1 はじめに 27

1.1 調査目的 27

1.2 市場の定義 27

1.3 市場範囲 28

1.3.1 ゼロ液体排出システム市場のセグメンテーション 28

1.3.2 含まれるものと除外されるもの 29

1.3.3 考慮した年数 30

1.3.4 通貨を考慮 30

1.3.5 単位の考慮 30

1.4 利害関係者 30

1.5 変更点のまとめ 31

2 調査方法 33

2.1 調査データ 33

2.1.1 二次データ 34

2.1.1.1 主な二次情報源 34

2.1.1.2 二次資料からの主要データ 34

2.1.2 一次データ 35

2.1.2.1 一次資料からの主なデータ 36

2.1.2.2 主要な業界インサイト 36

2.1.2.3 専門家へのインタビューの内訳 37

2.2 市場規模の推定 38

2.2.1 ボトムアップアプローチ 39

2.2.2 トップダウンアプローチ 39

2.3 データの三角測量 40

2.4 リサーチの前提 41

2.5 要因分析 41

2.6 成長予測 41

2.6.1 供給サイド

2.6.2 需要サイド

2.7 研究の限界 42

2.8 リスク評価 42

3 エグゼクティブ・サマリー 43

4 プレミアムインサイト 47

4.1 ゼロ液体排出システム市場におけるプレーヤーの機会 47

4.2 ゼロ液体排出システム市場:システム別 47

4.3 ゼロ液体排出システム市場:容量別 48

4.4 ゼロ液体排出システム市場:最終用途産業別 48

4.5 ゼロ液体排出システム市場:国別 49

5 市場の概要 50

5.1 導入 50

5.2 AI/GEN AIの影響 50

5.2.1 導入 50

5.2.2 影響の概要 50

5.2.2.1 AIと機械学習による液体排出ゼロシステムの変革 50

5.2.2.2 AI/GenAIの逆浸透膜へのインパクト 50

5.2.2.3 水処理とゼロ液体排出システムへのAIの影響 51

5.3 市場ダイナミクス 51

5.3.1 ドライバー 52

5.3.1.1 厳しい環境規制、産業の拡大、

アジア太平洋地域における水不足の増加 52

5.3.1.2 脱塩装置のコスト上昇傾向 52

5.3.1.3 水処理に関する厳しい規制の実施と新たな政策 53

5.3.1.4 持続可能性への取り組みに対する様々な組織のコミットメント 53

5.3.1.5 地域間での水不足の増加 54

5.3.2 抑制要因 54

5.3.2.1 高い初期投資とシステムの複雑さ 54

5.3.2.2 水処理における代替品の利用可能性 55

5.3.3 機会 55

5.3.3.1 水不足と環境悪化に対する社会的関心の高まり 55

環境悪化に対する社会的関心の高まり 55

5.3.3.2 アジア太平洋地域の新興経済国における産業の急速な成長 55

5.3.4 課題 56

5.3.4.1 高い保守・運用コスト 56

5.3.4.2 運転中の水損失の抑制 56

5.4 ポーターの5つの力分析 57

5.4.1 代替品の脅威 58

5.4.2 買い手の交渉力 58

5.4.3 新規参入企業の脅威 58

5.4.4 供給者の交渉力 58

5.4.5 競合ライバルの激しさ 58

5.5 主要ステークホルダーと購買基準 59

5.5.1 購入プロセスにおける主要ステークホルダー 59

5.5.2 購買基準 60

5.6 マクロ経済指標 60

5.6.1 世界のGDP動向 60

5.7 バリューチェーン分析 61

5.7.1 原材料サプライヤー 62

5.7.2 メーカー 62

5.7.3 供給業者/流通業者 62

5.7.4 最終用途産業 63

5.8 エコシステム 63

5.9 ケーススタディ分析 64

5.9.1 パールGTL工場における液体排出ゼロ 64

5.9.2 中国のCTX産業における廃水リサイクルと廃液ゼロ排出システム

システム 65

5.9.3 廃水処理における液体排出ゼロ 65

5.10 規制の状況 66

5.10.1 規制 66

5.10.1.1 欧州 66

5.10.1.2 アジア太平洋地域 67

5.10.1.3 北米 68

5.10.2 規制機関、政府機関、その他の機関 69

5.11 技術分析 71

5.11.1 主要技術 71

5.11.1.1 膜技術 71

5.11.2 補完的技術 71

5.11.2.1 限外ろ過技術 71

5.11.2.2 落下膜蒸発器 72

5.11.3 隣接技術 72

5.11.3.1 順浸透 72

5.12 顧客ビジネスに影響を与えるトレンド/混乱 73

5.13 貿易分析 73

5.13.1 輸出シナリオ(HSコード842121) 73

5.13.2 輸入シナリオ(HSコード842121) 75

5.14 主要会議・イベント(2024-2025年) 76

5.15 価格動向分析 77

5.15.1 平均販売価格(地域別) 77

5.15.2 ゼロ液排出システムの平均販売価格動向 77

5.15.3 ゼロ液体排出システムの主要メーカーの平均販売価格(容量別) 78

5.15.4 ゼロ液排出システム主要メーカー平均販売価格動向(最終用途産業別) 78

5.15.5 ゼロ液排出システム主要メーカー平均販売価格推移(最終用途産業別) 79

5.15.6 ゼロ液体排出システムの地域別平均販売価格 79

5.16 投資と資金調達シナリオ 80

5.17 特許分析 80

5.17.1 アプローチ 80

5.17.2 文書タイプ 81

5.17.3 洞察 81

5.17.4 特許の法的地位 82

5.17.5 管轄地域の分析 82

5.17.6 上位企業/出願人 83

5.17.7 過去10年間の特許所有者トップ10(米国) 84

6 ゼロ液体排出システム市場、プロセス別 85

6.1 導入 86

6.2 ゼロ液体排出プロセス 87

6.2.1 前処理 88

6.2.1.1 浮遊物質や汚染物質によるスケーリングやファウリングの防止が市場を牽引 88

6.2.2 ろ過 88

6.2.2.1 回収した透過液の再利用による需要への燃料供給 88

6.2.3 蒸発/晶析 88

6.2.3.1 汚染物質除去の需要が市場を牽引 88

7 ゼロ液体排出システム市場、容量別 89

7.1 導入 90

7.2 小規模 91

7.2.1 水資源が限られている産業への需要

市場を牽引 91

7.3 中規模 92

7.3.1 繊維、医薬品、食品加工産業での幅広い使用が市場を牽引 92

7.4 大規模 92

7.4.1 石油化学、製薬、発電分野での重要な使用、

発電分野での重要な使用が需要を促進 92

8 ゼロ液体排出システム市場:用途別 93

