1 エッセンシャルオイル 141

10.4.3.2 オレオレジン 141

10.4.3.3 その他 142

10.4.4 捕食者 142

10.5 その他の技術 142

11 ベクターコントロール市場(ベクタータイプ別) 144

11.1 導入 145

11.2 昆虫 146

11.2.1 世界的な媒介性疾患の流行増加と都市化の進展が需要を促進 146

11.2.2 蚊 147

11.2.3 ハエ 148

11.2.4 ゴキブリ 148

11.2.5 その他の昆虫 149

11.3 げっ歯類 149

11.3.1 レプトスピラ症、ハンタウイルス、サルモネラ症の増加が市場成長を促進 149

11.3.2 ねずみ 150

11.3.3 マウス 151

11.3.4 その他のげっ歯類 151

11.4 その他の媒介動物の種類 151

12 ベクター対策市場:地域別 153

12.1 はじめに 154

12.2 北米 156

12.2.1 米国 161

12.2.1.1 主要企業による政府戦略と技術革新が米国市場を牽引 161

12.2.2 カナダ 163

12.2.2.1 カナダのベクターコントロール市場を牽引する政府の支援 163

12.2.3 メキシコ 164

12.2.3.1 メキシコにおける蚊媒介性疾患の増加が媒介蚊駆除ソリューションの需要を促進 164

12.3 欧州 166

12.3.1 フランス 170

12.3.1.1 都市人口の増加と媒介蚊の蔓延がフランス市場の成長を促進 170

12.3.2 ドイツ 171

12.3.2.1 ドイツの持続可能な開発目標が媒介虫駆除の需要を促進 171

12.3.3 スペイン 173

173 12.3.3.1 気候変動が媒介動物の数を急増させ、スペインの媒介動物駆除需要を促進 173

12.3.4 イタリア 174

12.3.4.1 共同研究による科学研究の増加がイタリア市場を牽引 174

12.3.5 英国 176

12.3.5.1 主要業界プレイヤーの存在とベクターコントロールの技術革新が英国市場を牽引 176

12.3.6 その他の欧州 177

12.4 アジア太平洋地域 179

12.4.1 中国 183

12.4.1.1 中国におけるベクター対策への政府の取り組みが市場成長を促進 183

12.4.2 インド 185

12.4.2.1 インドでは業界主要企業による戦略的買収が市場成長を促進 185

12.4.3 日本 187

12.4.3.1 日本では都市化の進展により媒介性疾患の抑制ニーズが増加 187

12.4.4 オーストラリア・ニュージーランド 188

12.4.4.1 媒介生物対策製品開発企業との連携がオーストラリア・ニュージーランドにおける媒介生物対策製品の需要を促進 188

12.4.5 その他のアジア太平洋地域 190

12.5 南米 191

12.5.1 ブラジル 195

12.5.1.1 ブラジルの市場成長を促進するパートナーシップと革新的なベクターコントロールソリューション 195

12.5.2 アルゼンチン 197

12.5.2.1 アルゼンチンでは新製品開発のための企業間連携が市場成長を牽引 197

12.5.3 その他の南米 198

12.6 その他の地域(列記) 200

12.6.1 アフリカ 204

12.6.1.1 アフリカでは遺伝子ベースのベクター対策が市場成長を牽引 204

12.6.2 中東 205

12.6.2.1 中東における世界的なベクター対策対応プログラムの実施がベクター対策市場の成長を加速する 205

13 競争環境 208

13.1 概要 208

13.2 主要プレイヤーの戦略/勝利への権利 208

13.3 セグメント別収益分析 211

13.4 市場シェア分析、2023年 212

13.5 企業評価マトリックス:主要企業(2023年) 213

13.5.1 スター企業 213

13.5.2 新興リーダー 213

13.5.3 浸透型プレーヤー 214

13.5.4 参加企業 214

13.5.5 企業フットプリント:主要プレーヤー(2023年) 215

13.5.5.1 企業フットプリント 215

13.5.5.2 技術のフットプリント 216

13.5.5.3 最終用途部門のフットプリント 217

13.5.5.4 用途別フットプリント 218

13.5.5.5 地域別フットプリント 219

13.6 企業評価マトリクス:新興企業/SM(2023年) 220

13.6.1 進歩的企業 220

13.6.2 対応力のある企業 220

13.6.3 ダイナミックな企業 220

13.6.4 スタートアップ・ブロック 220

13.6.5 競争ベンチマーキング:新興企業/SM(2023年) 222

13.6.5.1 主要新興企業/中小企業の詳細リスト 222

13.6.5.2 主要新興企業/SMEの競合ベンチマーキング 223

13.7 企業評価と財務指標 224

13.8 ブランド/製品/サービス分析 225

13.9 競争シナリオと動向 226

13.9.1 製品発売 226

13.9.2 取引 228

13.9.3 拡張 232

14 会社プロファイル 233

BASF SE (Germany)

Rentokil Initial Plc (UK)

Sumitomo Chemical Co.Ltd. (Japan)

Syngenta Group (Switzerland)

FMC Corporation (US)

Ecolab (US)

Rollins Inc. (US)

Anticimex (Sweden)

UPL (India)

Neogen Corporation (US)

Senestech Inc. (US)

Environmental Science U.S. Inc. (US)

Bell Laboratories Inc. (US)

Pelgar International (UK)

S. C. Johnson & Son Inc. (US).

Futura Gmbh (Germany)

JT Eaton (US)

Liphatech Inc. (US)

Impex Europa S.L. (Spain)

ENSYSTEX (US)

Abell Pest Control (Canada)

Bioguard Pest Solutions (US)

Spotta Ltd (UK)

Massey Services Inc. (US)

Barefoot Mosquito & Pest Control (US)

and Pest Share (US)

15 隣接市場と関連市場 303

15.1 はじめに 303

15.2 制限 303

15.3 殺鼠剤市場 304

15.3.1 市場の定義 304

15.3.2 市場概要 304

15.4 ペストコントロール市場 305

15.4.1 市場の定義 305

15.4.2 市場概要 305

15.5 害虫市場 306

15.5.1 市場の定義 306

15.5.2 市場概要 306

16 付録 308

16.1 ディスカッションガイド 308

16.2 Knowledgestore: Marketsandmarketsの購読ポータル 312

16.3 カスタマイズオプション 314

16.4 関連レポート 314

16.5 著者の詳細 315

Adoption of AI is changing the vector control market, since it encompasses real-time surveillance and predictive models that adopts data-driven methods for handling mosquitoes and rodents. This technology develop the quality of outbreak detection, making interventions both effective and sustainable. In November 2023, a machine olfaction startup Osmo (US) was awarded USD 3.5 million by the Bill & Melinda Gates Foundation to advance its scatology-building AI scent platform as a tool for discovering compounds to repel or kill disease-carrying insects. In July 2023, Vergo Pest Management (UK) launched Pest Alert Sight, an AI-driven thermal imaging solution that offers non-invasive, real-time detection and targeted rodent control through advanced heat signature analysis.

Disruption in the vector control market: Technological advancements are disrupting the vector control market by offering more precise and efficient solutions. AI and IoT-based surveillance technologies further enhance any time monitoring of population parameters of vectors, while analytics and predictive modeling continue to strengthen the strength of control strategies. Biological control methods provide eco-friendly alternatives to chemical pesticides.

Some of the key disruptions in the vector control market include:

•Internet of Things (IoT): IoT devices enable constant monitoring of vector habitats and populations by connected sensors and smart traps. In this way, data collection and management will be efficient.

•Bio-Control Methods: Increased research on the development and application of biological control agents, including genetically modified organisms and natural predators, allows for safe and sustainable alternatives to chemical pesticides.

•Genomic Technologies: Advances in the field of genomic research now open up possibilities to develop targeted control methods, such as gene drived technologies with the potential to alter or suppress vector populations at the very genetic level.

“The spray segment holds the highest share in the mode of application segment of vector control market.”

The spray mode of application currently remains with the highest market share in the vector control market, due to its efficiency and effectiveness in the delivery over great areas. This mode of application allows precise targeting of vector populations with a rapid reduction of pest densities while minimizing exposure to non-target organisms. Advances in the application equipment further support widespread adoption of spray technology because they optimize the coverage and penetration of chemicals, thus also optimizing the control of vector-borne diseases. As a result, as public health initiatives continue to emphasize managing vectors, spray application will be maintained at the top position in the market. To prevent malaria, the WHO advises two extensive interventions in control vectors: insecticide-treated nets and IRS (Indoor residual spraying). IRS is an activity of applying insecticides in interior locations of homes and buildings that have a potential where disease-causing insects may rest. Although IRS mainly targets Anopheles mosquito species responsible for spreading malaria, it also destroys other disease-causing insects.

“The physical & mechanical segment is projected to hold a significant market share in the technology segment during the forecast period.”

Physical & Mechanical segment hold significant share in vector control market due to their ease of application and eco-friendly attributes. This includes trapping, habitat modification, and barriers as approaches rather than using chemical pesticides. These technologies not only reduce the risk of resistance development among the vector populations but also meet consumer needs for eco-friendly pest management solutions, as more and more customers work to stay away from synthetic chemicals. Anticimex (Sweden) provides In2Care Mosquito Trap that helps control the mosquito which is responsible for transferring diseases. Entotherm heat treatment offered by Rentokil Initial Plc (UK) is a form of commercial pest control that uses heat to kill pests. Similarly, mechanical traps are used to control rodents.

"North America is expected to hold highest share in the vector control market."

North America holds the highest share in the vector control market. This is essentially because of the increased cases of Lyme disease, West Nile virus, and Zika virus together with tremendous support from the regulatory side in public health programs. One of the key government initiatives has been the VBD National Strategy which is the biggest formal federal coordination concerning vector-borne disease (VBD) prevention and control. Supported by the US Developed in coordination with six federal departments and the Environmental Protection Agency at the request of the Department of Health and Human Services and the Centers for Disease Control and Prevention, this strategy goes further to underscore the region's commitment towards vector-borne threat mitigation efforts. The adoption of advanced technologies as AI-enabled monitoring systems and sustainable vector control solutions are driving the vector control market in the region.