8.1 導入 94

8.2 ブライン廃棄 95

8.2.1 海洋環境への濃縮ブラインの排出排除が市場の燃料に 95

8.3 化学廃棄物 95

8.3.1 環境規制が市場を促進 95

8.4 食品・飲料廃棄物 96

8.4.1 汚染の防止が市場を牽引 96

8.5 電子機器 96

8.5.1 金、銀、パラジウムなどの有価金属の回収が需要を促進 96

金、銀、パラジウムなどの有価金属の回収が需要を促進 96

8.6 その他の用途 96

9 ゼロ液体排出システム市場、システム別 97

9.1 導入 98

9.2 従来型 100

9.2.1 中・小容量プラントの需要が市場を牽引 100

9.3 ハイブリッド 100

9.3.1 高い水回収率が使用を促進する 100

10 ゼロ液体排出システム市場:最終用途産業別 101

10.1 導入 102

10.2 エネルギー・電力 104

10.2.1 火力発電産業が市場を牽引 104

10.2.2 発電 104

10.2.3 石油・ガス 105

10.3 化学・石油化学 105

10.3.1 水集約度の高い分野が市場を牽引 105

10.4 食品・飲料 106

10.4.1 大量の排水が需要を促進 106

10.5 繊維 106

10.5.1 大量の排水が市場を牽引 106

10.6 医薬品 107

10.6.1 有害化学物質と塩類の排出が市場を促進 107

10.7 半導体・エレクトロニクス 107

10.7.1 プロセスの重要性が市場を促進 107

10.8 その他の最終用途産業 107

11 ゼロ液体排出システム市場(地域別) 108

11.1 はじめに 109

11.2 北米 111

11.2.1 米国 116

11.2.1.1 エネルギー・電力、化学・石油化学の最終用途産業の急成長が市場を牽引 116

11.2.2 カナダ 118

11.2.2.1 産業の拡大が市場需要を高める 118

11.2.3 メキシコ 120

11.2.3.1 淡水不足と製造業への投資増加が成長を促進 120

11.3 欧州 122

11.3.1 ドイツ 127

11.3.1.1 強固な製造基盤が市場成長を牽引 127

11.3.2 フランス 129

11.3.2.1 大規模化学産業が市場を牽引 129

11.3.3 スペイン 131

11.3.3.1 化学・石油化学、エネルギー・電力、医薬品分野が需要を牽引 131

11.3.4 イギリス 133

11.3.4.1 政府の政策が市場を牽引 133

11.3.5 イタリア 135

11.3.5.1 医療・製薬業界が需要を牽引 135

11.3.6 ロシア 137

11.3.6.1 水不足と汚染に対する懸念の高まりが市場を牽引 137

11.3.7 その他のヨーロッパ 139

11.4 アジア太平洋地域 141

11.4.1 中国 146

11.4.1.1 電力・廃水処理分野が市場を牽引 146

11.4.2 日本 148

11.4.2.1 水処理における技術革新が市場を牽引 148

11.4.3 インド 149

11.4.3.1 都市化と工業化が市場成長を促進 149

11.4.4 韓国 151

11.4.4.1 食品・飲料産業が需要を創出 151

11.4.5 台湾 153

11.4.5.1 再生水処理に関する規制の枠組みが市場を牽引 153

市場を牽引 153

11.4.6 オーストラリア 155

11.4.6.1 上水・廃水処理のインフラが整備され

安定した需要につながる 155

11.4.7 その他のアジア太平洋地域 157

11.5 中東・アフリカ 159

11.5.1 GCC諸国 164

11.5.1.1 サウジアラビア 165

11.5.1.1.1 経済の多様化が市場成長を促進 165

11.5.1.2 ウアイ 167

11.5.1.2.1 石油生産量の増加が市場を押し上げる 167

11.5.1.3 その他のGCC諸国 169

11.5.2 南アフリカ 171

11.5.2.1 大規模化学産業が需要を促進 171

11.6 南米 175

11.6.1 ブラジル 179

11.6.1.1 化学処理、製薬、石油・ガス処理、

食品・飲料産業が市場を牽引 179

11.6.2 アルゼンチン 181

11.6.2.1 衛生サービスへの投資が市場成長を牽引 181

11.6.3 その他の南米諸国 183

12 競争環境 185

12.1 はじめに 185

12.2 主要プレーヤーの戦略/勝利への権利(2019~2024年) 185

12.3 収益分析(2021-2023年) 187

12.4 市場シェア分析、2023年 187

12.5 企業評価と財務指標(2023年) 190

12.6 ブランド/製品の比較 191

12.7 企業評価マトリックス:主要企業、2023年 191

12.7.1 スター企業 191

12.7.2 新興リーダー 191

12.7.3 浸透型プレイヤー 192

12.7.4 参加企業 192

12.7.5 企業フットプリント:主要プレイヤー(2023年) 193

12.7.5.1 企業フットプリント 193

12.7.5.2 地域別フットプリント 194

12.7.5.3 システムフットプリント 195

12.7.5.4 プロセスフットプリント 196

12.7.5.5 最終用途産業のフットプリント 197

12.8 企業評価マトリクス:新興企業/SM(2023年) 198

12.8.1 進歩的企業 198

12.8.2 対応力のある企業 199

12.8.3 ダイナミックな企業 199

12.8.4 スターティングブロック 199

12.8.5 競争ベンチマーキング 200

12.8.5.1 主要新興企業/中小企業の詳細リスト 200

12.8.5.2 主要新興企業/中小企業の競合ベンチマーキング 201

12.9 競争シナリオ 202

12.9.1 製品上市 202

12.9.2 事業拡大 203

12.9.3 取引 207

13 企業プロファイル 210

13.1 主要企業 210

Alfa Laval (Sweden)

AQUARION AG (Switzerland)

Veolia (France)

Aquatech (US)

GEA Group (Germany)

Praj Industries Ltd (India)

H2O GmbH (Germany)

Thermax Limited (India)

Mitsubishi Chemical Corporation. (Japan)

ANDRITZ (Austria)

Toshiba Infrastructure Systems & Solutions Corporation (Japan)