In-depth interviews have been conducted with chief executive officers (CEOs), Directors, and other executives from various key organizations operating in the vector control market:

• By Company Type: Tier 1 – 25%, Tier 2 – 45%, and Tier 3 – 30%

• By Designation: CXO’s – 20%, Managers – 50%, Executives- 30%

• By Region: North America – 25%, Europe – 30%, Asia Pacific – 20%, South America – 15% and Rest of the World –10%

Prominent companies in the market include BASF SE (Germany), Rentokil Initial Plc (UK), Sumitomo Chemical Co., Ltd. (Japan), Syngenta Group (Switzerland), FMC Corporation (US), Ecolab (US), Rollins Inc. (US), Anticimex (Sweden), UPL (India), Neogen Corporation (US), Senestech, Inc. (US), Environmental Science U.S. Inc. (US), Bell Laboratories Inc. (US), Pelgar International (UK), S. C. Johnson & Son, Inc. (US).

Other players include Futura Gmbh (Germany), JT Eaton (US), Liphatech, Inc. (US), Impex Europa S.L. (Spain), ENSYSTEX (US), Abell Pest Control (Canada), Bioguard Pest Solutions (US), Spotta Ltd (UK), Massey Services, Inc. (US), Barefoot Mosquito & Pest Control (US), and Pest Share (US).

Research Coverage:

This research report categorizes the vector control market by technology (chemical, physical & mechanical, biological, and other technologies), control method (comprehensive, targeted, and integrated vector management), vector type (insects, rodents, and other vector types), end-use sector (residential, commercial, industrial), mode of application (pellets, spray, powder) and region (North America, Europe, Asia Pacific, South America, and Rest of the World). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of vector control market. A detailed analysis of the key industry players has been done to provide insights into their business overview, services, key strategies, contracts, partnerships, agreements, new service launches, mergers and acquisitions, and recent developments associated with the vector control market. Competitive analysis of upcoming startups in the vector control market ecosystem is covered in this report. Furthermore, industry-specific trends such as technology analysis, ecosystem and market mapping, patent, regulatory landscape, among others, are also covered in the study.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall vector control and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

• Analysis of key drivers (rising vector diseases), restraints (environmental hazard of chemical vector control products), opportunities (increasing adoption of integrated vector management technique) and challenges (development of certain insecticide resistance in vectors) influencing the growth of the vector control smarket.

• New product launch/Innovation: Detailed insights on research & development activities and new product launches in the vector control market.

• Market Development: Comprehensive information about lucrative markets – the report analyzes the vector control market across varied regions.

• Market Diversification: Exhaustive information about new services, untapped geographies, recent developments, and investments in the vector control market.

• Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, brand/product comparison, and product foot prints of leading players such as BASF SE (Germany), Rentokil Initial Plc (UK), Anticimex (Sweden), Ecolab (US), and other players in the vector control market.