IEI (India)

Condorchem Enviro Solutions (Spain)

Kurita Water Industries Ltd (Japan)

Evoqua Water Technologies LLC (US)

14 付録 274

14.1 ディスカッションガイド 274

14.2 Knowledgestore: Marketsandmarketsの購読ポータル 276

14.3 カスタマイズオプション 278

14.4 関連レポート 278

14.5 著者の詳細 279

The global zero liquid discharge system market is witnessing growth due to its versatile properties and it is also widely used in various industries due to its exceptional properties. Furthermore, zero liquid discharge system are required for the application in various end use industries like energy & power, chemicals & petrochemicals, food & beverages, textiles, pharmaceuticals, semiconductors & electronics, and other end use industries , which fuels the need for zero liquid discharge systems.

“Pre treatment process type is projected to be the second fastest process type in terms of value.”

Pre treatment process type is projected to be the second fastest process type in terms of value in the zero liquid discharge system market due to various factors. The pre treatment process is one of the initial process in the zero liquid discharge systems. As pre treatment process removes contamination and its conditions the water. The goal with which the pre treatment process is done is to reduce the amount of contaminants in the water and prepare it for downstream equipment. The pre treatment method includes process like filtering, chemical treatment, coagulation, clarification, microfiltration and ultrafiltration. This process also reduces total suspended solids, chemical oxygen demand, and turbidity. Pre treatment is important process as it helps to protect downstream membrane process, minimize the need for downstream treatment and it also help downstream equipment perform more efficiently. Pre treatment process is carried out mostly in end use industries like energy & power, chemicals & petrochemicals, textiles. The process is followed amongst these industries as they produce large volumes of waste water and these industries require recycled water to carry out their functions.

“Semiconductors & electronics end use industry is expected to be the second fastest growing end use industry for forecasted period in terms of value.”

Semiconductors & electronics end use industry is expected to be the second fastest growing end use industry for forecasted period in terms of value. Electronics manufacturing process requires high purity water to avoid contamination of sensitive components. As the environmental regulations are tightened globally, the end use industry face pressure to minimize its ecological footprint. ZLD systems help the companies to adopt to these regulations by eliminating liquid waste discharge and reducing freshwater consumption, making them an attractive option for manufacturers looking to enhance their sustainability practices.

“Middle East & Africa is estimated to be the second fastest growing region in terms of value for the forecasted period.”