1 INTRODUCTION 29

1.1 STUDY OBJECTIVES 29

1.1.1 MARKET DEFINITION 29

1.2 MARKET SCOPE 30

1.2.1 MARKET SEGMENTATION 30

1.2.2 INCLUSIONS & EXCLUSIONS 31

1.3 YEARS CONSIDERED 31

1.4 UNIT CONSIDERED 32

1.4.1 CURRENCY/VALUE UNIT 32

1.4.2 VOLUME CONSIDERED 33

1.5 STAKEHOLDERS 33

1.6 SUMMARY OF CHANGES 34

2 RESEARCH METHODOLOGY 35

2.1 RESEARCH DATA 35

2.1.1 SECONDARY DATA 36

2.1.1.1 Key data from secondary sources 36

2.1.2 PRIMARY DATA 37

2.1.2.1 Key data from primary sources 37

2.1.2.2 Key industry insights 38

2.1.2.3 Breakdown of primaries 38

2.2 MARKET SIZE ESTIMATION 39

2.2.1 BOTTOM-UP APPROACH 39

2.2.2 TOP-DOWN APPROACH 40

2.2.2.1 Approach to estimate market size using top-down analysis 41

2.3 DATA TRIANGULATION 43

2.4 RESEARCH ASSUMPTIONS 44

2.5 RESEARCH LIMITATIONS 44

3 EXECUTIVE SUMMARY 45

4 PREMIUM INSIGHTS 51

4.1 ATTRACTIVE MARKET OPPORTUNITIES IN VECTOR CONTROL MARKET 51

4.2 NORTH AMERICA: VECTOR CONTROL MARKET, BY END-USE SECTOR AND COUNTRY 52

4.3 VECTOR CONTROL MARKET: SHARE OF MAJOR REGIONAL SUBMARKETS 52

4.4 VECTOR CONTROL MARKET, BY TECHNOLOGY AND REGION 53

4.5 VECTOR CONTROL MARKET, BY CONTROL METHOD AND REGION 54

4.6 VECTOR CONTROL MARKET, BY VECTOR TYPE AND REGION 55

4.7 VECTOR CONTROL MARKET, BY END-USE SECTOR AND REGION 56

4.8 VECTOR CONTROL MARKET, BY MODE OF APPLICATION AND REGION 57

5 MARKET OVERVIEW 58

5.1 INTRODUCTION 58

5.2 MACROECONOMIC OUTLOOK 58

5.2.1 RISING POPULATION AND URBANIZATION 58

5.2.2 CLIMATE CHANGE LEADING TO INCREASE IN VECTOR DISEASES 59

5.3 MARKET DYNAMICS 60

5.3.1 DRIVERS 60

5.3.1.1 Technological innovations to drive market growth 60

5.3.1.2 Government initiatives and funding 61

5.3.2 RESTRAINTS 61

5.3.2.1 High economic costs for vector control 61

5.3.2.2 Stringent regulatory approval process for vector control products 61

5.3.3 OPPORTUNITIES 62

5.3.3.1 Adopting Integrated Vector Management strategies 62

5.3.3.2 Growing demand for biological control solutions 62

5.3.4 CHALLENGES 63

5.3.4.1 Resistance development in vectors 63

5.3.4.2 Environmental and non-target impact of vector control products 63

5.4 IMPACT OF AI/GEN AI ON VECTOR CONTROL MARKET 64

5.4.1 INTRODUCTION 64

5.4.2 USE OF GEN AI IN VECTOR CONTROL 65

5.4.3 CASE STUDY ANALYSIS 66

5.4.3.1 VECTRACK Project - Advancing Vector Surveillance for Mosquito-Borne Disease Control 66

5.4.3.2 Anticimex Transforms Pest Control with IoT and Cloud Integration 66

6 INDUSTRY TRENDS 68

6.1 INTRODUCTION 68

6.2 VALUE CHAIN ANALYSIS 68

6.2.1 RESEARCH & DEVELOPMENT 69

6.2.2 RAW MATERIAL SOURCING 69

6.2.3 MANUFACTURING 69

6.2.4 DISTRIBUTION & LOGISTICS 69

6.2.5 MARKETING & SALES 70

6.2.6 END-USE APPLICATION 70

6.3 TRADE ANALYSIS 70

6.3.1 EXPORT SCENARIO OF HS CODE 3808 70

6.3.2 IMPORT SCENARIO OF HS CODE 3808 72

6.4 TECHNOLOGY ANALYSIS 73

6.4.1 KEY TECHNOLOGIES 73

6.4.1.1 Insecticide-treated Nets (ITNs) 73

6.4.2 COMPLEMENTARY TECHNOLOGY 73

6.4.2.1 Indoor Residual Spraying (IRS) 73

6.4.3 ADJACENT TECHNOLOGIES 74

6.4.3.1 Sterile Insect Technique (SIT) 74

6.5 PRICING ANALYSIS 74

6.5.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY MODE OF APPLICATION 74

6.5.2 AVERAGE SELLING PRICE TREND OF SPRAYS, BY REGION 77

6.5.3 AVERAGE SELLING PRICE TREND OF PELLETS, BY REGION 78

6.5.4 AVERAGE SELLING PRICE TREND OF POWDER, BY REGION 79

6.6 ECOSYSTEM ANALYSIS 79

6.6.1 DEMAND SIDE 79

6.6.2 SUPPLY SIDE 79

6.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS’ BUSINESSES 81

6.8 PATENT ANALYSIS 82

6.9 KEY CONFERENCES & EVENTS, 2024–2025 86

6.10 REGULATORY LANDSCAPE 87

6.10.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS 87

6.10.2 US 90

6.10.3 CANADA 93

6.10.4 EUROPE 93

6.10.4.1 Confederation of European Pest Management Association (CEPA) 95

6.10.4.2 European Food Safety Authority (EFSA) 95

6.10.4.3 European Committee for Standardization (CEN) 95

6.10.4.4 Biocidal Product Regulation (BPR) 95

6.10.4.5 Commission Implementing Regulation (EU) 2017/1376 95

6.10.5 ASIA PACIFIC 95

6.10.5.1 India 96

6.10.5.1.1 Insecticides Act 96

6.10.5.1.2 Central Insecticides Board (CIB) 96

6.10.5.1.3 Insecticides Rules 96

6.10.5.1.4 Pesticide Management Bill 97

6.10.5.2 China 97

6.10.5.2.1 New Chemical Substance Notification in China 98

6.10.5.2.2 Standardization Administration of China (SAC) 98

6.10.5.2.3 Regulation Pesticide Administration (RPA) 98

6.10.5.3 Australia 98

6.10.6 SOUTH AMERICA 99

6.10.6.1 Brazil 99

6.10.6.2 Argentina 99

6.10.7 REST OF THE WORLD 99

6.10.7.1 South Africa 99

6.10.7.2 UAE 99

6.11 PORTER’S FIVE FORCES ANALYSIS 100

6.11.1 INTENSITY OF COMPETITIVE RIVALRY 101

6.11.2 BARGAINING POWER OF SUPPLIERS 101

6.11.3 BARGAINING POWER OF BUYERS 101

6.11.4 THREAT OF SUBSTITUTES 102

6.11.5 THREAT OF NEW ENTRANTS 102

6.12 KEY STAKEHOLDERS AND BUYING CRITERIA 102

6.12.1 KEY STAKEHOLDERS IN BUYING PROCESS 102

6.12.2 BUYING CRITERIA 103

6.13 CASE STUDY ANALYSIS 105

6.13.1 ANTICIMEX’S IOT SOLUTION HELPED CREATE DIGITAL CONNECTED TRAPS 105

6.13.2 RENTOKIL USED IOT SOLUTIONS TO INCREASE ITS CUSTOMER BASE AND IMPROVE CUSTOMER RETENTION 105

6.13.3 NEOGEN CORPORATION'S LAUNCH OF SUREKILL GEL BAIT PRO APPLICATOR 106

6.14 INVESTMENT AND FUNDING SCENARIO 106

7 VECTOR CONTROL MARKET, BY CONTROL METHOD 107

7.1 INTRODUCTION 108

7.2 COMPREHENSIVE 109

7.2.1 COMPREHENSIVE CONTROL IS HIGHLY EFFECTIVE FOR SWIFT, LARGE-SCALE IMPACT, MAKING IT IDEAL FOR REGIONS FACING URGENT VECTOR-BORNE HEALTH THREATS, LIKE MALARIA OR DENGUE HOTSPOTS 109

7.3 TARGETED 110

7.3.1 PRECISION AND VERSATILITY OF TARGETED CONTROL METHODS LIKELY TO FUEL DEMAND 110

7.4 INTEGRATED VECTOR MANAGEMENT (IVM) 111

7.4.1 REGULATORY SUPPORT FROM GOVERNMENT ORGANIZATIONS TO MAKE WIDER ADAPTABILITY AMONG INDUSTRIAL AND COMMERCIAL END-USE INDUSTRIES 111

8 VECTOR CONTROL MARKET, BY END-USE SECTOR 112

8.1 INTRODUCTION 113

8.2 RESIDENTIAL 114

8.2.1 STRUCTURAL DAMAGE CAUSED BY TERMITES AND BUGS CREATES FAVORABLE ENVIRONMENT FOR VECTOR CONTROL MARKET 114

8.3 COMMERCIAL 115

8.3.1 NEED TO MEET DIVERSE REGULATORY AND COMPLIANCE REQUIREMENTS IN COMMERCIAL SETTINGS TO DRIVE DEMAND FOR VECTOR CONTROL SOLUTIONS 115

8.4 INDUSTRIAL 117

8.4.1 RISING CONCERN FOR EMPLOYEE HEALTH AND SAFETY, ALONG WITH QUALITY ASSURANCE, PROMPTING INDUSTRIES TO ADOPT MORE RIGOROUS PEST CONTROL PROTOCOLS 117

9 VECTOR CONTROL MARKET, BY MODE OF APPLICATION 119

9.1 INTRODUCTION 120

9.2 PELLETS 121

9.2.1 DEMAND FOR PELLET PRODUCTS STRONGLY DRIVEN BY THEIR TARGETED EFFECTIVENESS IN LARVICIDAL APPLICATIONS, PARTICULARLY IN WATER BODIES 121

9.3 SPRAY 123

9.3.1 RAPID URBANIZATION HAS INTENSIFIED DEMAND FOR EFFICIENT SPRAY-BASED VECTOR CONTROL SOLUTIONS 123

9.4 POWDER 125

9.4.1 DURABILITY OF POWDERS ON SURFACES, EVEN AGAINST ELEMENTS LIKE RAIN, HAS MADE THEM FAVORED CHOICE, MINIMIZING REAPPLICATION NEEDS IN OUTDOOR SETTINGS 125

10 VECTOR CONTROL MARKET, BY TECHNOLOGY 127

10.1 INTRODUCTION 128

10.2 CHEMICAL 129

10.2.1 STRUCTURAL DAMAGE CAUSED BY INSECTS CREATES FAVORABLE ENVIRONMENT FOR VECTOR CONTROL MARKET 129

10.2.2 INSECTS & OTHER VECTORS 130

10.2.2.1 Pyrethroids 131

10.2.2.2 Fipronil 131

10.2.2.3 Organophosphates 131

10.2.2.4 Larvicides 131

10.2.2.5 Other Chemicals 131

10.2.3 RODENTS 132

10.2.3.1 Anticoagulants 132

10.2.3.1.1 First-generation Anticoagulants 133

10.2.3.1.2 Second-generation Anticoagulants 133

10.2.3.2 Non-anticoagulants 133

10.2.3.2.1 Bromethalin 134

10.2.3.2.2 Cholecalciferol 135

10.2.3.2.3 Strychnine 135

10.2.3.2.4 Zinc Phosphide 135

10.3 PHYSICAL & MECHANICAL 135

10.3.1 REGULATORY SUPPORT FOR SUSTAINABLE PEST MANAGEMENT, ESPECIALLY IN REGIONS WITH STRICT CONTROLS ON CHEMICAL PESTICIDE USE, TO DRIVE SEGMENT’S GROWTH 135

10.3.2 TRAPS & BAITS 137

10.3.3 ULTRAVIOLET DEVICES 137

10.3.4 OTHER PHYSICAL & MECHANICAL METHODS 137

10.4 BIOLOGICAL 138

10.4.1 ENVIRONMENTAL SUSTAINABILITY AND REDUCING DEPENDENCE ON CHEMICAL PESTICIDES DRIVING DEMAND FOR BIOLOGICAL PRODUCTS 138