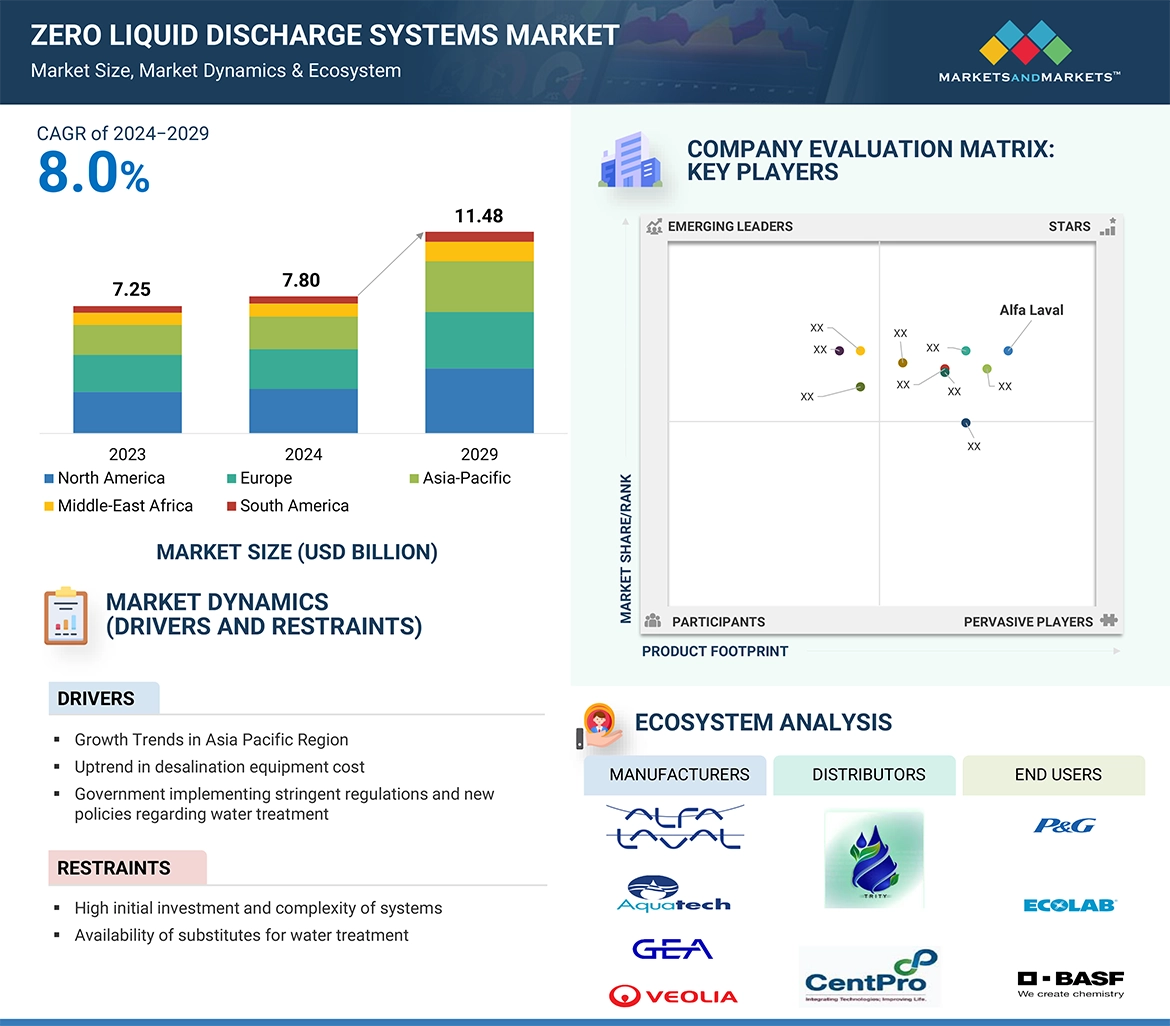

Middle East and Africa region is expected to be the second fastest growing region in forecasted period in terms of value. As these region faces severe water scarcity challenges which make it essential for the countries to practice efficient water management practices. Rapid industrialization across various end use industries like chemicals and petrochemicals, oil and gas is occuring in these region, as these industries expand they generate substantial amount of wastewater that require effective treatment solutions. Also government are implementing various regulations aimed at reducing water pollution and promoting sustainable practices. These parameters are helping the ZLD system market to grow at a faster rate.

In-depth interviews were conducted with Chief Executive Officers (CEOs), marketing directors, other innovation and technology directors, and executives from various key organizations operating in the zero liquid discharge system market, and information was gathered from secondary research to determine and verify the market size of several segments.

• By Company Type: Tier 1 – 40%, Tier 2 – 30%, and Tier 3 – 30%

• By Designation: C Level Executives– 20%, Directors – 10%, and Others – 70%

• By Region: North America – 22%, Europe – 22%, APAC – 45%, ROW –11%

The Zero liquid discharge system market comprises major players such as Alfa Laval (Sweden), AQUARION AG (Switzerland), Veolia (France), Aquatech (US), GEA Group (Germany), Praj Industries Ltd (India), H2O GmbH (Germany), Thermax Limited (India), Mitsubishi Chemical Corporation. (Japan), ANDRITZ (Austria), Toshiba Infrastructure Systems & Solutions Corporation (Japan), IEI (India), Condorchem Enviro Solutions (Spain), Kurita Water Industries Ltd (Japan), Evoqua Water Technologies LLC (US). The study includes in-depth competitive analysis of these key players in the zero liquid discharge system market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This report segments the market for zero liquid discharge system market on the basis of system, process, capacity, application, end use industry, and region, and provides estimations for the overall value of the market across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products & services, key strategies, new product launches, expansions, and mergers & acquisition associated with the market for zero liquid discharge system market.

Key benefits of buying this report

This research report is focused on various levels of analysis — industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view on the competitive landscape; emerging and high-growth segments of the zero liquid discharge system market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

• Market Penetration: Comprehensive information on the zero liquid discharge system market offered by top players in the global zero liquid discharge system market.

• Analysis of drivers: (Growth trends in Asia Pacific region, uptrend in desalination equipment costs, Government implementing stringent regulations and new policies regarding water treatment) restraints (High initial investment and complexity of systems, Availability of substitutes for water treatment), opportunities (Growing public concern about water scarcity and environmental degradation, Higher growth in emerging economies of Asia Pacific) and challenges (Operational cost and high maintenance, Controlling water loss during the operation)

• Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the zero liquid discharge system market.

• Market Development: Comprehensive information about lucrative emerging markets — the report analyzes the markets for zero liquid discharge system market across regions.

• Market Capacity: Production capacities of companies producing zero liquid discharge system are provided wherever available with upcoming capacities for the zero liquid discharge system market.

• Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the zero liquid discharge system market.

1 INTRODUCTION 27

1.1 STUDY OBJECTIVES 27

1.2 MARKET DEFINITION 27

1.3 MARKET SCOPE 28

1.3.1 ZERO LIQUID DISCHARGE SYSTEMS MARKET SEGMENTATION 28

1.3.2 INCLUSIONS AND EXCLUSIONS 29

1.3.3 YEARS CONSIDERED 30

1.3.4 CURRENCY CONSIDERED 30

1.3.5 UNITS CONSIDERED 30

1.4 STAKEHOLDERS 30

1.5 SUMMARY OF CHANGES 31

2 RESEARCH METHODOLOGY 33

2.1 RESEARCH DATA 33

2.1.1 SECONDARY DATA 34

2.1.1.1 Key secondary sources 34

2.1.1.2 Key data from secondary sources 34

2.1.2 PRIMARY DATA 35

2.1.2.1 Key data from primary sources 36

2.1.2.2 Key industry insights 36

2.1.2.3 Breakdown of interviews with experts 37

2.2 MARKET SIZE ESTIMATION 38

2.2.1 BOTTOM-UP APPROACH 39

2.2.2 TOP-DOWN APPROACH 39

2.3 DATA TRIANGULATION 40

2.4 RESEARCH ASSUMPTIONS 41

2.5 FACTOR ANALYSIS 41

2.6 GROWTH FORECAST 41

2.6.1 SUPPLY SIDE 42

2.6.2 DEMAND SIDE 42

2.7 RESEARCH LIMITATIONS 42

2.8 RISK ASSESSMENT 42

3 EXECUTIVE SUMMARY 43

4 PREMIUM INSIGHTS 47

4.1 OPPORTUNITIES FOR PLAYERS IN ZERO LIQUID DISCHARGE SYSTEMS MARKET 47

4.2 ZERO LIQUID DISCHARGE SYSTEMS MARKET, BY SYSTEM 47

4.3 ZERO LIQUID DISCHARGE SYSTEMS MARKET, BY CAPACITY 48

4.4 ZERO LIQUID DISCHARGE SYSTEMS MARKET, BY END-USE INDUSTRY 48

4.5 ZERO LIQUID DISCHARGE SYSTEMS MARKET, BY COUNTRY 49

5 MARKET OVERVIEW 50

5.1 INTRODUCTION 50

5.2 IMPACT OF AI/GEN AI 50

5.2.1 INTRODUCTION 50

5.2.2 OVERVIEW OF IMPACT 50

5.2.2.1 Transforming zero liquid discharge systems with AI and machine learning 50

5.2.2.2 Impact of AI/GenAI on reverse osmosis 50

5.2.2.3 Impact of AI on water treatment and zero liquid discharge systems 51

5.3 MARKET DYNAMICS 51

5.3.1 DRIVERS 52

5.3.1.1 Stringent environmental regulations, industrial expansion,

and increasing water scarcity in Asia Pacific 52

5.3.1.2 Uptrend in cost of desalination equipment 52

5.3.1.3 Implementation of stringent regulations and new policies regarding water treatment 53

5.3.1.4 Commitment of various organizations to sustainability initiatives 53

5.3.1.5 Increasing water scarcity across regions 54

5.3.2 RESTRAINTS 54

5.3.2.1 High initial investments and complexity of systems 54

5.3.2.2 Availability of substitutes for water treatment 55

5.3.3 OPPORTUNITIES 55

5.3.3.1 Growing public concerns about water scarcity and

environmental degradation 55

5.3.3.2 Rapid industrial growth in emerging economies of Asia Pacific 55

5.3.4 CHALLENGES 56

5.3.4.1 High maintenance and operational cost 56

5.3.4.2 Controlling water loss during operation 56

5.4 PORTER’S FIVE FORCES ANALYSIS 57

5.4.1 THREAT OF SUBSTITUTES 58

5.4.2 BARGAINING POWER OF BUYERS 58

5.4.3 THREAT OF NEW ENTRANTS 58

5.4.4 BARGAINING POWER OF SUPPLIERS 58

5.4.5 INTENSITY OF COMPETITIVE RIVALRY 58

5.5 KEY STAKEHOLDERS AND BUYING CRITERIA 59

5.5.1 KEY STAKEHOLDERS IN BUYING PROCESS 59

5.5.2 BUYING CRITERIA 60

5.6 MACROECONOMIC INDICATORS 60

5.6.1 GLOBAL GDP TRENDS 60

5.7 VALUE CHAIN ANALYSIS 61

5.7.1 RAW MATERIAL SUPPLIERS 62

5.7.2 MANUFACTURERS 62

5.7.3 SUPPLIERS/DISTRIBUTORS 62

5.7.4 END-USE INDUSTRIES 63

5.8 ECOSYSTEM 63

5.9 CASE STUDY ANALYSIS 64

5.9.1 ZERO LIQUID DISCHARGE AT PEARL GTL PLANT 64

5.9.2 WASTEWATER RECYCLING AND ZERO LIQUID DISCHARGE SYSTEM

FOR CTX INDUSTRY IN CHINA 65

5.9.3 ZERO LIQUID DISCHARGE IN WASTEWATER TREATMENT 65

5.10 REGULATORY LANDSCAPE 66

5.10.1 REGULATIONS 66

5.10.1.1 Europe 66

5.10.1.2 Asia Pacific 67

5.10.1.3 North America 68

5.10.2 REGULATORY BODIES, GOVERNMENT BODIES, AND OTHER AGENCIES 69

5.11 TECHNOLOGY ANALYSIS 71

5.11.1 KEY TECHNOLOGIES 71

5.11.1.1 Membrane technology 71

5.11.2 COMPLEMENTARY TECHNOLOGIES 71

5.11.2.1 Ultrafiltration technology 71

5.11.2.2 Falling film evaporators 72

5.11.3 ADJACENT TECHNOLOGIES 72

5.11.3.1 Forward osmosis 72

5.12 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS 73

5.13 TRADE ANALYSIS 73

5.13.1 EXPORT SCENARIO (HS CODE 842121) 73