10.4.2 MICROBIAL 139

10.4.2.1 Bacteria 140

10.4.2.2 Fungi 140

10.4.2.3 Others 140

10.4.3 BOTANICAL 140

10.4.3.1 Essential Oils 141

10.4.3.2 Oleoresins 141

10.4.3.3 Others 142

10.4.4 PREDATORS 142

10.5 OTHER TECHNOLOGIES 142

11 VECTOR CONTROL MARKET, BY VECTOR TYPE 144

11.1 INTRODUCTION 145

11.2 INSECTS 146

11.2.1 RISING PREVALENCE OF VECTOR-BORNE DISEASES GLOBALLY AND INCREASED URBANIZATION TO FUEL DEMAND 146

11.2.2 MOSQUITOES 147

11.2.3 FLIES 148

11.2.4 COCKROACHES 148

11.2.5 OTHER INSECTS 149

11.3 RODENTS 149

11.3.1 RISE IN CASES OF LEPTOSPIROSIS, HANTAVIRUS, AND SALMONELLOSIS TO FUEL MARKET GROWTH 149

11.3.2 RATS 150

11.3.3 MICE 151

11.3.4 OTHER RODENTS 151

11.4 OTHER VECTOR TYPES 151

12 VECTOR CONTROL MARKET, BY REGION 153

12.1 INTRODUCTION 154

12.2 NORTH AMERICA 156

12.2.1 US 161

12.2.1.1 Government strategies and technological innovation by key players to drive US market 161

12.2.2 CANADA 163

12.2.2.1 Government support to drive vector control market in Canada 163

12.2.3 MEXICO 164

12.2.3.1 Rise in mosquito-borne diseases in Mexico to drive demand for vector control solutions 164

12.3 EUROPE 166

12.3.1 FRANCE 170

12.3.1.1 Rise in urban population and vector infestations to drive French market growth 170

12.3.2 GERMANY 171

12.3.2.1 Germany’s sustainable development goals will fuel demand for vector control 171

12.3.3 SPAIN 173

12.3.3.1 Climate change has surged vector population, which will fuel demand for vector control in Spain 173

12.3.4 ITALY 174

12.3.4.1 Increase in scientific research through collaboration to drive Italian market 174

12.3.5 UK 176

12.3.5.1 Presence of key industry players and technological innovations in vector control to drive market in UK 176

12.3.6 REST OF EUROPE 177

12.4 ASIA PACIFIC 179

12.4.1 CHINA 183

12.4.1.1 Government initiatives for vector control in China to drive market growth 183

12.4.2 INDIA 185

12.4.2.1 Strategic acquisitions by key industry players to drive market growth in India 185

12.4.3 JAPAN 187

12.4.3.1 Rising urbanization leading to rise in need to control vector-borne diseases in Japan 187

12.4.4 AUSTRALIA & NEW ZEALAND 188

12.4.4.1 Collaboration with vector control product developers to fuel demand for vector control products in Australia & New Zealand 188

12.4.5 REST OF ASIA PACIFIC 190

12.5 SOUTH AMERICA 191

12.5.1 BRAZIL 195

12.5.1.1 Partnerships and innovative vector control solutions to drive market growth in Brazil 195

12.5.2 ARGENTINA 197

12.5.2.1 Collaboration between companies to develop new products to drive market growth in Argentina 197

12.5.3 REST OF SOUTH AMERICA 198

12.6 REST OF THE WORLD (ROW) 200

12.6.1 AFRICA 204

12.6.1.1 Genetic-based vector control to drive market growth in Africa 204

12.6.2 MIDDLE EAST 205

12.6.2.1 Implementation of global vector control response program in Middle East to accelerate vector control market growth 205