5.13.2 IMPORT SCENARIO (HS CODE 842121) 75

5.14 KEY CONFERENCES & EVENTS, 2024–2025 76

5.15 PRICING TREND ANALYSIS 77

5.15.1 AVERAGE SELLING PRICE, BY REGION 77

5.15.2 AVERAGE SELLING PRICE TREND OF ZERO LIQUID DISCHARGE SYSTEMS 77

5.15.3 AVERAGE SELLING PRICE OF ZERO LIQUID DISCHARGE SYSTEMS OF KEY PLAYERS, BY CAPACITY 78

5.15.4 AVERAGE SELLING PRICE TREND OF ZERO LIQUID DISCHARGE SYSTEMS OF KEY PLAYERS, BY END-USE INDUSTRY 78

5.15.5 AVERAGE SELLING PRICE OF ZERO LIQUID DISCHARGE SYSTEMS OF KEY PLAYERS, BY END-USE INDUSTRY 79

5.15.6 AVERAGE SELLING PRICE OF ZERO LIQUID DISCHARGE SYSTEMS, BY REGION 79

5.16 INVESTMENT AND FUNDING SCENARIO 80

5.17 PATENT ANALYSIS 80

5.17.1 APPROACH 80

5.17.2 DOCUMENT TYPE 81

5.17.3 INSIGHTS 81

5.17.4 LEGAL STATUS OF PATENTS 82

5.17.5 JURISDICTION ANALYSIS 82

5.17.6 TOP COMPANIES/APPLICANTS 83

5.17.7 TOP 10 PATENT OWNERS (US) LAST 10 YEARS 84

6 ZERO LIQUID DISCHARGE SYSTEMS MARKET, BY PROCESS 85

6.1 INTRODUCTION 86

6.2 ZERO LIQUID DISCHARGE PROCESSES 87

6.2.1 PRETREATMENT 88

6.2.1.1 Prevention of scaling or fouling by suspended solids and contaminants to drive market 88

6.2.2 FILTRATION 88

6.2.2.1 Reuse of recovered permeates to fuel demand 88

6.2.3 EVAPORATION/CRYSTALLIZATION 88

6.2.3.1 Demand for removal of contaminants to propel market 88

7 ZERO LIQUID DISCHARGE SYSTEMS MARKET, BY CAPACITY 89

7.1 INTRODUCTION 90

7.2 SMALL SCALE 91

7.2.1 DEMAND FOR INDUSTRIES WITH LIMITED WATER RESOURCES

TO DRIVE MARKET 91

7.3 MEDIUM SCALE 92

7.3.1 WIDE USE IN TEXTILES, PHARMACEUTICALS, AND FOOD PROCESSING INDUSTRIES TO PROPEL MARKET 92

7.4 LARGE SCALE 92

7.4.1 CRITICAL USE IN PETROCHEMICAL, PHARMACEUTICAL,

AND POWER GENERATION SECTORS TO FUEL DEMAND 92

8 ZERO LIQUID DISCHARGE SYSTEMS MARKET, BY APPLICATION 93

8.1 INTRODUCTION 94

8.2 BRINE DISPOSAL 95

8.2.1 ELIMINATION OF DISCHARGE OF CONCENTRATED BRINE INTO MARINE ENVIRONMENTS TO FUEL MARKET 95

8.3 CHEMICAL WASTE 95

8.3.1 ENVIRONMENTAL REGULATIONS TO PROPEL MARKET 95

8.4 FOOD & BEVERAGE WASTE 96

8.4.1 PREVENTION OF CONTAMINATION TO DRIVE MARKET 96

8.5 ELECTRONICS 96

8.5.1 RECOVERY OF VALUABLE METALS SUCH AS GOLD, SILVER,

AND PALLADIUM TO FUEL DEMAND 96

8.6 OTHER APPLICATIONS 96

9 ZERO LIQUID DISCHARGE SYSTEMS MARKET, BY SYSTEM 97

9.1 INTRODUCTION 98

9.2 CONVENTIONAL 100

9.2.1 REQUIREMENT IN SMALL AND MEDIUM CAPACITY PLANTS TO DRIVE MARKET 100

9.3 HYBRID 100

9.3.1 HIGH WATER RECOVERY RATE TO PROMOTE USE 100

10 ZERO LIQUID DISCHARGE SYSTEMS MARKET, BY END-USE INDUSTRY 101

10.1 INTRODUCTION 102

10.2 ENERGY & POWER 104

10.2.1 THERMAL POWER INDUSTRY TO DRIVE MARKET 104

10.2.2 POWER GENERATION 104

10.2.3 OIL & GAS 105

10.3 CHEMICALS & PETROCHEMICALS 105

10.3.1 HIGHLY WATER-INTENSIVE SECTOR TO PROPEL MARKET 105

10.4 FOOD & BEVERAGES 106

10.4.1 SIGNIFICANT EFFLUENT VOLUMES TO FUEL DEMAND 106

10.5 TEXTILES 106

10.5.1 HEAVY EFFLUENT DISCHARGE TO DRIVE MARKET 106

10.6 PHARMACEUTICALS 107

10.6.1 DISCHARGE OF HAZARDOUS CHEMICALS AND SALTS TO PROPEL MARKET 107

10.7 SEMICONDUCTORS & ELECTRONICS 107

10.7.1 CRITICALITY OF PROCESSES TO FUEL MARKET 107

10.8 OTHER END-USE INDUSTRIES 107

11 ZERO LIQUID DISCHARGE SYSTEMS MARKET, BY REGION 108

11.1 INTRODUCTION 109

11.2 NORTH AMERICA 111

11.2.1 US 116

11.2.1.1 Rapid growth of energy & power and chemicals & petrochemicals end-use industries to drive market 116

11.2.2 CANADA 118

11.2.2.1 Industrial expansion to enhance market demand 118

11.2.3 MEXICO 120

11.2.3.1 Scarcity of fresh water and increased investments in manufacturing sector to drive growth 120

11.3 EUROPE 122

11.3.1 GERMANY 127

11.3.1.1 Strong manufacturing base to drive market growth 127

11.3.2 FRANCE 129

11.3.2.1 Large chemical industry to drive market 129

11.3.3 SPAIN 131

11.3.3.1 Chemicals & petrochemicals, energy & power, and pharmaceuticals sectors to drive demand 131

11.3.4 UK 133

11.3.4.1 Government policies to drive market 133

11.3.5 ITALY 135

11.3.5.1 Healthcare and pharmaceutical industries to drive demand 135

11.3.6 RUSSIA 137

11.3.6.1 Growing concerns about water scarcity and pollution to drive market 137

11.3.7 REST OF EUROPE 139

11.4 ASIA PACIFIC 141

11.4.1 CHINA 146

11.4.1.1 Power and wastewater treatment sectors to propel market 146

11.4.2 JAPAN 148

11.4.2.1 Technological innovations in water treatment to propel market 148

11.4.3 INDIA 149

11.4.3.1 Urbanization and industrialization to propel market growth 149

11.4.4 SOUTH KOREA 151

11.4.4.1 Food & beverage industry to create demand 151

11.4.5 TAIWAN 153

11.4.5.1 Regulatory framework for treatment of reclaimed water

to drive market 153

11.4.6 AUSTRALIA 155

11.4.6.1 Established infrastructure for water & wastewater treatment

to lead to steady demand 155

11.4.7 REST OF ASIA PACIFIC 157

11.5 MIDDLE EAST & AFRICA 159

11.5.1 GCC COUNTRIES 164

11.5.1.1 Saudi Arabia 165

11.5.1.1.1 Economic diversification to enhance market growth 165

11.5.1.2 UAE 167

11.5.1.2.1 Rising oil production to boost market 167

11.5.1.3 Rest of GCC countries 169

11.5.2 SOUTH AFRICA 171

11.5.2.1 Large chemical industry to propel demand 171

11.6 SOUTH AMERICA 175

11.6.1 BRAZIL 179

11.6.1.1 Chemical processing, pharmaceutical, oil & gas processing,

and food & beverage industries to drive market 179

11.6.2 ARGENTINA 181

11.6.2.1 Investment in sanitation services to drive market growth 181

11.6.3 REST OF SOUTH AMERICA 183

12 COMPETITIVE LANDSCAPE 185

12.1 INTRODUCTION 185

12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2019–2024 185

12.3 REVENUE ANALYSIS, 2021–2023 187

12.4 MARKET SHARE ANALYSIS, 2023 187

12.5 COMPANY VALUATION AND FINANCIAL METRICS, 2023 190

12.6 BRAND/PRODUCT COMPARISON 191

12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023 191

12.7.1 STARS 191

12.7.2 EMERGING LEADERS 191

12.7.3 PERVASIVE PLAYERS 192

12.7.4 PARTICIPANTS 192

12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023 193

12.7.5.1 Company footprint 193

12.7.5.2 Region footprint 194

12.7.5.3 System footprint 195

12.7.5.4 Process footprint 196

12.7.5.5 End-use industry footprint 197

12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023 198

12.8.1 PROGRESSIVE COMPANIES 198

12.8.2 RESPONSIVE COMPANIES 199

12.8.3 DYNAMIC COMPANIES 199

12.8.4 STARTING BLOCKS 199

12.8.5 COMPETITIVE BENCHMARKING 200

12.8.5.1 Detailed list of key startups/SMEs 200

12.8.5.2 Competitive benchmarking of key startups/SMEs 201

12.9 COMPETITIVE SCENARIO 202

12.9.1 PRODUCT LAUNCHES 202

12.9.2 EXPANSIONS 203

12.9.3 DEALS 207

13 COMPANY PROFILES 210

13.1 KEY PLAYERS 210

13.1.1 ALFA LAVAL 210

13.1.1.1 Business overview 210

13.1.1.2 Products/Solutions/Services offered 211

13.1.1.3 Recent developments 212

13.1.1.3.1 Expansions 212

13.1.1.4 MnM view 213

13.1.1.4.1 Right to win 213

13.1.1.4.2 Strategic choices 213

13.1.1.4.3 Weaknesses and competitive threats 213

13.1.2 AQUARION AG 214

13.1.2.1 Business overview 214

13.1.2.2 Products/Solutions/Services offered 214

13.1.2.3 Recent developments 216

13.1.2.3.1 Deals 216

13.1.2.3.2 Expansions 216

13.1.2.4 MnM view 216

13.1.3 VEOLIA 217

13.1.3.1 Business overview 217

13.1.3.2 Products/Solutions/Services offered 218

13.1.3.3 Recent developments 219

13.1.3.3.1 Product launches 219

13.1.3.3.2 Deals 220

13.1.3.3.3 Expansions 221

13.1.3.4 MnM view 221

13.1.3.4.1 Right to win 221

13.1.3.4.2 Strategic choices 221

13.1.3.4.3 Weaknesses and competitive threats 221

13.1.4 AQUATECH 222

13.1.4.1 Business overview 222

13.1.4.2 Products/Solutions/Services offered 222

13.1.4.3 Recent developments 224

13.1.4.3.1 Deals 224

13.1.4.4 MnM view 225

13.1.4.4.1 Right to win 225