13 COMPETITIVE LANDSCAPE 208

13.1 OVERVIEW 208

13.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN 208

13.3 SEGMENTAL REVENUE ANALYSIS 211

13.4 MARKET SHARE ANALYSIS, 2023 212

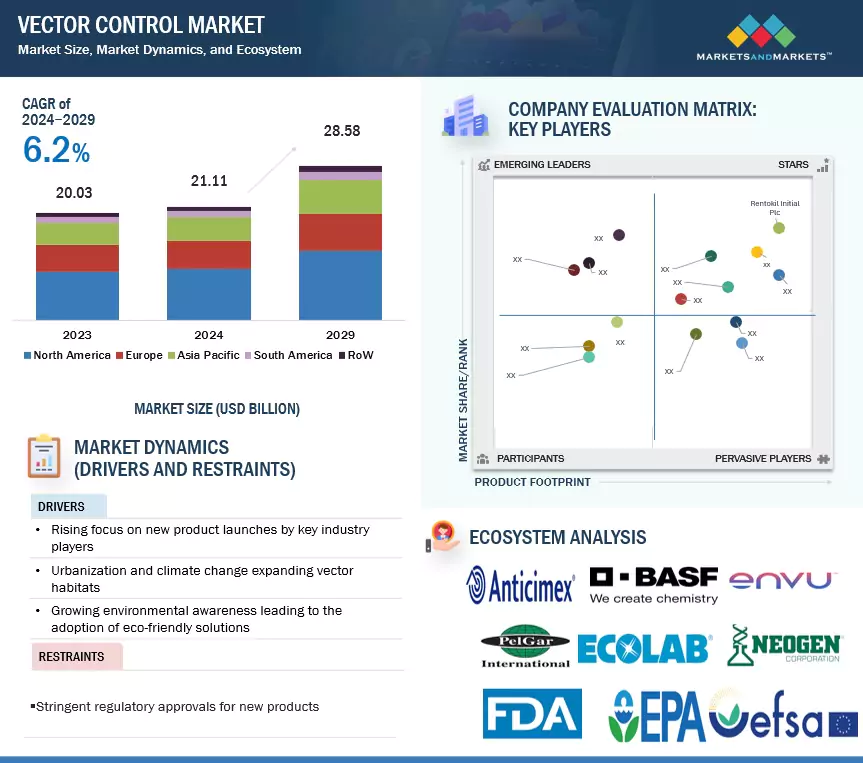

13.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023 213

13.5.1 STARS 213

13.5.2 EMERGING LEADERS 213

13.5.3 PERVASIVE PLAYERS 214

13.5.4 PARTICIPANTS 214

13.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023 215

13.5.5.1 Company footprint 215

13.5.5.2 Technology footprint 216

13.5.5.3 End-use sector footprint 217

13.5.5.4 Mode of application footprint 218

13.5.5.5 Region footprint 219

13.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023 220

13.6.1 PROGRESSIVE COMPANIES 220

13.6.2 RESPONSIVE COMPANIES 220

13.6.3 DYNAMIC COMPANIES 220

13.6.4 STARTING BLOCKS 220

13.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2023 222

13.6.5.1 Detailed list of key startups/SMEs 222

13.6.5.2 Competitive benchmarking of key startups/SMEs 223

13.7 COMPANY VALUATION AND FINANCIAL METRICS 224

13.8 BRAND/PRODUCT/SERVICE ANALYSIS 225

13.9 COMPETITIVE SCENARIO AND TRENDS 226

13.9.1 PRODUCT LAUNCHES 226

13.9.2 DEALS 228

13.9.3 EXPANSIONS 232

14 COMPANY PROFILES 233

14.1 PRODUCT COMPANIES 233

14.1.1 BASF SE 233

14.1.1.1 Business overview 233

14.1.1.2 Products/Solutions/Services offered 235

14.1.1.3 Recent developments 236

14.1.1.3.1 Product launches 236

14.1.1.3.2 Deals 236

14.1.1.4 MnM view 237

14.1.1.4.1 Key strengths 237

14.1.1.4.2 Strategic choices 237

14.1.1.4.3 Weaknesses and competitive threats 237

14.1.2 RENTOKIL INITIAL PLC 238

14.1.2.1 Business overview 238

14.1.2.2 Products/Services/Solutions offered 239

14.1.2.3 Recent developments 240

14.1.2.3.1 Product launches 240

14.1.2.3.2 Deals 241

14.1.2.3.3 Expansions 242

14.1.2.4 MnM view 243

14.1.2.4.1 Key strengths 243

14.1.2.4.2 Strategic choices 243

14.1.2.4.3 Weaknesses and competitive threats 243

14.1.3 SUMITOMO CHEMICAL CO., LTD. 244

14.1.3.1 Business overview 244

14.1.3.2 Products/Solutions/Services offered 245

14.1.3.3 Recent developments 246

14.1.3.3.1 Deals 246

14.1.3.4 MnM view 247

14.1.3.4.1 Key strengths 247

14.1.3.4.2 Strategic choices 247

14.1.3.4.3 Weaknesses and competitive threats 247

14.1.4 SYNGENTA GROUP 248

14.1.4.1 Business overview 248

14.1.4.2 Products/Solutions/Services offered 249

14.1.4.3 Recent developments 250

14.1.4.3.1 Product launches 250

14.1.4.3.2 Expansions 251

14.1.4.4 MnM view 251

14.1.4.4.1 Key strengths 251

14.1.4.4.2 Strategic choices 251

14.1.4.4.3 Weaknesses and competitive threats 252

14.1.5 FMC CORPORATION 253

14.1.5.1 Business overview 253

14.1.5.2 Products/Solutions/Services offered 254

14.1.5.3 Recent developments 255

14.1.5.3.1 Deals 255

14.1.5.4 MnM view 256

14.1.5.4.1 Key strengths 256

14.1.5.4.2 Strategic choices 256

14.1.5.4.3 Weaknesses and competitive threats 256

14.1.6 UPL 257

14.1.6.1 Business overview 257

14.1.6.2 Products/Solutions/Services offered 258

14.1.6.3 MnM view 259

14.1.7 ANTICIMEX 260

14.1.7.1 Business overview 260

14.1.7.2 Products/Services/Solutions offered 261

14.1.7.3 Recent developments 262

14.1.7.3.1 Deals 262

14.1.7.4 MnM view 263

14.1.8 NEOGEN CORPORATION 264

14.1.8.1 Business overview 264

14.1.8.2 Products/Services/Solutions offered 265

14.1.8.3 Recent developments 266

14.1.8.3.1 Product launches 266

14.1.8.4 MnM view 267

14.1.9 SENESTECH, INC. 268

14.1.9.1 Business overview 268

14.1.9.2 Products/Services/Solutions offered 269

14.1.9.3 Recent developments 270

14.1.9.3.1 Product launches 270

14.1.9.3.2 Deals 270

14.1.9.4 MnM view 271

14.1.10 ENVIRONMENTAL SCIENCE U.S. INC. 272

14.1.10.1 Business overview 272

14.1.10.2 Products/Solutions/Services offered 272

14.1.10.3 Recent developments 273