13.1.4.4.2 Strategic choices 225

13.1.4.4.3 Weaknesses and competitive threats 225

13.1.5 GEA GROUP 226

13.1.5.1 Business overview 226

13.1.5.2 Products/Solutions/Services offered 227

13.1.5.3 Recent developments 228

13.1.5.3.1 Expansions 228

13.1.5.4 MnM view 230

13.1.5.4.1 Right to win 230

13.1.5.4.2 Strategic choices 230

13.1.5.4.3 Weaknesses and competitive threats 230

13.1.6 PRAJ INDUSTRIES 231

13.1.6.1 Business overview 231

13.1.6.2 Products/Solutions/Services offered 233

13.1.6.3 MnM view 234

13.1.6.3.1 Right to win 234

13.1.6.3.2 Strategic choices 234

13.1.6.3.3 Weaknesses and competitive threats 234

13.1.7 H2O GMBH 235

13.1.7.1 Business overview 235

13.1.7.2 Products/Solutions/Services offered 235

13.1.7.3 MnM view 236

13.1.8 THERMAX LIMITED 237

13.1.8.1 Business overview 237

13.1.8.2 Products/Solutions/Services offered 239

13.1.8.3 Recent developments 240

13.1.8.3.1 Deals 240

13.1.8.3.2 Expansions 240

13.1.8.4 MnM view 241

13.1.8.4.1 Right to win 241

13.1.8.4.2 Strategic choices 241

13.1.8.4.3 Weaknesses and competitive threats 241

13.1.9 MITSUBISHI CHEMICAL CORPORATION 242

13.1.9.1 Business overview 242

13.1.9.2 Products/Solutions/Services offered 243

13.1.9.3 MnM view 244

13.1.10 ANDRITZ 245

13.1.10.1 Business overview 245

13.1.10.2 Products/Solutions/Services offered 246

13.1.10.3 MnM view 246

13.1.11 TOSHIBA INFRASTRUCTURE SYSTEMS & SOLUTIONS CORPORATION 247

13.1.11.1 Business overview 247

13.1.11.2 Products/Solutions/Services offered 249

13.1.11.3 MnM view 249

13.1.12 IEI (ION EXCHANGE) 250

13.1.12.1 Business overview 250

13.1.12.2 Products/Solutions/Services offered 251

13.1.12.3 MnM view 251

13.1.13 CONDORCHEM ENVIRO SOLUTIONS 252

13.1.13.1 Business overview 252

13.1.13.2 Products/Solutions/Services offered 252

13.1.13.3 Recent developments 253

13.1.13.3.1 Expansions 253

13.1.13.4 MnM view 253

13.1.14 KURITA WATER INDUSTRIES LTD. 254

13.1.14.1 Business overview 254

13.1.14.2 Products/Solutions/Services offered 255

13.1.14.3 MnM view 256

13.1.15 EVOQUA WATER TECHNOLOGIES LLC 257

13.1.15.1 Business overview 257

13.1.15.2 Products/Solutions/Services offered 259

13.1.15.3 Recent developments 260

13.1.15.3.1 Deals 260

13.1.15.3.2 Expansions 260

13.1.15.4 MnM view 260

13.2 OTHER PLAYERS 261

13.2.1 PETRO SEP CORPORATION 261

13.2.2 FLUENCE CORPORATION LIMITED 262

13.2.3 ENVISOL ARVIND 263

13.2.4 SAMCO TECHNOLOGIES 264

13.2.5 LENNTECH B.V. 265

13.2.6 SHIVA GLOBAL ENVIRONMENTAL PRIVATE LIMITED 266

13.2.7 GMM PFAUDLER 267

13.2.8 IDE WATER TECHNOLOGIES 268

13.2.9 SALTWORKS TECHNOLOGIES INC 269

13.2.10 ENCON EVAPORATORS 269

13.2.11 SCALEBAN EQUIPMENTS PVT.LTD. 270

13.2.12 MEMSIFT INNOVATIONS PTE LTD. 271

13.2.13 GRUNDFOS 272

13.2.14 U.S. WATER SERVICES CORPORATION 273

14 APPENDIX 274

14.1 DISCUSSION GUIDE 274

14.2 KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL 276

14.3 CUSTOMIZATION OPTIONS 278

14.4 RELATED REPORTS 278

14.5 AUTHOR DETAILS 279

❖ 世界のゼロ液体排出システム市場に関するよくある質問(FAQ) ❖

・ゼロ液体排出システムの世界市場規模は?

→MarketsandMarkets社は2024年のゼロ液体排出システムの世界市場規模を78.0億米ドルと推定しています。

・ゼロ液体排出システムの世界市場予測は?

→MarketsandMarkets社は2029年のゼロ液体排出システムの世界市場規模を114.8億米ドルと予測しています。

・ゼロ液体排出システム市場の成長率は?

→MarketsandMarkets社はゼロ液体排出システムの世界市場が2024年~2029年に年平均8.0%成長すると予測しています。

・世界のゼロ液体排出システム市場における主要企業は?

→MarketsandMarkets社は「Alfa Laval (Sweden), AQUARION AG (Switzerland), Veolia (France), Aquatech (US), GEA Group (Germany), Praj Industries Ltd (India), H2O GmbH (Germany), Thermax Limited (India), Mitsubishi Chemical Corporation. (Japan), ANDRITZ (Austria), Toshiba Infrastructure Systems & Solutions Corporation (Japan), IEI (India), Condorchem Enviro Solutions (Spain), Kurita Water Industries Ltd (Japan), Evoqua Water Technologies LLC (US)など ...」をグローバルゼロ液体排出システム市場の主要企業として認識しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、納品レポートの情報と少し異なる場合があります。