14.1.10.3.1 Product launches 273

14.1.10.3.2 Deals 274

14.1.10.4 MnM view 274

14.1.11 BELL LABORATORIES INC. 275

14.1.11.1 Business overview 275

14.1.11.2 Products/Services/Solutions offered 275

14.1.11.3 Recent developments 277

14.1.11.3.1 Product launches 277

14.1.11.4 MnM view 278

14.1.12 PELGAR INTERNATIONAL 279

14.1.12.1 Business overview 279

14.1.12.2 Products/Solutions/Services offered 279

14.1.12.3 Recent developments 280

14.1.12.3.1 Product launches 280

14.1.12.4 MnM view 280

14.1.13 LIPHATECH, INC. 281

14.1.13.1 Business overview 281

14.1.13.2 Products/Services/Solutions offered 281

14.1.13.3 Recent developments 282

14.1.13.3.1 Product launches 282

14.1.13.3.2 Deals 283

14.1.13.4 MnM view 283

14.1.14 S. C. JOHNSON & SON, INC. 284

14.1.14.1 Business overview 284

14.1.14.2 Products/Solutions/Services offered 284

14.1.14.3 Recent developments 285

14.1.14.3.1 Product launches 285

14.1.14.4 MnM view 285

14.1.15 FUTURA GMBH 286

14.1.15.1 Business overview 286

14.1.15.2 Products/Services/Solutions offered 286

14.1.16 JT EATON 287

14.1.16.1 Business overview 287

14.1.16.2 Products/Services/Solutions offered 287

14.1.16.3 Recent developments 288

14.1.16.3.1 Product launches 288

14.1.16.3.2 Deals 288

14.1.16.4 MnM view 288

14.1.17 IMPEX EUROPA S.L. 289

14.1.17.1 Business overview 289

14.1.17.2 Products/Services/Solutions offered 289

14.1.18 ENSYSTEX 290

14.2 SERVICE COMPANIES 291

14.2.1 ECOLAB 291

14.2.1.1 Business overview 291

14.2.1.2 Products/Services/Solutions offered 292

14.2.1.3 Recent developments 293

14.2.1.3.1 Product launches 293

14.2.1.3.2 Deals 293

14.2.1.4 MnM view 294

14.2.2 ROLLINS, INC. 295

14.2.2.1 Business overview 295

14.2.2.2 Products/Services/Solutions offered 296

14.2.2.3 Recent developments 297

14.2.2.3.1 Deals 297

14.2.2.4 MnM view 298

14.2.3 ABELL PEST CONTROL 299

14.2.3.1 Business overview 299

14.2.3.2 Products/Services/Solutions offered 299

14.2.4 BIOGUARD PEST SOLUTIONS 300

14.2.4.1 Business overview 300

14.2.4.2 Products/Services/Solutions offered 300

14.2.5 SPOTTA LTD 301

14.2.6 MASSEY SERVICES, INC. 301

14.2.7 BAREFOOT MOSQUITO & PEST CONTROL 302

14.2.8 PEST SHARE 302

15 ADJACENT AND RELATED MARKETS 303

15.1 INTRODUCTION 303

15.2 LIMITATIONS 303

15.3 RODENTICIDES MARKET 304

15.3.1 MARKET DEFINITION 304

15.3.2 MARKET OVERVIEW 304

15.4 PEST CONTROL MARKET 305

15.4.1 MARKET DEFINITION 305

15.4.2 MARKET OVERVIEW 305

15.5 INSECT PEST MARKET 306

15.5.1 MARKET DEFINITION 306

15.5.2 MARKET OVERVIEW 306

16 APPENDIX 308

16.1 DISCUSSION GUIDE 308

16.2 KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL 312

16.3 CUSTOMIZATION OPTIONS 314

16.4 RELATED REPORTS 314

16.5 AUTHOR DETAILS 315

❖ 世界のベクターコントロール市場に関するよくある質問(FAQ) ❖

・ベクターコントロールの世界市場規模は?

→MarketsandMarkets社は2024年のベクターコントロールの世界市場規模を217億2000万米ドルと推定しています。

・ベクターコントロールの世界市場予測は?

→MarketsandMarkets社は2029年のベクターコントロールの世界市場規模を298億米ドルと予測しています。

・ベクターコントロール市場の成長率は?

→MarketsandMarkets社はベクターコントロールの世界市場が2024年~2029年に年平均6.5%成長すると予測しています。

・世界のベクターコントロール市場における主要企業は?

→MarketsandMarkets社は「BASF SE (Germany)、Rentokil Initial Plc (UK)、Sumitomo Chemical Co.、Ltd. (Japan)、Syngenta Group (Switzerland)、FMC Corporation (US)、Ecolab (US)、Rollins Inc. (US)、Anticimex (Sweden)、 UPL (India)、Neogen Corporation (US)、Senestech、Inc. (US)、Environmental Science U.S. Inc. (US)、Bell Laboratories Inc. (US)、Pelgar International (UK)、S. C. Johnson & Son、Inc. (US).、Futura Gmbh (Germany)、JT Eaton (US)、Liphatech、Inc. (US)、Impex Europa S.L. (Spain)、ENSYSTEX (US)、Abell Pest Control (Canada)、Bioguard Pest Solutions (US)、Spotta Ltd (UK)、Massey Services、Inc. (US)、Barefoot Mosquito & Pest Control (US)、and Pest Share (US)など ...」をグローバルベクターコントロール市場の主要企業として認識しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、納品レポートの情報と少し異なる場合があります。